(Thursday Market Open) Equity index futures are higher ahead of another day of congressional testimony from Fed chairman Jerome Powell as he moves from the Senate Banking Committee to the House Financial Services Committee.

Potential Market Movers

While Mr. Powell told the Senate yesterday that a recession was possible, he also said that the Fed would slow its rate hiking plans if the economy slowed. This appears to be helping stocks this morning as the S&P 500 futures traded 0.3% higher premarket. However, the Cboe Market Volatility Index (VIX) was higher this morning as well, which suggests that investors are still a little tentative.

Initial jobless claims were released ahead of the opening bell revealing a higher-than-expected number of people looking for unemployment benefits. After the open, investors will see the U.S. manufacturing PMI to gain insights into the strength of the U.S. manufacturing sector.

A few more earnings stragglers reported this morning:

- Accenture (ACN) reported a miss on earnings despite better-than-expected revenues, causing the stock to fall 3.63% before the open. ACN cited the strong dollar as one of the reasons for the miss.

- Darden Restaurants (DRI) beat on top- and bottom-line numbers, raised its dividend, and announced a $1 billion stock buyback program. The stock rallied3.8% before the opening bell.

- FactSet Research (FDS) also beat on earnings and revenue estimates and reaffirmed its fiscal 2022 earning guidance around the upper end of analyst estimates. FDS was up 1.41% in premarket action.

- FedEx (FDX) is expected to report after the closing bell.

Reviewing the Market Minutes

Even though Federal Reserve Chairman Jerome Powell told Congress yesterday that the economy is still strong enough to tolerate more interest rate hikes to fight inflation, investors stepped back from a midday rally to leave all major indexes modestly in the red.

It was a late reversal to Tuesday’s turnaround rally after heavy losses last week immediately following the Fed’s 75-basis-point rate hike announcement. The Dow Jones Industrial Average ($DJI) and the Nasdaq Composite ($COMP) both lost 0.15% by the close, followed by a 0.13% loss for the S&P 500 (SPX). The Russell 2000 (RUT) finished down 0.22%. Last week, the S&P 500 finished its worst week since March 2020.

Perhaps a sign of continued volatility to come, the Cboe Market Volatility Index (VIX) finished slightly below 30.

Earlier Wednesday, Powell told the U.S. Senate Banking Committee that the Fed believes the U.S. economy could withstand future rate hikes but acknowledged the central bank’s current direction could cause recession. But he added that the Fed believes continued rate increases will be “absolutely essential” to curtailing rising inflation until the central bank sees prices slow down.

As Powell continues his discussions with Congress today, on Wednesday, Chicago Federal Reserve Bank President Charles Evans said he would probably back another 75-basis-point hike at the Fed’s July meeting “to take the steam” out of inflationary conditions.

With AAA confirming a week of price decreases under the $5-per-gallon level, broader concerns about a global economic slowdown curbing energy usage made that sector Wednesday’s worst performer as the S&P Energy Select Sector Index lost 4.19% for the session.

Top-performing sectors were real estate (+1.55%), health care (+1.42%), and utilities (+1.04%).

After the closing bell on Wednesday, KB Home KBH reported better-than-expected earnings and added that even though it expects the housing market to moderate, it thinks it will still meet its revenue goals in 2022. KBH gained 5.51% in after-market trading.

Also, after the close, adhesives maker H.B. Fuller FUL gained 0.75% after beating earnings and revenue estimates.

Gas prices weren’t having much impact on Winnebago Industries WGO, which exceeded earnings expectations and gained 2.62% by the close.

Even embattled streamer Netflix (NASDAQ: NFLX), reportedly in talks about moving ahead with ad-supported subscriptions and other partnerships, gained nearly 8% on the day.

Meanwhile, Altria Group MO lost 9% after The Wall Street Journal reported early yesterday that the Food and Drug Administration is planning to order Juul Labs to take its e-cigarettes off the market. MO purchased a 35% stake in Juul in 2018. The Dow Jones U.S. Tobacco Total Stock Market Index lost 3.74% on Wednesday.

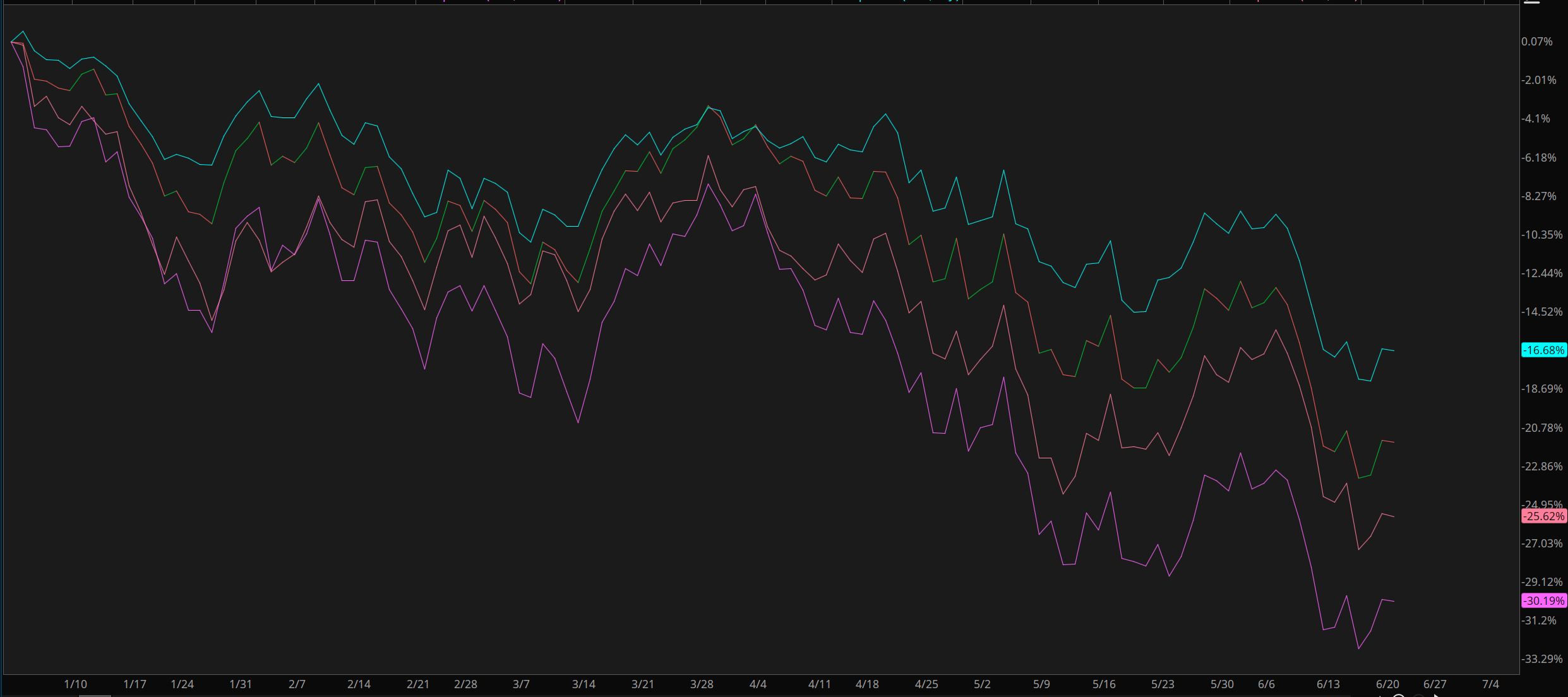

CHART OF THE DAY: POWELL BOUNCE. The Dow Jones Transportation Average ($DJT—BLUE), S&P 500 (SPX—RED/GREEN), Nasdaq Composite ($COMP—PINK), and the Russell 2000 (RUT—RED) failed to sustain a midday rally after Federal Reserve Chairman Jerome Powell’s speech to the U.S. Senate Banking Committee. He’ll be back on Capitol Hill today speaking to U.S. House members. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

Half and Half: Hours after investment giants Citigroup C and Goldman Sachs GS told investors they were raising their recession expectations, one more expert weighed in with a projection of a slightly higher than 50% chance of recession over the next four quarters. That would be Michael Kiley, a senior economist with the Federal Reserve. According to The Wall Street Journal, Kiley published a paper on Tuesday that found a two-thirds probability of a downturn over the next two years. Citigroup raised its own projection to 50%, while Goldman doubled its 12-month chance of a recession to 30%.

Crowdfunding for Crypto? As bitcoin lost another 4.84% by late yesterday afternoon to finish just under the $20,000 mark, news from the rest of the digital currency space didn’t get much better. Earlier yesterday, the CEO of crypto exchange firm FTX US Derivatives offered a multimillion-dollar bailout (mostly in digital currency) to help struggling banking platform BlockFi and digital asset brokerage Voyage Digital.

Meanwhile, Coinbase (COIN) closed down 9.71% after rival Binance.US said it plans to drop certain trading fees for its customers. The impact of the Fed’s recent rate hikes, the collapse of stablecoin terraUSD weeks ago, and now new competitive pressures have reset crypto’s volatility meter—with no immediate stability in sight.

Closer to Home: The mortgage slowdown has clearly arrived at JPMorgan Chase (NYSE: JPM) as the company confirmed a Bloomberg report late yesterday that it’s laying off or reassigning hundreds of workers in its mortgage operation. “Our staffing decision this week was a result of cyclical changes in the mortgage market,” said the company. Still, there’s some activity out there. The Mortgage Bankers Association reported on Wednesday an increase in mortgage applications for the second week in a row.

Notable Calendar Items

June 24: Michigan Consumer Sentiment, New home sales, and earnings from CarMax KMX

June 27: Durable Goods Orders, pending home sales, and earnings from Nike NKE

June 28: CB Consumer Confidence

June 29: Gross domestic product (GDP) and earnings from Paychex and PAYX General Mills GIS

June 30: Initial Jobless Claims, PCE inflation, Chicago PMI, and earnings from Walgreens Boots WBA, Micron MU, and Constellation Brands STZ

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Unsplash

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.