(Friday Market Open) The U.S. dollar was rising ahead of the market open as the British pound slid on better-than-expected economic news.

Potential Market Movers

Great Britain reported a smaller-than-expected contraction in gross domestic product (GDP) and industrial production. Despite the positive news that should allow the Bank of England to continue increasing rates to combat inflation, the pound fell against the dollar.

Additionally, the euro fell against the dollar despite rising inflation in France and higher industrial production gains in the Eurozone. These are signs that the European Central Bank has more work to do in combatting inflation, which should be strengthening the euro.

The London FTSE 100 was up 0.37% and the Stoxx Europe 600 was up 0.11% over night. In fact, European markets were in the green across the board with the German DAX rising 0.5% and the French CAC 40 increasing 0.21%.

The stronger dollar doesn’t appear to be slowing down U.S. markets because equity index futures were higher in all three major indexes. The strong dollar has been a drag on mega-cap stocks. Additionally, the Cboe Market Volatility Index (VIX) remains below 20 suggesting that investors aren’t concerned about the bounce.

The 10-year Treasury yield (TNX) was lower by three basis points in premarket action, taking the yield down to 2.85%. Falling yields usually have depressive effect on the dollar as well.

U.S. import prices came in at -1.4% in July, lower than the -1.1% forecasted. Falling fuel prices helped drive results as fuel costs fell 7.5%.

One driver of the higher dollar could be that the U.S. House of Representatives is expected to pass the $2.2 trillion Inflation Reduction Act, which increases spending on many climate-related projects which could help to reduce the long-term costs of oil and health care initiatives that are aimed to decrease costs for patients. However, critics of the bill believe it will be inflationary despite its name because the money supply will be expanded through issuing of unfunded debt in order to pay for the programs. This approach tends to be inflationary. However, tax hikes in the bill could help to reduce some of the money supply expansion. Additionally, much of the spending won’t take place immediately.

After the market open, investors will see the preliminary Michigan Consumer Sentiment and Inflation Expectations reports. The hope is that consumers are starting to see — or at least feel more confident — that inflation is going to subside soon.

After Thursday’s close, a couple of earnings reports were making news. Illumina (ILMN) reported that it fell short on earnings and revenue estimates and then offered a bleak earnings outlook that caused the stock to fall more than 20% in after-hours trading. The gene-sequencing company forecasted full-year revenue growth of 4% to 5% due to unfavorable exchange rates, delays in lab expansions, and issues in acquiring capital.

Electric truck maker Rivian (RIVN) reported a larger-than-expected loss despite higher-than-expected revenues. However, the company was able to maintain its full-year production estimate. About two weeks ago, Rivian announced plans to reduce its workforce by 6%. It has also plunged 80% from its peak in November and has been the cause of large investment losses for companies like Amazon (AMZN) and Ford (F). However, RIVN was slightly higher during the extended-hours session.

Reviewing the Market Minutes

Stocks were relatively flat on Thursday despite another softer-than-expected inflation report. The July Producer Price Index (PPI), which measures wholesale inflation, fell 0.5% for the month. However, it grew 5.8% year over year (YOY). Core PPI increased 0.2% for July, but that was lower than the forecasted 0.4%. Core PPI was on target YOY at 7.6%. Lower wholesale inflation should translate into lower input costs for companies, which could mean wider profit margins.

The Dow Jones Industrial Average ($DJI) ticked slightly higher at 0.08%, while the S&P 500® index (SPX) ticked lower at 0.07%. The Nasdaq ($COMP) fell a little further, closing 0.58% lower on the day. Despite the final numbers, NYSE advancers outpaced decliners nearly 1.5-to-1, suggesting that investors may have been a little more bullish than what was reflected in the indexes.

The Dow was boosted for the second day in a row by Disney (DIS). On Wednesday, the stock rallied 3.98%, making it the top stock among Dow components. Yesterday, it rallied 4.68% on better-then-expected earnings that was driven by its theme parks performance and making it the top Dow component once again.

Investors appeared to be looking to take on a little more risk as the Russell 2000 (RUT) small-cap index beat the major indexes by closing 0.3% higher. The S&P Mid-Cap 400 Index outperformed all the indexes, rising 0.6%.

The energy sector was the top performer with the Energy Select Sector Index closing 3.22% higher on the day. It was helped by WTI crude oil futures rising 2.7% to settle at $94.33 per barrel and natural gas futures jumping 9.1% higher.

The bond markets had a much bigger reaction to the PPI report than stocks did. The 10-year Treasury yield (TNX) tumbled to 2.74% and then rallied to close at 2.89%, gaining 10-basis points.

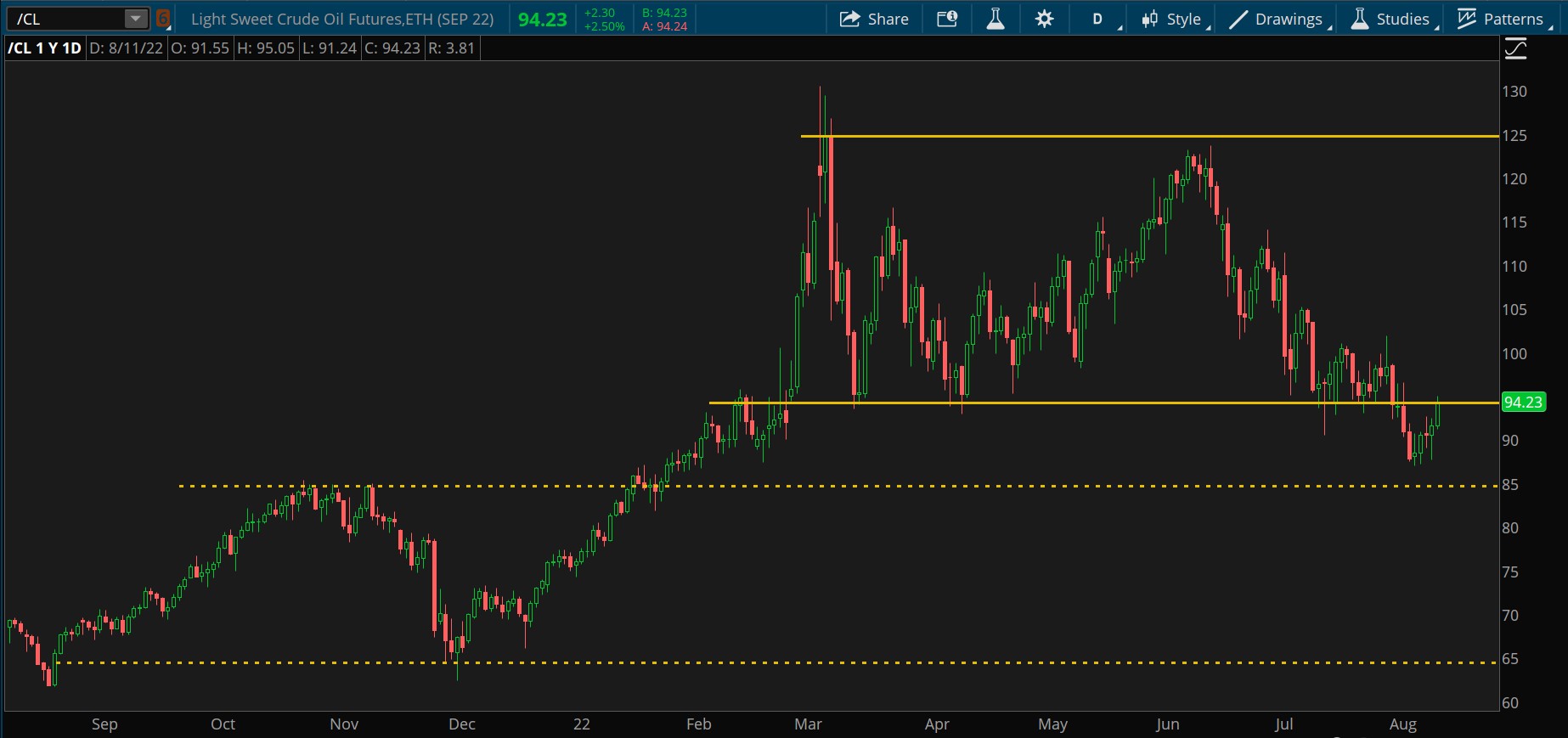

CHART OF THE DAY: OIL LEVELS. The WTI crude oil futures (/CL—candlesticks) broke support last week and retested old support as resistance on Thursday. If resistance holds, oil prices could fall to the November highs around $85. Another charting technique for setting price targets is to measure previous range and subtract it from the old support level. Using this method, a long-term target would be around $65. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

OILED UP: Oil prices commonly find a top in late summer and sell off in anticipation of the cooler months when North Americans are traveling less. If oil prices follow this cycle, Q3 earnings could worsen for the energy sector and the S&P 500 has a whole.

Q2 earnings season is on track for a blended earnings growth rate of 6.7% for the S&P 500, according to FactSet. However, the energy sector growth rate of 299% is skewing the results. When energy is removed, the earnings growth rate for the S&P 500 is -3.7% YOY. In fact, only six of the 11 sectors have positive growth rates YOY.

For the 2022 calendar year, the blended growth rate for the S&P 500 looks a little better. With energy it’s 8.9%, but without energy, it falls to 2.4%.

KEEP ON TRUCKIN’: The American Trucking Association reported that the average compensation for truckdrivers was just shy of $70,000 last year. Total compensation includes salaries, bonuses, and benefit packages. This represents a pay raise of 11% over the prior year. The tight labor market caused compensations to rise because the companies had offered incentives to bring in new drivers and retain existing driver in order to keep supply chains running.

Last week’s Employment Situation report showed an increase of 21,000 jobs in the transportation and warehousing sector, suggesting that there are still jobs for truckdrivers.

Wednesday’s Consumer Price Index (CPI) reported that transportation costs fell 0.5% in July but were up 9.2% YOY, which is likely cutting into company profits. Companies like Walmart WMT and Sysco SYY that have large in-house fleets are likely feeling the pinch on compensation.

TRADER SENTIMENT: The latest Charles Schwab Trader Sentiment Survey revealed that the biggest concern for traders going into the third quarter was inflation. However, recession was the second-highest concern with 71% saying that a recession was “likely” to “highly likely” to occur. Of those that expected a recession, 24% anticipated it would last 3 to 6 months, 39% expected it to last 6 to 12 months, and 28% said 1 to 3 years. Only one in five traders said they were moving money out of stocks as a way to hedge against a continued market downturn or recession.

Notable Calendar Items

Aug 15: Earnings from James Hardie Industries JHX and ZipRecruiter ZIP

Aug 16: Building permits, Housing Starts, and earnings from Walmart WMT, Home Depot HD, and TJX Companies TJX

Aug 17: Retail sales and earnings from Cisco CSCO, Lowe’s LOW, Analog Devices ADI, Target TGT, and Macy’s M

Aug 18: Philadelphia Fed Manufacturing Index, Existing Home Sales, and earnings from Estee Lauder EL, Applied Materials AMAT, NetEase NTES, and Ross Stores ROST

Aug 19: Earnings from Deere DE, Foot Locker FL, and Buckle BKE

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Unsplash

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.