(Friday Market Open) Equity index futures headed lower before the open as investors consider this week’s competing Fed messages about how high September’s rate hike could go. It’s also a big options expiration day, so be prepared for possible turbulence before the close.

Potential Market Movers

The last big earnings stories of the week featured one big hit and a miss.

- Foot Locker (FL) rocketed 23.67% before the bell on an earnings beat and news that former Ulta Beauty (ULTA) CEO Mary Dillon will become FL’s new CEO on September 1.

- Deere (DE) was off 3.56% premarket after cutting its full-year forecast; the company reported below-estimate earnings for the quarter on above-consensus revenues.

Shares of fashion retailer Buckle (BKE) were up 4.59% premarket in anticipation of its earnings announcement later in the day.

As summer winds down, there’s still a month to go until the next Federal Open Market Committee (FOMC) meeting and rate decision, with plenty of conjecture to come until it’s clear how big the almost-certain rate hike will be.

Near the open, S&P 500 futures were off 0.86%, Dow Jones futures were down 0.63% and Nasdaq composite futures were off 1.01%. The 10-year Treasury yield edged up slightly to 2.967% while WTI crude oil was down 1.62% to $89.03 a barrel.

Elsewhere in the market, the dramatic saga that is Bed Bath & Beyond (BBBY) continued with a 35% slide in premarket trading after investor and Chewy.com founder Ryan Cohen confirmed the sale of his 7.78-million-share stake in the company yesterday, which sent BBBY down 30% by the close. Recent reports have noted that Cohen’s past purchases of call options had likely fueled buying in BBBY’s stock over the past few weeks.

Starbucks (SBUX) lost 1.08% premarket as executive reshuffling continues under Howard Schultz in his interim CEO role. The international coffee chain announced Thursday that it was eliminating the company’s chief operating officer post, after the previous CEO retired earlier this year.

Meanwhile, crypto winter could be back. Bitcoin, the largest cryptocurrency by market cap, plunged below $22,000 Friday to a two-month low.

And in a sign that people might want to stock up on sweaters for the winter, natural gas prices are now at 14-year highs driven by extreme weather patterns in Europe and the Far East.

Reviewing the Market Minutes

Mixed economic data and seemingly mixed opinions from Federal Reserve officials on the future pace of rate hikes made for a choppy session Thursday, though all major stock indexes finished slightly ahead.

The S&P 500® index (SPX) advanced 0.23%, the Dow Jones Industrial Average ($DJIA) moved upward a slight 0.06%, the Nasdaq ($COMP) gained 0.21%, and the Russell 2000 (RUT) added 0.68%.

Meanwhile, the U.S. Dollar Index ($DXY) finished at 107.5, the highest level in a month.

After better-than-expected numbers before the open on weekly jobless claims and the Philadelphia Fed’s Manufacturing Index, the National Association of Realtors reported that U.S. existing home sales fell in July for the sixth straight month, the longest downward movement since 2015 not including the first three months of the pandemic. Previously owned home sales fell 5.9% in July from June to a seasonally adjusted annual rate of 4.81 million.

Though homeowners may not be happy with those results, the Fed might consider the housing slowdown as one more sign their efforts to slow inflation are finally producing consistent results. The central bank’s July minutes released on Tuesday gave investors some relief that, while rate hikes would likely continue into 2023, the Fed could moderate based on fresh data along the way.

Yet on Thursday, two central bank officials indicated in separate appearances that there’s still a healthy debate on the direction of rate increases. In a Wall Street Journal interview published yesterday, St. Louis Fed President James Bullard remained hawkish for a 75-basis-point increase at the next Federal Open Market Committee meeting and rate announcement scheduled for September 21. Meanwhile, Kansas City Fed President Esther George seemed to take a more cautious stance in public comments yesterday about the size and pace of rates going forward, saying the central bank has already “done a lot” and should be mindful that its policy decisions “operate on a lag.”

Technology and semiconductor sectors moved higher, led by Wolfspeed (WOLF), which is up more than 30% after better fourth-quarter results and raising its guidance for the coming year. Cisco (CSCO) shares gained another 5.81% on Thursday after an above-estimates performance on revenue and profits and a better-than-expected forecast for its coming year.

Kohl’s (KSS) shares lost another 7.72% by Thursday’s close after trimming its annual earnings guidance again on how inflation appears to be hurting its core middle-market customers.

After gaining 2.14% during yesterday’s regular session, Applied Materials (AMAT) beat on sales and earnings and rose another 1.92% in after-hours trading. Ross Stores (ROST) lost 0.97% in the extended session after missing on revenues but finishing ahead of earnings estimates.

In anticipation of today’s earnings announcements, shares of Deere (DE) gained 0.90%, Foot Locker (FL) lost 1.45%, and Buckle (BKE) fell 1.45% by Thursday’s close.

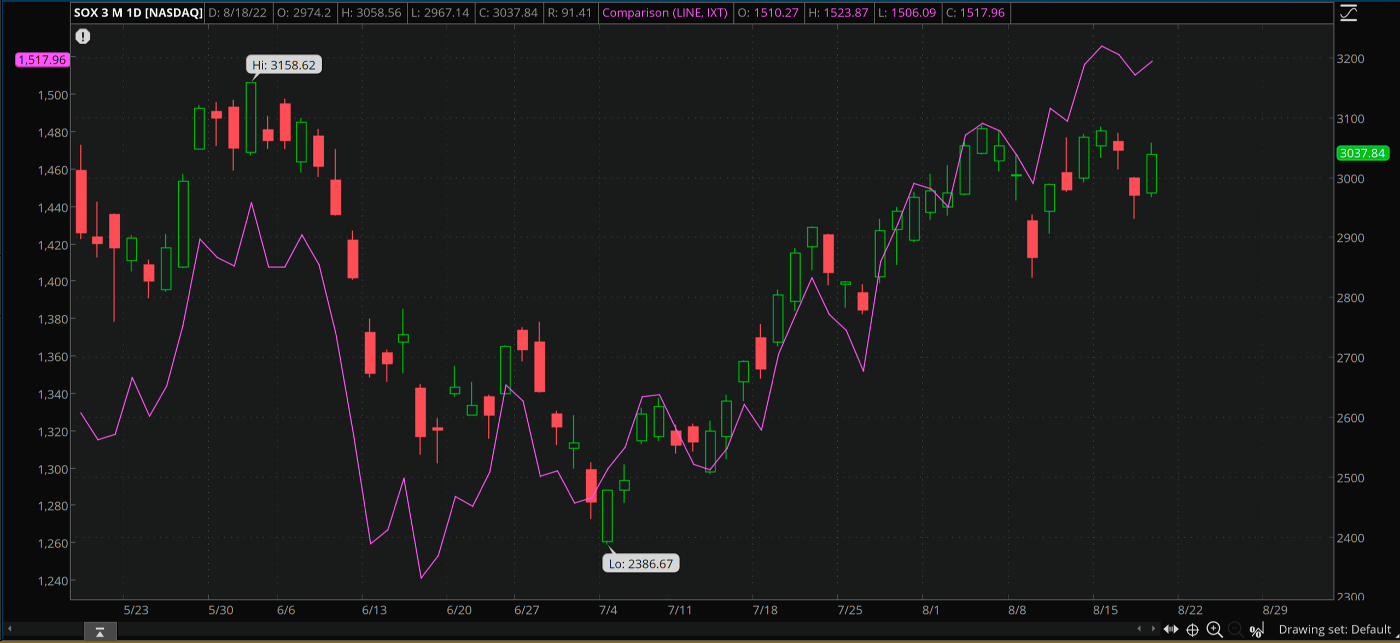

CHART OF THE DAY: WILL CHIPS DIP—OR RIP? With renewed reports on uneven supplies of semiconductor products for markets in need (think autos) or oversupply (computers), the PHLX Semiconductor Index’s (SOX—candles) move upward on Thursday was attributed largely to standout earnings by Wolfspeed (WOLF) and reports that Qualcomm (QCOM) may re-enter the server market. The Technology Select Sector Index (IXT) rode higher on positive results from Cisco (CSCO) and NetEase (NTES). Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

LAYOFFS ARE BACK? A survey published Thursday by global consultant PwC said that half of executives and corporate board members were either reducing headcount or thinking about it, while 52% said they were freezing new hiring. After interviewing more than 700 U.S. executives and board members, PwC also reported that more than 40% were rescinding job offers, and a similar amount were reducing or eliminating sign-on bonuses that were popular in the before times of the tight job market. In its coverage of the results, Bloomberg pointed out one bright spot—about two-thirds of the firms are raising pay or expanding mental health benefits, which might come in handy if payrolls are about to shrink.

GHOSTING THE CLOSING: Redfin says purchase agreements between homebuyers and sellers are falling off the rails at the highest levels since the beginning of the COVID-19 pandemic. The real estate firm reported that nationally 63,000 home-purchase agreements fell through in July, equal to 16.1% of homes that went under contract that month. With housing market clearly cooling, things seem to be getting tense—Redfin said that buyers are “more likely to call a deal off if a seller refuses to bring the price down or make requested repairs.”

INFLATIONARY BABIES: The cost of raising kids through high school just topped $300,000, and yes, we have 40-year-high inflation to thank for that. The Wall Street Journal reported Brookings Institution data this morning that a married, middle-income couple with two children would spend $310,605—averaging $18,271 a year—to raise a younger child born in 2015 through age 17. According to the Journal, that calculation uses “an earlier government estimate as a baseline, with adjustments for inflation trends.” Those suddenly thinking about buying a refrigerator lock may not be alone.

Notable Calendar Items

Aug 22: Earnings from Palo Alto Networks (PANW)

Aug 23: New home sales and earnings from Intuit (INTU), Medtronic (MDT), Advance Auto Parts (AAP), Dick’s Sporting Goods (DKS), and Toll Brothers (TOL)

Aug 24: Durable goods orders, Pending home sales, and earnings from Nvidia (NVDA), Salesforce.com (CRM), Snowflake (SNOW), and Autodesk (ADSK)

Aug 25: Gross domestic product (GDP) and earnings from Dollar General (DG), Workday (WDAY), Dollar Tree (DLTR), Ulta Beauty (ULTA), Burlington Stores (BURL), and Gap (GPS)

Aug 26: PCE price index, Michigan Consumer Sentiment, Personal Income, and earnings from Marvell Technology (MRVL) and Dell (DELL)

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.