(Tuesday Market Open) U.S. equity index futures are pointing to a higher open despite economic turmoil overseas.

Potential Market Movers

Global stocks fell Monday and the euro slid to a 20-year low amid recession fears and fallout from the ongoing Nord Stream shutdown. However, news out of China that the country plans to accelerate its stimulus program of providing liquidity to its banks helped to turn stocks around. The Shanghai Composite rose 1.4% and the Europe Stoxx 600 climbed 0.4%. The London FTSE 100, German DAX, and the French CAC 40 respectively rose 0.23%, 0.95%, and 0.46%.

The futures market energy complex was already experiencing a lot of volatility ahead of the opening bell after OPEC+ announced a surprise production cut. WTI crude oil futures rose more than 3.5% overnight and then surrendered most of those gains before the U.S. markets opened. While OPEC+ may be cutting production with hopes of raising oil prices, more than 70 Chinese cities have placed their citizens under full or partial lockdown since late August which is keeping oil demand and prices lower.

The U.K.’s new prime minister Liz Truss plans to help Britons with higher energy prices by essentially freezing energy bills as part of a $130 billion rescue package. However, the move could be risky. Price caps often reduce incentives for other companies to increase production or move into the space to provide more supply, which can bring down prices.

Despite all the news overseas, the S&P 500 futures were 0.60% higher in premarket action, but there are reasons to be concerned that the move may not have “staying power.” The Cboe Market Volatility Index (VIX) was also higher in premarket trading despite the move in stock futures. The 10-year Treasury yield (TNX) rose five basis points to 3.24% which is likely to suppress growth stocks.

And the U.S. Dollar Index ($DXY) rose 0.45% to a new 52-week high, which could be a drag on U.S. multinational companies.

After the market open, investors will get data on the U.S. service sector with the ISM Nonmanufacturing PMI.

Reviewing the Market Minutes

The last investors watching Friday’s pre-Labor Day session had little to cheer them on their way to the beach.

Though August’s jobs report sparked a brief, 370-point rally in the Dow Jones Industrial Average ($DJI), interest rate worries returned quickly, sending the markets backward. Then by midday, Russian-owned Gazprom announced that a technical problem would force it to keep its Nord Stream natural gas pipeline shuttered until further notice. It was set to reopen on Saturday after what had been called a three-day maintenance shutdown.

Few analysts appeared to believe Russia’s explanations Friday after months of continued service problems on the key European energy artery, mainly because they’ve coincided with escalating trade sanctions and security tensions over Russia’s war against Ukraine. The Energy Select Sector Index advanced 1.77% by the close, representing the only industry sector to finish ahead in Friday’s low-volume session. Communications services, real estate and health care were the top three sectors in the red.

With these developments and overnight word of new COVID-19 lockdowns in China, leading stock indices finished down for their third consecutive week. Friday’s closing Dow was off by 1.1%, the same amount as the S&P 500® index (SPX), while the Nasdaq ($COMP) slid 1.3% for its sixth losing session in a row in its longest losing streak since 2019.

Since Federal Reserve Chairman Jerome Powell shook the markets August 26 with his continued hawkish comments on the central bank’s plans to curb inflation, both the Dow and the S&P 500® index (SPX) have lost over 3% respectively while the Nasdaq has lost over 4% in value. The Federal Open Market Committee’s next two-day meeting is scheduled to wrap up with the body’s latest rate decision on September 21.

Before Friday’s open, the government said the U.S. added 315,000 jobs in August, higher than the forecasted 300,000 but still within estimates while the unemployment rate nudged up 0.2% to 3.7%.

Former Fed vice chairman Roger Ferguson told CNBC that he didn’t believe the latest job numbers indicated the Fed was any closer to a soft landing for the economy, but by day’s end, CME FedWatch Tool showed a 56% probability of a 75-basis-point rate hike at the Fed’s September meeting, down from 75% on Thursday.

Despite current turbulence, other signs of a cooling U.S. economy are continuing to mount. Behind Friday’s jobs and energy news was the release of U.S. factory orders data, which actually fell for the first time in 10 months. The Commerce Department said July’s numbers fell 1% after increasing by a revised 1.8% in June. Expectations were for a 0.2% gain during the month.

After climbing as high as 27 during the session, Cboe Market Volatility Index (VIX) finished for the long weekend just above 25.

Lululemon LULU followed up above-estimate earnings and revenue results and better guidance with an additional gain of 6.7% on Friday. The high-end fitness apparel company rocketed more than 9% ahead of the opening bell.

Broadcom AVGO gained 1.67% after reporting better-than-expected earnings and revenue as well as forward guidance above expectations.

Chobani, the yogurt maker, withdrew its November application to go public on the Nasdaq citing current market conditions. According to FactSet, second-half 2022 initial public offerings (IPOs) were down over 90% from the year-ago period.

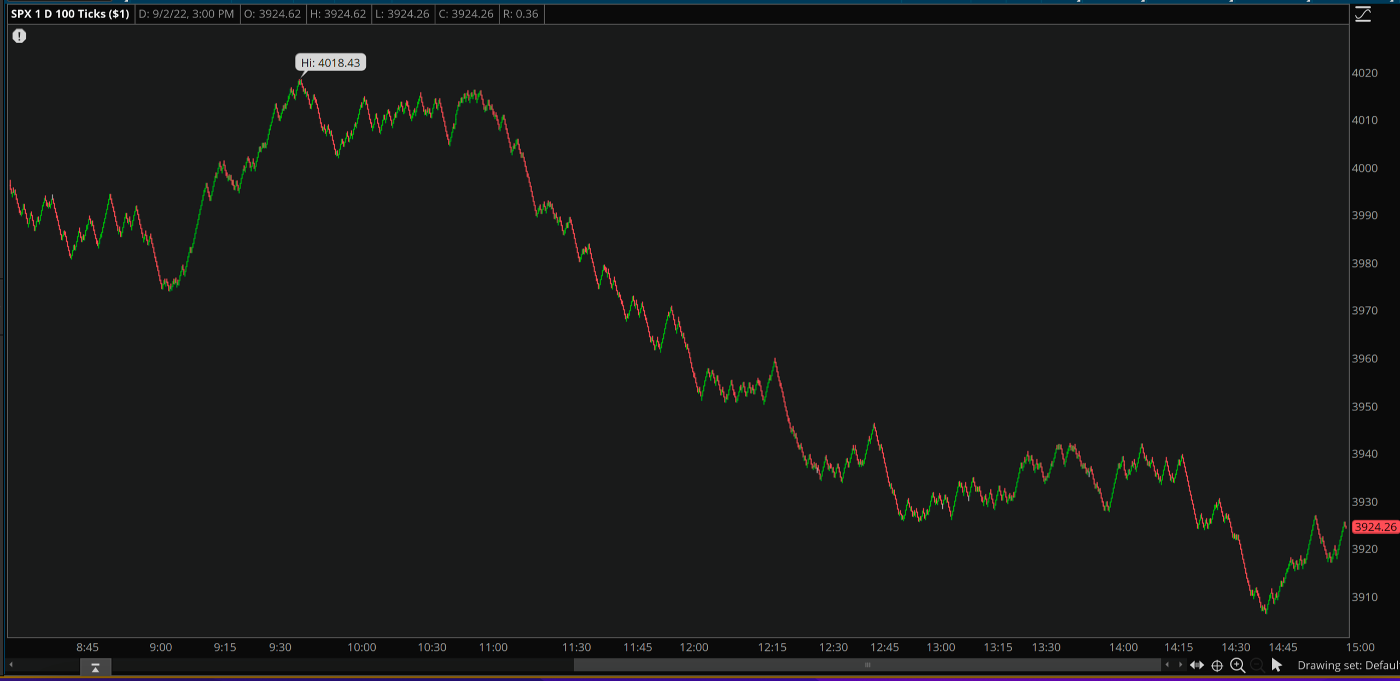

CHART OF THE DAY: OFF THE FLOOR. The S&P 500® index (SPX) managed to close above 3,900 Friday, but many wonder if September’s historically poor market conditions and emerging global market developments could soon have the broad index testing June lows. Data Sources: ICE, S&P Dow Jones Indices. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

NEW PRICE! If you haven’t seen price-drop signs in front of a home for sale in a while, keep watching. Redfin reports that the average home sold for less than its price for the first time in 17 months as of August 28.

TIME ON MARKET: The National Association of Realtors reports that during August, the typical home spent 42 days on the market, the most since June 2020, though still ahead of pre-pandemic levels.

NOT A CRASH: Moody’s chief economist Mark Zandi told MarketWatch on Friday that rising mortgage rates and falling selling prices indicate that the housing market is heading toward a “correction,” but not a crash. Zandi said he expects nationwide prices to decline in the low single-digits, around 5%.

Notable Calendar Items

Sep 7: U.S. Trade Balance, Federal Reserve Beige Book, and earnings from GameStop (GME), MongoDB (MDB), and UiPath (PATH)

Sep 8: Earnings from Zscaler (ZS), SentinelOne (S), National Beverage (FIZZ), and Korn Ferry (KFY)

Sep 13: August Consumer Price Index (CPI) and earnings from United Natural Foods (UNFI)

Sep 14: August Producer Price Index (PPI)

Sep 15: August U.S. Retail Sales, Philadelphia Fed Manufacturing Index and earnings from Oracle (ORCL), and Adobe (ADBE)

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.