A Real Estate Investment Trust (REIT) is a company that owns, operates, or finances income-generating real estate. REITs provide investors with an opportunity to invest in real estate without directly owning properties, offering advantages such as regular income through dividends, portfolio diversification, potential tax benefits, professional management, and liquidity through publicly traded shares.

While the REIT industry has struggled since the 2020 Covid pandemic, underperforming the stock market, the three REITs I talk about here have outperformed the industry and the broad market.

Brookfield Infrastructure Partners BIP, EastGroup Properties EGP, and Iron Mountain IRM all have high Zacks Ranks, and market-beating performances. Additionally, they are from three different industries within the REIT sector offering a diverse range of investment options.

Brookfield Infrastructure Partners

Brookfield Infrastructure Partners is a leading global infrastructure company that owns and operates a diversified portfolio of high-quality infrastructure assets. With a focus on sectors such as utilities, transportation, energy, and data infrastructure, the partnership aims to deliver long-term, stable cash flows and attractive returns to its investors.

Leveraging its expertise in asset management, Brookfield Infrastructure Partners actively seeks investment opportunities that offer growth potential and contribute to the essential infrastructure needs of societies around the world.

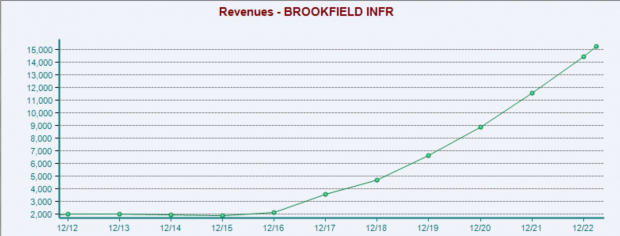

BIP annual revenue has exploded since 2016, growing from $2.1 billion to over $15 billion today. Brookfield's reputation as an asset manager has grown to be one of the most respected in the industry, and rightfully so. This strong reputation has allowed them to grow AUM and purchase new infrastructure assets.

Image Source: Zacks Investment Research

One of the best aspects of owning REITs is the regular dividend payments. BIP offers a dividend yield of 4.3%, which has been increased by an average of 3.1% annually over the last five years.

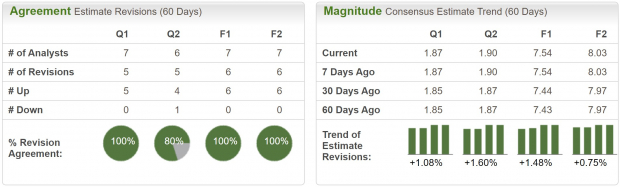

Brookfield Infrastructure Partners is trading at a one-year forward earnings multiple of 11.7x, which is below the industry average of 14.3x, and below its 10-year median of 12x. Considering BIP is a premier asset manager that has outperformed the market it is quite compelling that it can be owned at a valuation below the industry.

Image Source: Zacks Investment Research

EastGroup Properties

EastGroup Properties is a self-administered real estate investment trust focused on ownership, acquisition, and selective development of industrial properties.

The company pursues a three-pronged investment strategy that includes: the acquisition of industrial properties at favorable initial yields, with opportunities to improve cash flow performance through management; selective development of industrial properties in markets where they already have a presence and where market conditions justify such investments; and the acquisition of existing public & private companies.

EastGroup focuses on buying properties in local economies growing faster than the US economy, with its top holdings in Texas (35%), Florida (24%), California (20%), Arizona (7%), and North Carolina (6%). EGP owns a total of 57 million square feet, with multi-tenant properties, and a focus on last mile e-commerce in supply constrained markets.

EastGroup currently has a Zacks Rank #2 (Buy), indicating upward trending earnings revisions. Analysts have nearly unanimously upgraded earnings estimates across the board. Current quarter earnings are expected to grow 9% YoY to $1.87, and sales are expected to climb 15% to $136 million over the period as well.

Image Source: Zacks Investment Research

EGP is trading at a one-year forward earnings multiple of 20x, which is above the industry average of 14.3x, and just below its 10-year median of 20.5x. The company is a lean and fast-growing company, which explains the premium valuation, however because of the geographic location of its properties, and the industries they service, a higher valuation may be justified.

EGP has a 3.1% dividend yield, which has been raised by an average of 14.7% annually for the last five years.

Image Source: Zacks Investment Research

Iron Mountain

Iron Mountain is a global information management company founded in 1951. Originally specializing in secure storage for vital records, the company expanded its services to include offsite tape storage, document imaging, data centers, and digital archiving.

Today, Iron Mountain offers comprehensive information management and storage solutions, serving 225,000 customers from various industries through its 1400 facilities.

IRM is as steady as they come. Current quarter sales are expected to grow 5% YoY and FY23 sales are expected to grow 8.2% YoY. Current quarter earnings are projected to climb 4.3%, while FY23 earnings are expected to grow 4.2%.

Iron Mountain also maintains a very well positioned balance sheet. They are running the lowest level of leverage since 2017, and currently have more than $1 billion of liquidity. Additionally, the current weighted average interest rate they pay on debt is 5.3% of which 75% is at a fixed rate.

IRM is trading at a one-year forward earnings multiple of 14.2x, which is right in line with the industry average, and below its 10-year median of 16x. Iron Mountain pays a dividend yield of 4.6% and has not altered it over the last five years.

Image Source: Zacks Investment Research

Bottom Line

Above we have identified three compelling REIT investments, each of which has managed to succeed during a challenging period in the industry. With IRM focusing on the digital economy, EGP covering industrial and e-commerce fulfillment, and BIP giving exposure to a range of infrastructure, these REITs allow shareholders access to alternative investment options.

Image by Kostiantyn Li on Unsplash

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.