Lululemon athletica inc. LULU reported first-quarter fiscal 2024 results, wherein revenues and earnings surpassed the Zacks Consensus Estimate and improved year over year. The results were driven by strong momentum in the international business as its products resonate well with customers. Innovative product offerings and progress on optimizing the U.S. product assortments also aided the results.

The company has been on track with the Power of Three X2 growth plan. LULU outlined the guidance for the fiscal second quarter. Moreover, it reiterated the revenue guidance but raised its EPS view for fiscal 2024.

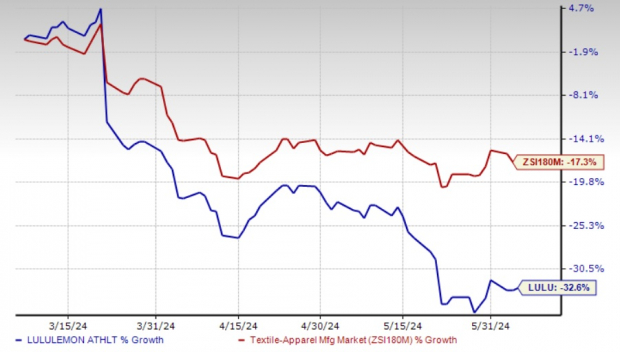

Shares of lululemon gained 9.7% in the after-market trading session on Jun 5, mainly on strong first-quarter fiscal 2024 results and a solid international performance. The Zacks Rank #4 (Sell) company's shares have lost 32.6% in the past three months compared with the industry's decline of 17.3%.

Image Source: Zacks Investment Research

Q1 Details

lululemon's fiscal first-quarter earnings of $2.54 per share increased 11.4% year over year and beat the Zacks Consensus Estimate of $2.38.

The Vancouver, Canada-based company's quarterly revenues advanced 10% year over year to $2.209 billion and outpaced the Zacks Consensus Estimate of $2.198 billion. On a constant-dollar basis, net revenues improved 11% year over year in the fiscal first quarter. Net revenues grew 3% in the Americas (up 4% on a constant-dollar basis) and 35% internationally (up 40% on a constant-dollar basis).

Total comparable sales rose 6% year over year and 7% on a constant-dollar basis. Comparable sales in the Americas were flat year over year. Internationally, comparable sales increased 25% and 29% on a constant-dollar basis.

lululemon athletica inc. Price, Consensus and EPS Surprise

lululemon athletica inc. price-consensus-eps-surprise-chart | lululemon athletica inc. Quote

In the store channel, the company's total sales increased 12%. Digital revenues improved 8% year over year and contributed 41% to the total revenues.

Gross profit improved 11% year over year to $1.3 billion. Also, the gross margin expanded 20 basis points (bps) to 57.7%, driven by a 120-bps rise in the product margin due to lower product costs, airfreight costs and inventory provisions, offset by a 50-bps increase in markdowns. The increase in product margin was partly negated by 70-bps deleverage on fixed costs and 30-bps deleverage on foreign exchange. We expected the gross margin to be flat year over year at 57.5% for the fiscal first quarter.

SG&A expenses of $842 million increased 12.7% from the year-ago quarter. SG&A expenses, as a percentage of net revenues, of 38.1% were up 70 bps from the 37.4% reported in the prior-year quarter.

Our model predicted SG&A expenses to rise 13.8% year over year for the fiscal first quarter, with a 130-bps increase in the SG&A expense rate to 38.7%.

Operating income rose 7.8% year over year to $433 million in the fiscal first quarter. The operating margin of 19.6% contracted 50 bps year over year. Our model predicted a 2.9% year-over-year increase in operating income. We estimated the operating margin to decline 130 bps year over year to 18.8%.

Store Update

In the fiscal first quarter, LULU opened five and closed five stores. The company also completed three store optimizations. As of Apr 28, 2024, it operated 711 stores.

For the second quarter of fiscal 2024, lululemon plans to open 14 company-operated stores. For fiscal 2024, the company anticipates opening 35-40 company-operated stores and completing approximately 40 co-located optimizations, contributing to overall square footage growth in the low double digits. The store openings in fiscal 2024 will include five to 10 stores and 15-20 optimizations in the Americas. The rest of the store openings in fiscal 2024 are likely to occur in the international markets, primarily in China Mainland.

Financials

lululemon exited the quarter with cash and cash equivalents of $1.9 billion and stockholders' equity of $4.2 billion. At the end of the quarter, LULU had $400 million remaining under its committed revolving credit facility. Its inventories decreased 15% year over year to $1.3 billion.

In the fiscal first quarter, lululemon repurchased 0.8 million shares for $296.9 million. On May 29, 2024, the company approved a $1-billion increase to its share repurchase program. Including this, as of Jun 5, 2024, it had $1.7 billion remaining under its current share repurchase authorization.

Outlook

For the second quarter of fiscal 2024, management anticipates net revenues of $2.4-$2.42 billion, indicating 9-10% year-over-year growth. The company expects gross margin to contract 100-110 bps year over year, driven by deleverage on fixed costs and ongoing investment in the multi-year distribution center project. It expects the product margin to be relatively flat year over year in the fiscal second quarter, including an increase in markdowns. However, it expects the increase in markdowns to be lesser than it witnessed in first-quarter fiscal 2024.

SG&A, as a percentage of sales, is likely to leverage 40-60 bps year over year due to improved regional penetration, a shift in the timing of certain brand campaign-related spends that occurred in the second quarter of last year to the first quarter of this year, the top line growth and ongoing prudent expense management.

The operating margin is expected to contract 50-60 bps year over year in the fiscal second quarter. EPS in the fiscal second quarter is expected to be $2.92-$2.97, whereas it reported $2.68 in the prior-year quarter. It estimates an effective tax rate of 30% for the fiscal second quarter.

The company expects dollar inventory to decline in the mid-teens in the fiscal second quarter. It expects an increase in dollar inventory in the second half of fiscal 2024 against a decline reported in the prior year.

For fiscal 2024, LULU anticipates net revenues of $10.7-$10.8 billion, suggesting growth of 11-12%, or 10-11%, excluding the 53rd week in 2024.

The company anticipates the gross margin to be flat year over year. Within the gross margin, it expects both markdowns and airfreight to be relatively flat with last year. SG&A, as a percentage of sales, is likely to leverage 10 bps year over year. It expects the fiscal 2024 operating margin to be 23.3%, suggesting year-over-year growth of 10 bps.

The company projects an EPS of $14.27-$14.47, an increase from $12.77 reported in fiscal 2023. LULU anticipates an effective tax rate of 30% for fiscal 2024.

lululemon expects a capital expenditure of $670-$690 million for fiscal 2024.

As part of the Power of Three X2 growth plan, LULU estimates net revenues of $12.5 billion by 2026, implying significant growth from the 2021 reported figure of $6.25 billion.

Stocks to Consider

A few better-ranked stocks in the same space are Hanesbrands HBI, Crocs Inc. CROX and Guess? Inc. GES.

Hanesbrands engages in the design, manufacture, sourcing and sale of apparel essentials for men, women and children in the United States and internationally. It sports a Zacks Rank #1 (Strong Buy) at present.

The Zacks Consensus Estimate for Hanesbrands' current fiscal-year earnings indicates growth of 666.7% from the year-ago period's reported figure. HBI has a trailing four-quarter average earnings surprise of 10.2%.

Crocs is one of the leading footwear brands with its focus on comfort and style. It has a Zacks Rank #2 (Buy) at present.

The Zacks Consensus Estimate for Crocs' current fiscal-year earnings and sales indicates growth of 4.4% and 5.2%, respectively, from the year-ago period's reported figures. CROX has a trailing four-quarter average earnings surprise of 17.1%.

Guess designs, markets, distributes and licenses casual apparel and accessories for men, women and children, per the American lifestyle and European fashion sensibilities. The company currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Guess's current fiscal-year sales indicates growth of 11.7% from the year-ago period's reported figure. GES has a trailing four-quarter average earnings surprise of 31%.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.