The U.S. Business Services space has been benefiting from the strong fundamentals of the economy. Despite facing a record-high interest rate, a sticky inflation rate and extremely tight monetary control by the Fed, this sector has provided double-digit returns year to date.

Industries within this sector are mature, with demand for services in good shape. Revenues, income and cash flows are anticipated to gradually reach the pre-pandemic levels, aiding most industry players to pay out stable dividends.

The pandemic has changed the way industry players conduct business and deliver services. The industry's key focus is currently on channeling money and efforts toward more effective operational components, such as technology, digital transformation, data-driven decision-making and enhanced cybersecurity.

To position themselves suitably in the post-pandemic era and better utilize the opportunities that the economic recovery will bring, service providers are increasing their efforts toward formulating and reassessing strategic initiatives and targeting end markets.

The stuffing industry has been benefiting from a resilient labor market. The industry has been increasingly leveraging technology to streamline processes, enhance efficiency, and provide better services. Utilizing tech-driven recruitment methods such as AI, social media, and Big Data are on the rise.

Higher talent costs due to a competitive talent market have been a headwind for the industry. However, growing immigration is helping service providers thrive with the increased flow of foreign talent.

Our Top Picks

We have narrowed our search to five business services stocks with strong growth potential for the rest of 2024. These stocks have seen positive earnings estimate revisions in the last 60 days. Each of our picks carries either a Zacks Rank #1 (Strong Buy) or 2 (Buy).

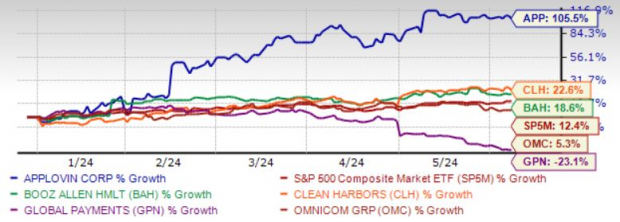

The chart below shows the price performance of our five picks year to date.

Image Source: Zacks Investment Research

AppLovin Corp. APP is engaged in building a software-based platform for mobile app developers to enhance the marketing and monetization of their apps in the United States and internationally. APP provides a technology platform that enables developers to market, monetize, analyze and publish their apps.

Zacks Rank #1 AppLovin has an expected revenue and earnings growth rate of 31.7% and more than 100%, respectively, for the current year. The Zacks Consensus Estimate for current-year earnings has improved 8.4% over the last 30 days.

Booz Allen Hamilton Holding Corp. BAH is benefiting from its Vision 2020 strategy, which has accelerated organic revenue growth, strengthened its profitability and fetched significant headcount and backlog growth.

BAH's VoLT strategy focuses on integrating velocity, leadership and technology in the process of transformation. BAH is focusing on areas such as Artificial Intelligence, advanced engineering, directed energy and modern digital platforms.

Zacks Rank #2 Booz Allen Hamilton has an expected revenue and earnings growth rate of 9.8% and 10%, respectively, for the current year (ending March 2025). The Zacks Consensus Estimate for current-year earnings has improved 1% over the last seven days.

Clean Harbors Inc.'s CLH capital investments enhance the quality of its services, and help it comply with government and local regulations. Acquisitions help CLH expand its business across multiple lines of services.

CLH has a diversified customer base, ranging from Fortune 500 companies to midsize and small public and private entities, which provides it with stable and recurring revenue sources. Consistent share repurchases boost investor confidence and aid CLH's earnings per share.

Zacks Rank #2 Clean Harbors has an expected revenue and earnings growth rate of 8.7% and 6.9%, respectively, for the current year. The Zacks Consensus Estimate for current-year earnings has improved 0.1% over the last 30 days.

Global Payments Inc. GPN has benefited from solid contributions of its merchant business. The growing demand for digital payment methods is expected to support GPN's transaction volume growth.

The EVO Payments buyout is enhancing GPN's capabilities, as evidenced by the results of recent quarters. GPN's favorable 2024 outlook further buoys investors' confidence. We expect revenues to increase 5.5% year over year in 2024.

Zacks Rank #2 Global Payments has an expected revenue and earnings growth rate of 6.4% and 11.6%, respectively, for the current year. The Zacks Consensus Estimate for current-year earnings has improved 0.1% over the last 60 days.

Omnicom Group Inc. OMC continues to focus on its internal development initiatives. Consistency and diversity of operations and increased focus on delivering consumer-centric strategic business solutions ensure persistent profitability.

OMC's bottom line is gaining from ongoing operating efficiency initiatives in real estate, back-office services, procurement and IT areas. Change in the business mix of OMC resulting from the disposition of some non-core or underperforming agencies has been aiding the bottom line.

Zacks Rank #2 Omnicom Group has an expected revenue and earnings growth rate of 6.2% and 5.8%, respectively, for the current year. The Zacks Consensus Estimate for current-year earnings has improved 1.4% over the last 60 days.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.