Carpenter Technology Corporation CRS has been gaining from strong demand in its markets, cost-cutting initiatives and efforts to preserve liquidity. Acquisitions and investing in additive manufacturing will also aid growth.

Solid Backlog & Strong Demand: In the third quarter of fiscal 2024, CRS's backlog increased 3% sequentially and 12% year over year, backed by strong booking growth. The company expects continued growth across its end-use markets, especially in Aerospace, Defense and Medical applications, which is expected to boost its fiscal 2024 results. Notably, Aerospace is gaining from the pickup in global travel. Demand continues to accelerate across all aerospace submarkets as the supply chain ramps up to meet steadily increasing travel demand.

The company's record backlog levels indicate a positive near and long-term outlook for each end-use market.

Impressive Pricing Actions & Productivity: Despite a decline in revenues due to lower shipment volumes in the third quarter of fiscal 2024. CRS achieved a solid improvement in its earnings, courtesy of improved productivity, product mix optimization and pricing actions. For 2024, CRS projects an adjusted operating profit of $339-$344 million. If achieved, 2024 would mark the company's most profitable year on record.

Carpenter Technology demonstrated its recovery growth trajectory through fiscal 2023, with increased productivity across the company's facilities. It expects to make substantial progress in fiscal 2024. To further drive shareholder returns, the company seeks to incorporate strategic initiatives to maximize market demand, accelerate growth, optimize operations and generate cash.

Upbeat Long-Term Targets: The company previously expected operating income to double from the fiscal 2019 reported level by fiscal 2027. At the end of the third quarter of fiscal 2024, it revised its objective of $460 million to $500 million in operating income from fiscal 2027 to fiscal 2026. The upside will primarily be driven by higher prices, improved product mix and increased volumes. The rise in operating income will provide significant cash flow over the next several years, adding value to the company's stockholders.

Strong Financial Position: Carpenter Technology's total liquidity (including cash and available credit facility borrowings) was $402 million at the end of the third quarter of fiscal 2024. This consisted of $53 million of cash in hand and $349 million of available borrowings under the credit facility. Its long-term debt was around $694 million at the end of the third quarter of fiscal 2024. The company has identified additional actions to preserve and manage cash and plans to deploy those actions as and when necessary.

It continues to realize price and share gains through contract renewals and price increases in its transactional business. The company continues to implement the Carpenter operating model to address any short-term challenges and increase productivity across facilities.

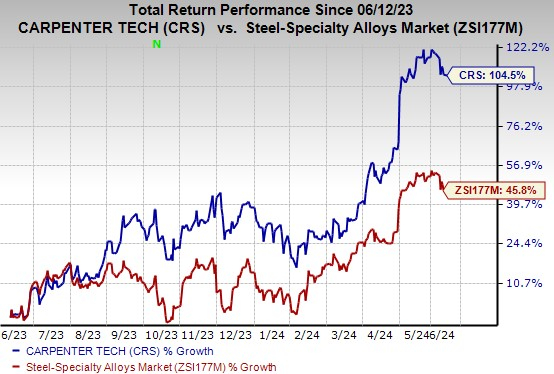

Price Performance

Shares of the company have gained 104.5% in the past year compared with the industry's 45.8% growth.

Image Source: Zacks Investment Research

Zacks Rank & Other Stocks to Consider

Carpenter Technology currently flaunts a Zacks Rank #1 (Strong Buy).

Some other top-ranked stocks from the basic materials space are Ero Copper Corp. ERO, Ecolab Inc. ECL and ATI Inc. ATI. ERO sports a Zacks Rank #1 at present, and ECL and ATI have a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Ero Copper's 2024 earnings is pegged at $1.66 per share. The consensus estimate for 2024 earnings has moved 20.3% north in the past 60 days. It has an average trailing four-quarter earnings surprise of 53.9%. ERO shares have gained 9.5% in a year.

The Zacks Consensus Estimate for Ecolab's 2024 earnings is pegged at $6.59 per share, indicating an increase of 26.5% from the prior year's reported number. It has an average trailing four-quarter earnings surprise of 1.3%. ECL shares have gained 34.5% in a year.

The Zacks Consensus Estimate for ATI's 2024 earnings is pegged at $2.41 per share. The Zacks Consensus Estimate for ATI's current-year earnings has been revised 3% north in the past 60 days. It has an average trailing four-quarter earnings surprise of 8.3%. The company's shares have rallied 65.9% in the past year.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.