The Ensign Group, Inc. ENSG is benefiting from improved service revenues, a series of acquisitions and a strong financial position. An optimistic 2024 business outlook also reinforces investors' confidence in the stock.

Zacks Rank & Price Performance

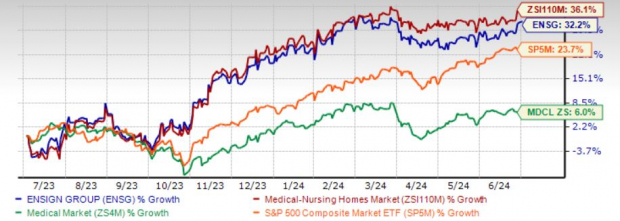

Ensign Group carries a Zacks Rank #3 (Hold) at present.

The stock has gained 32.2% in the past year compared with the industry's 36.1% growth. The Medical sector and the S&P 500 composite index have increased 6% and 23.7%, respectively, in the same time frame.

Image Source: Zacks Investment Research

Robust Growth Prospects

The Zacks Consensus Estimate for Ensign Group's 2024 earnings is pegged at $4.95 per share, indicating an improvement of 12.6% from the year-earlier reading, while the same for revenues stands at $4.1 billion, implying an 11% increase from the prior-year actual.

The consensus mark for 2025 earnings is pegged at $5.46 per share, indicating 10.2% growth from the 2024 estimate. The same for revenues is $4.5 billion, which indicates a rise of 9.4% from the 2024 estimate.

Decent Surprise History

ENSG's earnings outpaced estimates in two of the trailing four quarters and matched the mark twice, the average surprise being 0.95%.

Solid Return on Equity

Ensign Group's efficiency in utilizing shareholders' funds can be substantiated by its return on equity of 19.1% as of Mar 31, 2024, against the industry's negative return of 13.8%.

A Favorable 2024 Outlook

ENSG anticipates revenues within the range of $4.13-$4.17 billion in 2024, the midpoint of which indicates 11.3% growth from the 2023 reported figure.

Adjusted earnings per share are estimated to be between $5.29 and $5.47 this year. The midpoint of the outlook indicates 13% growth from the 2023 reported figure.

Key Business Tailwinds

Ensign Group's revenue growth is primarily driven by increasing service revenues from its enhanced healthcare services provided at skilled nursing, rehabilitation and senior living facilities. An aging U.S. population is expected to sustain the strong demand for ENSG's senior living services while the significant need for effective rehabilitation services, which help individuals return to daily activities, is anticipated to boost its Skilled Services segment's revenues.

The strong performance of ENSG's Skilled Services and Standard Bearer segments also contributes to revenue growth. Through the Standard Bearer unit, the company earns rental revenues from leasing post-acute care properties, which it has purchased, to healthcare operators under triple-net lease arrangements. These agreements are advantageous for ENSG as the company not only receives rental income but also passes the property-related costs to the tenants.

Ensign Group's inorganic growth strategy is impressive. The company is actively acquiring facilities in various U.S. regions, which allows it to collaborate with local caregiver teams. This approach provides ENSG with a deep understanding of regional needs and enables it to deliver high-quality healthcare services to underserved communities.

In June 2024, Ensign Group purchased the real estate and operations of an Arizona-based 32-bed skilled nursing facility, Wellsprings of Gilbert. Concurrently, it also acquired the operations of a skilled nursing facility in Colorado, The Springs at St. Andrews Village.

Such proactive growth initiatives expand Ensign Group's healthcare portfolio and national presence. The company currently operates 312 healthcare facilities across several U.S. states and owns 120 real estate assets. Acquisitions remain a top priority for management when deploying capital.

To support such continuous business investments, maintaining a solid financial position is essential. Ensign Group boasts strong cash reserves and sufficient cash-generating capabilities. These financial strengths also enable ENSG to reward shareholders through share buybacks and dividend payments. The company has resorted to dividend hikes for straight 21 years.

Stocks to Consider

Some better-ranked stocks in the Medical space are Tenet Healthcare Corporation THC, HCA Healthcare, Inc. HCA and Stryker Corporation SYK. While Tenet Healthcare sports a Zacks Rank #1 (Strong Buy), HCA Healthcare and Stryker carry a Zacks Rank #2 (Buy) each at present.

Tenet Healthcare's earnings surpassed estimates in each of the last four quarters, the average surprise being 56.50%. The Zacks Consensus Estimate for THC's 2024 earnings indicates a 22.5% rise from the prior-year tally. The consensus mark for THC's earnings has moved 35.7% north in the past 60 days.

The bottom line of HCA Healthcare outpaced estimates in three of the trailing four quarters and missed the mark once, the average surprise being 5.64%. The Zacks Consensus Estimate for HCA's 2024 earnings indicates a 10% rise while the same for revenues implies an improvement of 7.2% from the respective prior-year figures. The consensus mark for HCA's earnings has moved 0.5% north in the past 60 days.

Stryker's earnings outpaced estimates in each of the trailing four quarters, the average surprise being 4.93%. The Zacks Consensus Estimate for SYK's 2024 earnings indicates a 12.7% rise, while the same for revenues implies an improvement of 8.9% from the respective prior-year tallies. The consensus mark for SYK's earnings has moved up 0.8% in the past 60 days.

Shares of Tenet Healthcare, HCA Healthcare and Stryker have gained 64.8%, 6.8% and 12%, respectively, in the past year.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.