Glaukos Corporation GKOS is well-poised for growth on the back of favorable clinical trial results and a robust product pipeline. However, stiff competition is a concern.

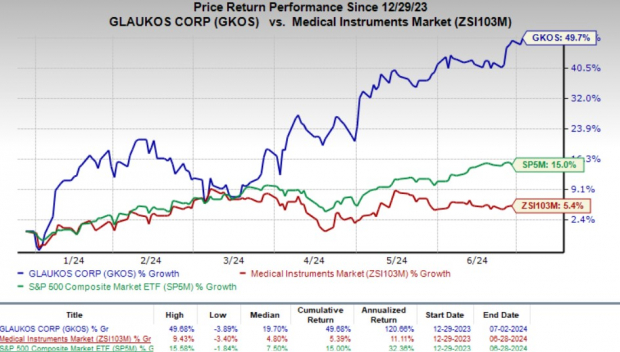

Shares of this Zacks Rank #3 (Hold) company have risen 49.7% year to date compared with the industry's 5.4% growth. The S&P 500 Index has also increased 15% in the same time frame.

Glaukos, with a market capitalization of $5.91 billion, is a leading ophthalmic medical technology and pharmaceutical company. It projects earnings growth of 1.3% for 2024, followed by 43.1% growth in 2025, and expects to maintain its strong performance in terms of revenues as well.

The company has a trailing four-quarter average negative earnings surprise of 4.74%.

Image Source: Zacks Investment Research

Key Catalysts

In 2023, Glaukos witnessed sales returning to growth after experiencing a downturn in 2022. This positive shift can be attributed to a more favorable macroeconomic climate and the introduction of a series of new products in recent quarters. The first-quarter results also reflected the strength. The company anticipates sustained robust demand in its international Glaucoma and Corneal Health product lines to support its top-line growth in the rest of 2024.

The commercial launch of the iStent infinite in 2023 has provided a significant lift to the U.S. glaucoma franchise, positioning it as a key growth catalyst in the forthcoming quarters. The company's optimistic revenue projections for 2024 indicate a positive trajectory.

Meanwhile, the new local coverage determinations, proposed in June 2023, are likely to remove certain ophthalmic goniotomy and canaloplasty procedures from coverage. This is also expected to have a positive impact on the iStent business in 2024.

Over recent quarters, GKOS has launched a suite of products, including iPrime, iAccess and iStent, which have been instrumental in boosting the company's revenues. In December, the company achieved a milestone by securing FDA approval for its latest product, iDose TR, to lower intraocular pressure in individuals with ocular hypertension or open-angle glaucoma.

These innovations are expected to continue to bolster Glaukos' growth trajectory into 2024. Earlier this month, the company received a permanent Healthcare Common Procedure Coding System J-code from the U.S. Centers for Medicare and Medicaid Services that should drive patient access in the United States. This is because it will likely accelerate the billing and physician reimbursement procedures.

In May, Glaukos announced first-quarter 2024 results. The company's net sales were $85.6 million, up 16% year over year. Revenues for 2024 are estimated to be in the range of $357-$365 million, implying a year-over-year improvement of 13.4-16%.

What's Hurting GKOS?

Although Glaukos has a promising pipeline, it has faced setbacks in terms of clinical development or regulatory activities. Any potential clinical or regulatory setback can have an adverse impact on the company's share price, thereby hurting investors' wealth.

The FDA denied approval to a pre-market approval application for the ab-externo device for glaucoma, MicroShunt. The company is currently evaluating alternate regulatory pathways for approval, and its commercial launch in the United States remains uncertain.

Moreover, Glaukos currently relies on a limited number of third-party suppliers, in some cases sole suppliers, to supply components for the iStent, the iStent inject models and other pipeline products. If one or more of these suppliers cease to provide the company with sufficient quantities of components or drugs in a timely manner or on acceptable terms, it would have to seek alternative sources of supply.

Glaukos' production of the iStent, iStent inject models and other products in development depends on a select group of third-party suppliers, occasionally exclusive ones. If any of these suppliers fail to deliver the necessary components or drugs in a timely manner or on acceptable terms, Glaukos would be compelled to find other suppliers to maintain its production line.

Estimate Trend

The bottom-line estimate for GKOS is pegged at a loss of $2.24 per share for 2024, which narrowed 2 cents in the past 30 days. The Zacks Consensus Estimate for 2024 revenues is pinned at $362.3 million, indicating growth of 15.1% from the top line recorded in 2023.

Stocks to Consider

Some better-ranked stocks in the broader medical space that have announced quarterly results are DaVita DVA, Ecolab ECL and Universal Health Services UHS.

DaVita, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 13.6%. DVA's earnings surpassed estimates in each of the trailing four quarters, the average surprise being 29.4%.

DaVita's shares have risen 32.1% compared with the industry's 5% growth so far this year.

Ecolab, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 13.3%. ECL's earnings surpassed estimates in each of the trailing four quarters, the average surprise being 1.7%.

Ecolab's shares have rallied 18.8% against the industry's 21.9% decline so far this year.

Universal Health Services has an Earnings ESP of +2.91% and a Zacks Rank #2 at present. UHS has an estimated earnings growth rate of 30.5% for 2024.

UHS' earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 8.12%. The company's shares have rallied 21.2% compared to the industry's 18.5% increase so far this year.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.