Paycom PAYC is one stock investors should consider adding to their portfolio to benefit from its upside potential.

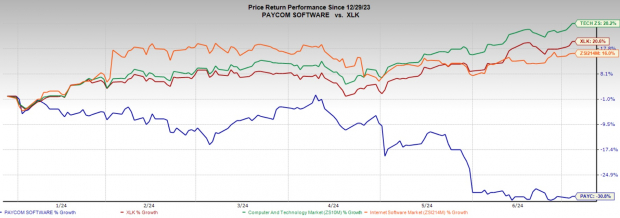

Making a remarkable rally in 2023, tech stocks have shown no signs of slowing this year. With a year-to-date (YTD) rise of 20.6%, the tech-laden Nasdaq Composite has outperformed The Dow Jones Industrial Average and the S&P 500 index's increase of 4.3% and 16.1%, respectively.

Technology stocks have more than 50% weightage in the Nasdaq Composite index. The Technology Select Sector SPDR Fund ETF, the most important component of the broad technology market index, has returned 21% YTD. The Zacks Computer and Technology sector has registered a YTD gain of 28.2%

The rally has been primarily driven by cooling inflationary pressure and stable gasoline prices, which have subsided the fears of a recession. A resurgence in global semiconductor sales and a potential benchmark interest rate cut this year are expected to continue driving the momentum for tech stocks for the remainder of 2024.

However, Paycom is among such stocks that have been left behind this year's tech rally. The stock has plunged 30.8% YTD while the Zacks Internet – Software industry has risen 39.1% during the same time frame. Therefore, considering the company's impressive growth profile and attractive valuation, we believe it is the right time to invest in the stock.

Image Source: Zacks Investment Research

Why Should You Invest in PAYC Stock?

Paycom currently trades significantly lower than its 52-week high, which reflects its potential to go upward. The stock's closing price of $143.11 on Jul 3, 2024, is 61.7% lower than the 52-week high of $374.04 attained on Jul 31, 2023.

Moreover, Paycom currently trades at an attractive valuation multiple. The stock trades at a one-year forward price-to-sales multiple of 4.22X compared with its five-year average of 14.41X. It also trades at a discount to the Zacks Computer – Technology Sector's one-year forward price-to-sales multiple of 6.90X.

Additionally, amid ongoing macroeconomic headwinds and geopolitical issues, it is prudent to pick solid growth companies as these are financially stable, accruing profits in established markets. These stocks, with their solid fundamentals, allow investors to hedge their funds from any economic downturn.

Apart from having solid fundamentals, Paycom sports a Zacks Rank #1 (Strong Buy) at present and has a Growth Score of B. Per Zacks' proprietary methodology, stocks with a combination of a Zacks Rank #1 or #2 (Buy) and a Growth Score of A or B offer solid investment opportunities.

Paycom has an impressive earnings surprise history. The company outpaced estimates in each of the trailing four quarters, delivering an average earnings surprise of 6.4%. Additionally, earnings estimates for PAYC's current fiscal year have increased, implying robust inherent growth potential. The Zacks Consensus Estimate for fiscal 2024 earnings has been revised 2 cents upward over the past 30 days to $7.71 per share.

Long-Term Growth Drivers

Paycom is capitalizing on the growing demand for bulky and complex Human Capital Management (HCM) software needed by large enterprises. The company is increasing its market share in this space by designing and deploying HCM solutions that minimize data integrity issues across applications.

PAYC flaunts a diverse portfolio of HCM solutions serving the various needs of enterprises at all levels. Its solutions help it manage talent acquisition, talent management, time and labor management, payroll and human resources management for both permanent and temporary workforce. This has increased Paycom's client base over the years, with an average annual client retention rate above 90% over the past seven years.

Paycom has grown its revenue meaningfully over the years by providing industry-leading service and technology solutions to its clients and their employees. Its solid business model, diversified products and services, and strategic acquisitions have boosted top-line growth. The Zacks Consensus Estimate suggests that its revenues in 2024 and 2025 will grow 10.2% and 11.1%, respectively, on a year-over-year basis.

Paycom is a cash-rich company with a strong balance sheet. As of Mar 31, 2024, the company had cash and cash equivalents of approximately $371 million, while it had no long-term debt. Since it has net cash available on its balance sheet, the existing cash can be used for pursuing strategic acquisitions, investing in growth initiatives and distributing to shareholders.

Considering a robust demand environment along with a diverse portfolio, continuously expanding customer base and strong cash balance, it is wise to invest in the PAYC stock right now.

Other Stocks to Consider

Some other top-ranked stocks from the broader technology sector are NVIDIA, Dropbox DBX and Datadog DDOG, each sporting a Zacks Rank #1 at present.

The Zacks Consensus Estimate for NVIDIA's 2025 earnings per share has been revised upward by 3 cents to $2.68 in the past 30 days. Shares of NVDA have skyrocketed 159% in the year-to-date period.

The Zacks Consensus Estimate for Dropbox's 2024 earnings per share has been revised upward by 11 cents to $2.12 in the past 60 days. Shares of DBX have plunged 23.3% in the year-to-date period.

The Zacks Consensus Estimate for Datadog's 2024 earnings per share has been revised upward by 12 cents to $1.54 in the past 60 days. Shares of DDOG have gained 8.3% in the year-to-date period.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.