lululemon athletica inc. LULU, a distinguished name in the athleisure and high-performance sportswear world, has often been lauded for its innovative products and strong brand loyalty. However, the stock recently experienced a notable dip in the past month, prompting investors to question whether now is the ideal time to buy.

lululemon's share price has experienced a downward trend, shedding a notable percentage in the past month. lululemon's share price has rolled down 7% in the past month, the broader industry has dropped 6.6%, and the Consumer Discretionary sector has declined 0.5%. The stock also traded shy of the S&P 500's gain of 3.6% in the same period.

Image Source: Zacks Investment Research

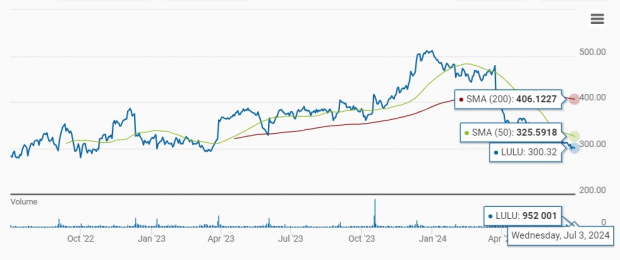

At the current price of $300.32, the stock trades closer to its 52-week low of $293.03 reached on May 28, 2024. The current stock price reflects a 42% discount from its 52-week high mark of $516.39.

Furthermore, LULU is trading below its 50 and 200-day moving averages, signaling potential bearish sentiment in maintaining recent performance levels.

lululemon's Stock Trades Above 50 and 200-Day Moving Average

Image Source: Zacks Investment Research

Understanding the Recent Decline

The recent stock decline follows lululemon's latest Jun 5 earnings report, highlighting slightly lower-than-expected revenue growth and cautious guidance for the upcoming quarters. While generally positive, the company's recent earnings report gave investors many reasons to mull over, including LULU losing its foothold in the core America market.

Investors noted that LULU's revenues improved by just 10% in the recent quarter, much below the 24% revenue growth recorded in the year-ago quarter. This marks a notable decline from the company's double-digit revenue growth trend that the investor community is used to witnessing.

lululemon attributed some of these challenges to inventory shortages in key product lines, such as popular bag designs and essential apparel sizes and colors, particularly in the United States. The company has been working on filling the inventory gaps that resulted in the shortage and expects to replenish inventory in its stores by the second half of fiscal 2024.

Taking a closer look, revenues for lululemon's Americas business grew 3% in the last reported quarter, displaying a significant slowdown from the growth of 17% in the year-ago quarter. The unfavorable trends in North America due to the inflationary environment have also weighed on the performance of LULU's competitors, including Columbia Sportswear COLM and Ralph Lauren Corp. RL.

Further, lululemon's business is not shielded from the tough macroeconomic environment, which entails serious pressures on discretionary items spending by consumers. The ongoing rise in inflation and higher interest rates have impacted the income levels of consumers, making them selective about their purchases.

Given the soft trends, the company guided a dim second quarter, with revenue growth of 9-10% year over year.

Should You Buy lululemon Amid Recent Challenges?

Although the above discussion might cause some concern, the company holds strong growth potential from an earnings standpoint. Despite the slowed revenues, lululemon has managed to maintain robust gross margin and operating margin levels at 57.7% and 19.6%, respectively, in the first quarter of fiscal 2024.

The company's improved margins mainly come from its ability to sustain its pricing power in all environments. How does the company achieve this?

lululemon is known for selling high-end apparel, placing it in the premier clothing category. Moreover, the company operates through owned stores and e-commerce portals rather than relying on third-party retailers to generate revenues.

This premium positioning and lack of dependency on third parties give lululemon control over its pricing strategies. Through effective pricing policies, the company efficiently converts revenues into profits.

lululemon's earnings potential is well reflected by its forward guidance, which predicts the second-quarter fiscal 2024 EPS to be $2.92-$2.97, up from $2.68 in the prior-year quarter. For fiscal 2024, LULU anticipates EPS of $14.27-$14.47, an increase from $12.77 reported in fiscal 2023.

The company is optimistic about its growing presence in the international market, particularly in China, which offers a lucrative opportunity. The company expects the momentum in the international business to continue in fiscal 2024. Over the long term, lululemon expects the international business to represent nearly 50% of its total revenue.

Also, lululemon continues to benefit from progress on its Power of Three X2 growth strategy. As part of the plan, LULU estimates net revenues of $12.5 billion by 2026, implying significant growth from the 2021 reported figure of $6.25 billion.

Upward Estimate Trajectory

The Zacks Consensus Estimate for LULU's fiscal 2024 and 2025 EPS rose 1.4% and 0.5%, respectively, in the last 30 days. The upward revision in earnings estimates indicates analysts' increasing confidence in the stock.

For fiscal 2024, the Zacks Consensus Estimate for LULU's sales and EPS implies 11.4% and 11.9% year-over-year growth, respectively. The consensus mark for fiscal 2025 sales and earnings indicates 9.9% and 10.1% year-over-year growth, respectively.

Image Source: Zacks Investment Research

Valuation

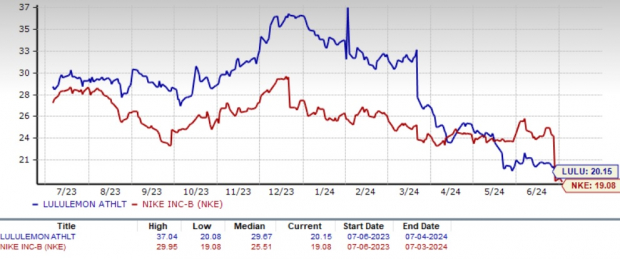

Despite the downside, lululemon is currently trading at a forward 12-month P/E multiple of 20.15X, significantly exceeding the industry average of 12.49X. The stock trades at a premium to its rival NIKE's NKE current forward 12-month P/E of 19.08X, which witnessed a significant drop in its market value after its recent earnings release.

The premium valuation indicates that investors have high expectations for lululemon's future performance and growth potential. However, lululemon's valuation appears a bit pricey. Investors may be skeptical about buying the stock at these premium levels and may wait for a better entry point.

Image Source: Zacks Investment Research

Conclusion

lululemon's recent stock decline may appear concerning at first glance, but it could also be seen as an opportunity for savvy investors. Despite the slowdown in revenues and the challenging path ahead, LULU shows resilience and growth potential in its earnings outlook and strategic positioning.

Despite the decline in the stock price, the company's premium valuation may give some investors pause, suggesting a potentially higher risk profile at current price levels. Therefore, investors should carefully consider their risk tolerance and wait for a more favorable entry point if concerned about current valuations. For those already invested, you should consider holding back the stock for solid long-term prospects.

lululemon currently carries a Zacks Rank #3 (Hold).

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.