The Financial Transaction Services industry is poised to benefit from the increasing adoption of digital solutions. A robust digital offering allows industry players to leverage this trend effectively. Favorable consumer spending patterns are expected to drive transaction volumes higher. To maintain a competitive edge, companies must invest in technology, enhance operational efficiency and diversify revenue streams. A merger and acquisition (M&A) strategy enhances capabilities. Companies like Fiserv, Inc. FI, Fidelity National Information Services, Inc. FIS, Global Payments Inc. GPN, WEX Inc. WEX and The Western Union Company WU are placed well to gain from the industry's encouraging growth prospects.

About the Industry

The Zacks Financial Transaction Services industry is part of the Financial Technology or the FinTech space, including companies with diverse natures of businesses. The industry comprises card and payment processing and other solutions providers, ATM services and money remittance service providers and providers of investment solutions to financial advisors. The players in this segment operate their unique and proprietary global payments network that links issuers and acquirers around the globe to facilitate the switching of transactions, permitting account holders to use their products at millions of acceptance locations. Monetary transactions are effectuated through these networks, offering a convenient, quick and secure payment method in several currencies across the globe. The industry is benefiting from the ongoing digitization movement triggered by the pandemic.

4 Trends Influencing the Financial Transaction Services Industry's Future

Widespread Adoption of Contactless Payment Methods: There has been a growing preference for contactless payments among worldwide consumers and the trend shows no mood of slowing down. With cash and checks declining in use, industry players have introduced various flexible digital payment options such as cryptocurrency, biometrics, QR codes and buy now, pay later solutions. They have enjoyed an expanding customer base and diversified revenue streams, owing to the ease and benefits that these solutions provide. Therefore, these companies are driven to invest heavily in technology to maintain a competitive edge and sustain market leadership. However, increasing digitization also attracts sophisticated cybercrimes, leading to significant losses and data breaches for consumers and merchants alike. Thus, industry players not only develop efficient payment solutions but also invest in effective fraud prevention measures.

Strong Consumer Spending: The increase in consumer spending indicates a higher utilization of the product and service offerings of industry players. This surge in consumer spending translates to higher transaction volumes and, consequently, increased revenues for these companies. Deloitte, in an article published by Deloitte Global Economics Research Center, projects consumer spending to remain robust through the first half of 2024, driven by ongoing improvements in the labor market and consistent spending levels from both business and government sectors. A tight labor market with strong wage gains and a thriving e-commerce environment is expected to keep consumer spending at favorable levels in the days ahead. However, inflationary pressures could strain consumers' purchasing power.

Inorganic Growth Efforts: To build a comprehensive digital solutions suite, the industry players frequently pursue mergers and acquisitions alongside their technology investments. These strategies are vital for enhancing capabilities, gaining diversification benefits, expanding the customer base, and strengthening global presence. The Federal Reserve decided to maintain its interest rate at its latest policy meeting, with no rate changes since the beginning of 2024 after 11 hikes in 2022 and 2023. Steady interest rates may encourage more financial transaction services companies to opt for loans to enter M&A deals and avoid the complete exhaustion of cash reserves.

Strong Cross-Border Volumes: Financial transaction services stocks with exposure to the cross-border business are well-positioned to capitalize on increased international trade, increased travel, whether for recreational or office purposes, and the ongoing demand for efficient remittance services. Companies offering advanced cross-border payment solutions stand out as attractive investments, as they facilitate seamless international transactions and manage currency exchange. These solutions play a crucial role in enabling businesses to easily accept payments from customers in different countries and make timely supplier payments, ensuring smooth operations. The growing international workforce continues to drive the demand for effective cross-border remittance services.

Zacks Industry Rank Instills Optimism

The group's Zacks Industry Rank, which is basically the average of the Zacks Rank of all member stocks, indicates bright near-term prospects. The Zacks Financial Transaction Services industry is housed within the broader Zacks Business Services sector. It currently carries a Zacks Industry Rank #67, which places it in the top 27% of more than 250 Zacks industries.

Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1. The industry's positioning in the bottom 50% of the Zacks-ranked industries is a result of a negative earnings outlook for the constituent companies in aggregate.

Before we present a few stocks that you may want to buy or retain in your portfolio, let's take a look at the industry's recent stock-market performance and valuation picture.

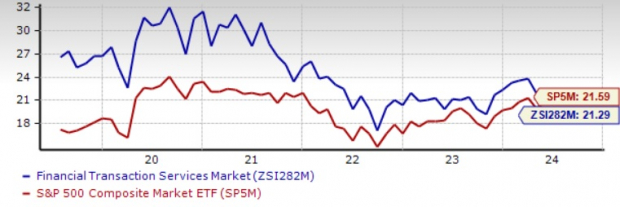

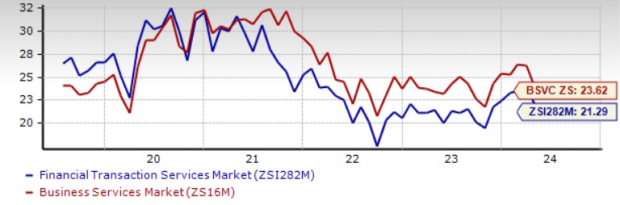

Industry Underperforms Sector, S&P 500

The Zacks Financial Transaction Services industry underperformed its sector and the Zacks S&P 500 composite in the past year.

In the said time frame, the industry has gained 10.6% compared with the Business Services sector's growth of 15.1%. The S&P 500 has rallied 26.7% in the same time frame.

One-Year Price Performance

Image Source: Zacks Investment Research

Industry's Current Valuation

On the basis of the forward 12-month Price/Earnings ratio, commonly used for valuing financial transaction services stocks, the industry is currently trading at 21.29X compared with the S&P 500's 21.59X and the sector's 23.62X.

In the past five years, the industry traded as high as 32.49X, as low as 17.61X and at the median of 23.97X.

Forward 12-Month Price/Earnings (P/E) Ratio

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

5 Stocks to Keep a Close Eye on

We are presenting five stocks from the Financial Transaction Services industry that currently carry a Zacks Rank #2 (Buy) or Zacks Rank #3 (Hold). Considering the current industry scenario, it might be prudent for investors to buy or retain these stocks in their portfolio, as these are well-placed to generate growth in the long haul.

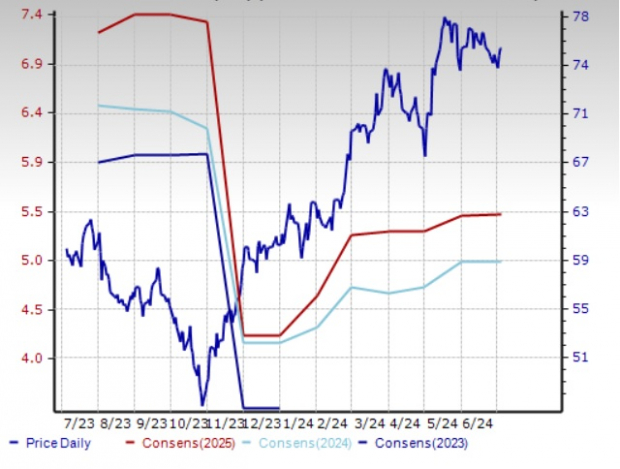

Fiserv: Wisconsin-based, Fiserv provides a varied array of products and services, including payment processing, core banking systems, digital banking solutions, and more. Its business model combines the benefits of recurring revenues and high incremental margins from a scaled processing business, which enhances growth and profitability. The Zacks Rank #2 company can achieve outperformance through new client acquisition, retaining and expanding relationships with existing clients and delivering value-added solutions.

The Zacks Consensus Estimate for Fiserv's 2024 earnings is pegged at $8.69 per share, indicating a 15.6% rise from the year-ago reported figure. FI's earnings beat estimates in three of the last four quarters and matched the mark once, the average being 2.28%.

Price and Consensus: FI

Image Source: Zacks Investment Research

Global Payments: Based in Atlanta, GA, Global Payments is well-poised for growth on the back of solid contributions from the Merchant Solutions and Issuer Solutions segments. The Merchant Solutions unit is poised to benefit from increased transaction volumes and an expanding base of U.S. merchant partners. At the same time, the Issuer Solutions segment is anticipated to benefit from growth in core issuers. This Zacks Rank #2 company has resorted to acquisitions and partnerships to bolster its capabilities and geographical presence.

The Zacks Consensus Estimate for Global Payments' 2024 earnings is pegged at $11.64 per share, indicating an 11.7% rise from the year-ago figure. GPN's earnings beat estimates in each of the last four quarters, the average being 1.14%.

Price and Consensus: GPN

Image Source: Zacks Investment Research

Western Union: The Colorado-based Western Union, traditionally a brick-and-mortar money transfer company, has successfully developed a strong digital arm. Through significant investments and strategic digital partnerships, the Zacks Rank #2 company has seen impressive digital revenue growth. To further digitize the money movement process for consumers and businesses, Western Union partnered with several prominent global and regional financial service providers.

The Zacks Consensus Estimate for Western Union's 2024 earnings is pegged at $1.76 per share, indicating an improvement of 1.2% from the year-ago reported figure. WU's earnings beat estimates in each of the last four quarters, the average being 15.66%.

Price and Consensus: WU

Image Source: Zacks Investment Research

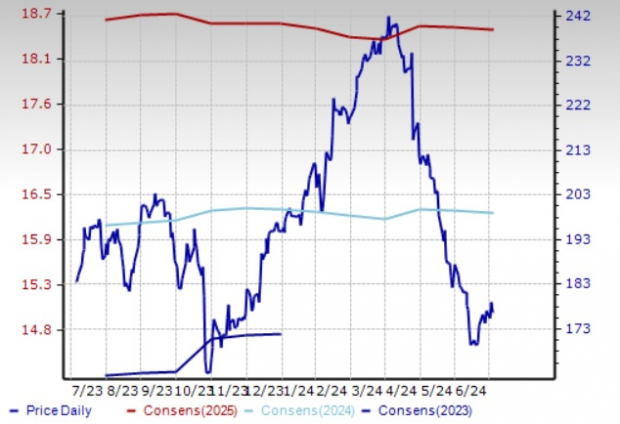

Fidelity National: Headquartered in Jacksonville, FL, Fidelity National's revenue growth is being driven by the robust performances of its Banking Solutions and Capital Market Solutions segments. The Banking unit is benefiting from new client acquisitions, while the Capital Market business is experiencing strong sales growth, contributing to increased recurring revenues. This Zacks Rank #3 company employs organic growth strategies and acquisitions to secure multi-year recurring contracts.

The Zacks Consensus Estimate for Fidelity National's 2024 earnings is pegged at $4.97 per share, calling for an improvement of 47.5% from the year-ago reported figure. The consensus mark for 2024 earnings has moved 7.1% north in the past 60 days.

Price and Consensus: FIS

Image Source: Zacks Investment Research

WEX: Headquartered in Portland, ME, WEX is being aided by an extensive fuel network and service providers, improved transaction volumes, product excellence, marketing prowess, sales force productivity and other strategic revenue generation efforts. This Zacks Rank #3 company's revenue stability is underpinned by its high-quality products and services and deep client understanding, along with long-term strategic relationships, multi-year contracts and high contract renewal rates. Acquisitions are a key growth catalyst.

The Zacks Consensus Estimate for WEX's 2024 earnings is pegged at $16.23 per share, which indicates a rise of 9.6% from the 2023 figure. WEX's earnings beat estimates in three of the last four quarters and missed the mark once, the average being 3.31%.

Price and Consensus: WEX

Image Source: Zacks Investment Research

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.