RLI Corp.'s RLI strong product portfolio, rate increases, improved retention, higher premium receipts and sufficient liquidity make it worth adding to one's portfolio.

Optimistic Growth Projections

The Zacks Consensus Estimate for RLI's 2024 earnings per share indicates an increase of 18.4% from the year-ago reported number. The consensus estimate for revenues is pegged at $1.64 billion, implying a year-over-year improvement of 15.6%.

The consensus estimate for 2025 earnings per share and revenues indicates an increase of 3.8% and 9.2%, respectively, from the corresponding 2024 estimates.

Earnings have grown 18.7% in the past five years, better than the industry average of 10.5%

Earnings Surprise History

RLI has a solid track record of beating earnings estimates in three of the last four quarters while missing in one, the average being 132.39%.

Estimate Revision

The Zacks Consensus Estimate for 2024 and 2025 earnings has moved 1.9% and 2.7% north, respectively, in the past 60 days. This should instill investors' confidence in the stock.

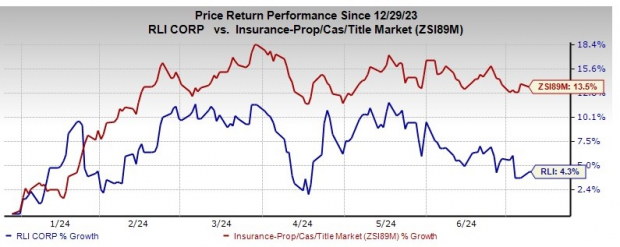

Zacks Rank & Price Performance

RLI currently carries a Zacks Rank #2 (Buy). Year to date, the stock has gained 4.3% compared with the industry's growth of 13.5%.

Image Source: Zacks Investment Research

Business Tailwinds

Product diversification across the Casualty, Property and Surety segments of the company has fueled the insurer's growth and financial success. The Casualty segment continues to gain from an expanded distribution base in personal umbrella and rate increases.

The commercial property business has been gaining from higher wind and earthquake exposure rates. Rate increases, improved retention and new opportunities in the inland marine space should benefit marine products.

The Surety segment continues to benefit from its compelling product portfolio, growth within existing accounts and writing of bonds with new customers. Building materials inflation and new accounts will aid commercial and contract surety businesses in the future. RLI boasts solid operating results and its financial position remained strong. Operating cash flows are likely to gain from higher premium receipts.

The insurer has a sound capital structure, helping it meet the interests of its policyholders, enhance operations in the insurance sector and aid growth in its book value for the long term. The insurer's trailing 12-month return on equity of 17.2% outperforms the industry average of 7.8%. Such a robust capital position provides significant financial flexibility to the operating subsidiaries.

RLI has been paying dividends for 187 consecutive quarters and increased regular dividends in each of the last 48 years at an eight-year (2016-2023) CAGR of 3.9%. In addition, the insurer has been paying special dividends since 2011. Over the past five years, the insurer has returned $816 million to shareholders. RLI has $87.5 million of remaining capacity from the repurchase program.

Other Stocks to Consider

Some other top-ranked stocks from the property and casualty insurance industry are Palomar Holdings, Inc. PLMR, ProAssurance Corporation PRA and NMI Holdings Inc NMIH. While Palomar Holdings and ProAssurance sport a Zacks Rank #1 (Strong Buy) each, NMI Holdings currently carries a Zacks Rank #2.

Palomar Holdings earnings surpassed estimates in each of the last four quarters, the average surprise being 15.10%. Year to date, shares of PLMR have jumped 49.4%. The Zacks Consensus Estimate for PLMR's 2024 and 2025 revenues implies year-over-year growth of 26% and 18.1%, respectively.

The Zacks Consensus Estimate for ProAssurance's 2024 and 2025 earnings has moved 46.1% and 24.5% north, respectively, in the past 60 days. Year to date, shares of PRA have jumped 4.3%. The Zacks Consensus Estimate for PRA's 2024 and 2025 revenues implies year-over-year growth of 371.43% and 72.63%, respectively.

NMI Holdings' earnings surpassed estimates in each of the last four quarters, the average surprise being 8.60%. Year to date, shares of NMIH have jumped 14.1%. The Zacks Consensus Estimate for NMIH's 2024 and 2025 revenues implies year-over-year growth of 10.6% and 7.6%, respectively.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.