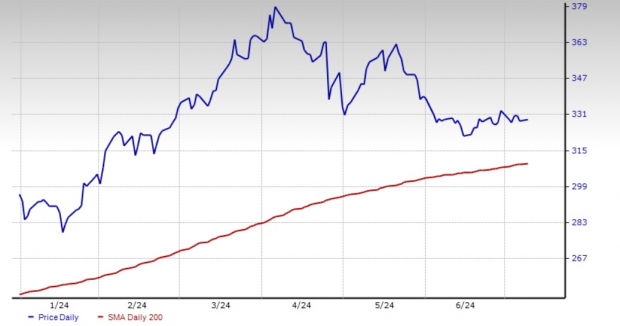

Caterpillar CAT has consistently traded above its 200-day simple moving average so far this year, indicating robust upward momentum. This reflects the company's solid financial performance, steady return to shareholders, and confidence in CAT's financial health and prospects.

CAT Trades Above 200-Day SMA

Image Source: Zacks Investment Research

Caterpillar shares have gained 32.2% in the past year, outperforming the industry's 28.4%. It has also outpaced the broader Zacks Industrial Products sector's 9.2% growth and the S&P 500's climb of 27.8%.

CAT's One Year Price Performance Against Industry & Broader Market

Image Source: Zacks Investment Research

The stock's performance has been upbeat compared with its peers. Shares of Komatsu KMTUY have risen 16%, whereas Astec ASTE and Terex TEX have witnessed declines of 33.3% and 9.8%, respectively, in the same time span.

Is this the right time to buy CAT shares to gain from the potential upside? Let us delve deeper into the stock's fundamentals to find out.

Earnings Growth Consistent

Caterpillar has reported year-over-year improvements in earnings per share for thirteen straight quarters. This demonstrates resilience amid the significant challenges faced by the company and the broader industry during this period, including the pandemic, supply-chain disruptions and prolonged contraction in the manufacturing sector since November 2022.

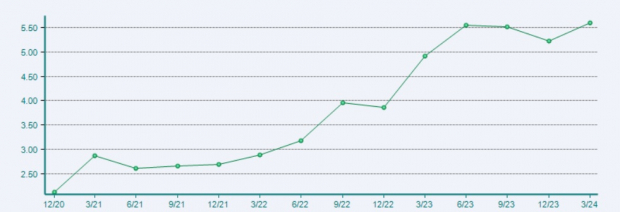

The chart below shows an upward trend in CAT's EPS over the past three years. This feat was achieved by its cost-saving strategies, pricing actions and strong demand in its end markets. Notably, Caterpillar has delivered record EPS in 2023 and the first quarter of 2024.

Caterpillar's EPS Trend in Past 3 Years

Image Source: Zacks Investment Research

Backlog Robust & End-Market Demand Upbeat

Caterpillar reported a solid backlog of $27.9 billion at the end of the first quarter of 2024. Backlog as a percentage of revenues is higher than historic levels, which poises the company well for the forthcoming few quarters.

The increase in projects enabled by the U.S. Infrastructure Investment and Jobs Act creates massive opportunities for Caterpillar's wide range of construction equipment.

The worldwide efforts in the transition to clean energy will require a huge amount of commodities, which, in turn, will boost the demand for Caterpillar's mining equipment. Miners are increasingly relying on autonomy to increase productivity and efficiency, reduce costs, and improve safety. Caterpillar has been enhancing its autonomous fleet to capitalize on these trends.

In Energy & Transportation, strong order rates in most applications are expected to support revenues. In the Oil & Gas sector, the increased focus on sustainability will drive the demand for CAT equipment. As technology companies establish data centers globally to support their generative AI applications, Caterpillar is witnessing robust order levels for reciprocating engines for data centers. The company is planning to double its output with a multi-year capital investment.

High-Margin Service Revenues Act as a Key Catalyst

In the e-commerce space, Caterpillar has been enhancing its digital product offerings. In 2023, the company added more than 100,000 customers to its online channel. In 2022, it had set a three-year goal to grow dealer parts sales through e-commerce by 50% from a baseline of $10 million per day and has already achieved the goal.

CAT has been seeing growth in aftermarket parts and service-related revenues, which generate high margins. Caterpillar is on track to double its services revenues from $14 billion in 2016 to $28 billion in 2026.

Solid Liquidity & Attractive Dividend Yield & Payout

Caterpillar's cash and liquidity position remains strong, which enables it to invest in business while returning cash to shareholders. Machinery and Energy & Transportation's (ME&T) free cash was a record $10 billion in 2023 and was $1.3 billion in the first quarter of 2024. It expects the free cash flow in 2024 to be in the top half of $5-$10 billion. The company returned a record $5.1 billion in cash as share repurchases and dividends in the first quarter of 2024. CAT has a target to return all of its ME&T free cash flow to shareholders over time.

In June 2024, Caterpillar announced an 8% hike in the quarterly dividend to $1.41 per share. The company has a five-year dividend growth rate of 6.1%. CAT's 1.57% dividend yield is higher than the sector's yield of 1.50% and the S&P 500's 1.26%.

CAT has a payout ratio of 23.7%, higher than the industry's 22.5%. The company has a solid track of paying higher dividends to shareholders for 30 straight years and is a member of the S&P 500 Dividend Aristocrat Index.

CAT has also added $20 billion to its existing share repurchase authorization, which was launched in 2022 with no expiration date. This entitles Caterpillar to repurchase up to $21.8 billion of its common stock.

Generating Returns Higher Than Broader Market

Return on equity — a profitability measure of how prudently the company is utilizing its shareholders' funds — is 57%, higher than the sector's average of 22.8% and the S&P 500's 28.2%.

CAT's Return on Assets is at 12.7%, ahead of the sector's 7.5% and the S&P 500's 7.1%, indicating that the company has been utilizing its assets efficiently to generate returns.

Upbeat Earnings Estimates

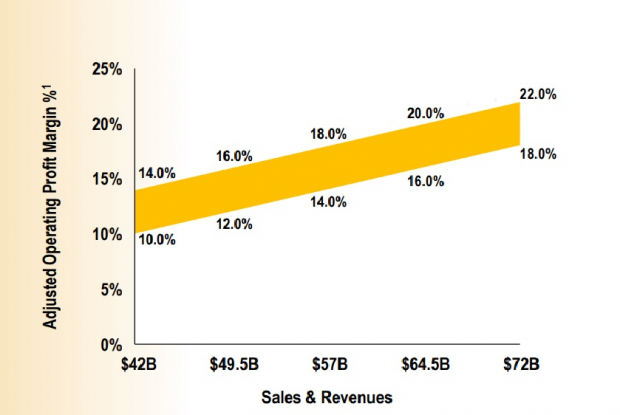

Caterpillar expects revenues in 2024 to be in line with the record 2023 revenues of $67 billion. The company maintains its guidance of revenues at $42-$72 billion. According to the revenue levels, margins are expected between 10% and 22%. The adjusted operating margin in 2024 is expected to be in the top half of the target range corresponding to the expected level of revenues.

CAT's Guidance Range

Image Source: Caterpillar

The Zacks Consensus Estimate for 2024 earnings indicates year-over-year growth of 2.45% and 5.90% for 2025. CAT has a long-term EPS growth rate of 8.9%.

Valuation

CAT is currently trading at a forward 12-month P/E of 14.68, at a premium compared with the industry's 14.22X. The stock is also not cheap when compared with Komatsu, Terex and Manitowoc, all of which are currently trading below the industry.

Image Source: Zacks Investment Research

To Sum Up

Caterpillar's solid long-term demand prospects, backed by infrastructure spending and energy-transition trends, as well as its focus on growing service revenues, should help it maintain an upbeat performance. The company is also returning value to shareholders through share buybacks and consistent dividend payments. Existing stakeholders should maintain their position in this Zacks Rank #3 (Hold) stock, while new investors should wait for a better entry point, given its higher valuation.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.