PG&E Corporation PCG is poised to benefit from positive developments like steady infrastructural investments, the addition of clean energy projects and initiatives to build California's electric vehicle charging infrastructure.

Let's focus on the factors that make this Zacks Rank #2 (Buy) stock a good investment option at the moment.

Rising Estimates

The Zacks Consensus Estimate for PCG's 2024 and 2025 earnings per share implies growth of 9.8% and 8.4%, respectively, from the year-ago levels.

The Zacks Consensus Estimate for PCG's 2024 and 2025 sales indicates a rise of 4.9% and 4.1%, respectively, from the prior-year figures.

Better-Than-Industry Returns

PCG's return on invested capital has outperformed the industry's average in the trailing 12 months. ROIC of PCG was 5.05% compared with the industry average of 3.41%. The company has been investing effectively in profitable projects, which is evident from its ROIC.

PCG's trailing 12-month return on equity is 11.32%, ahead of the industry's average of 9.72%. Return on equity, a profitability measure, reflects how effectively a company utilizes its shareholders' funds to generate income.

Capital Expenditure

PG&E continues to make considerable investments in gas-related projects and electric system safety and reliability to further strengthen its grid and thereby boost customer satisfaction. To this end, the company invested $9.8 billion in 2023. Looking ahead, management aims to make investments worth $10.4 billion in 2024. For 2024-2028, the company expects to invest $62 billion.

Solvency Ratio

The times interest earned ratio at the end of first-quarter 2024 is 1.42, which indicates financial strength of the company and its ability to meet short-term obligations or dues within the next 12 months.

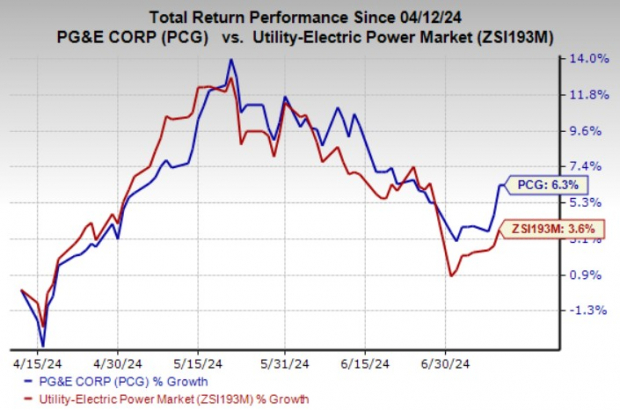

Price Movement

In the past three months, PCG's shares have risen 6.3% compared with the industry's growth of 3.6%.

Image Source: Zacks Investment Research

Other Key Picks

Some other top-ranked stocks from the same industry are CenterPoint Energy CNP, FirstEnergy FE and Consolidated Edison ED, each carrying a Zacks Rank #2 at present.

The Zacks Consensus Estimate for CenterPoint Energy, FirstEnergy and Consolidated Edison's 2024 earnings reflects year-over-year growth of 8%, 5.1% and 3.1%, respectively.

The long-term (three-to-five years) earnings growth rate of CenterPoint Energy, FirstEnergy, and Consolidated Edison is 7%, 5.9% and 7.4%, respectively.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.