Hawaiian Holdings HA is riding on its continued healthy demand scenario. The company's efforts to expand are commendable. However, a surge in operating expenses and weak liquidity does not bode well for the company.

Factors Favoring HA

The uptick in air travel demand bodes well for Hawaiian Holdings. In the first quarter of 2024, scheduled airline traffic (measured by revenue passenger miles) increased 5.9% year over year. Scheduled capacity (measured in available seat miles or ASM) rose 2.7% year over year. Passenger load factor (percentage of seats filled by passengers) improved by 2.4 pts to 80.6% year over year.

For the second quarter of 2024, the company expects a 3.5%-6.5% year-over-year increase in ASM. Meanwhile, for the full year, the company expects the metrics to improve 4.5%-7.5% year over year.

HA's expansion efforts are praiseworthy. On Apr 15, 2024, Hawaiian Holdings began Boeing 787-9 Dreamliner revenue service, a move expected to double premium seating on key routes while maintaining competitive operating costs. The airline also announced new flights from Salt Lake City to Honolulu and from Sacramento to Lihu'e and Kona.

The impending merger with Alaska Air Group ALK is another tailwind for HA, under which Alaska will acquire Hawaiian for $18.00 per share in cash with a transaction value of approximately $1.9 billion. This merger is expected to provide a substantial boost for Hawaiian, enhancing its ability to execute its business plan, strengthen its liquidity and manage its debts effectively.

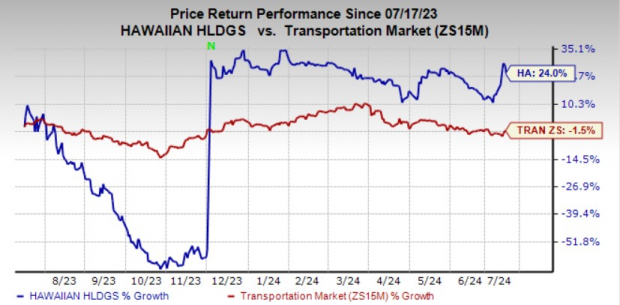

Shares of Hawaiian Holdings have rallied 24% over the past year compared to a 1.5% decline of the industry.

Image Source: Zacks Investment Research

Key Risks

Rising fuel costs are hurting Hawaiian Holdings' bottom line. This trend is primarily due to the ongoing production cuts adopted by Saudi Arabia and Russia. The fuel price per gallon is anticipated to be $2.85 for the second quarter of 2024 and $2.83 for the full year of 2024.

The elevated labor expenses are also severely impacting the company's bottom line by pushing up operating costs.The company expects costs per available seat mile (excluding fuel & non-recurring items) in the second quarter of 2024 to increase 5-8% from the second-quarter 2023 actuals.

Hawaiian Holdings ended the first quarter of 2024 with a current ratio (a measure of liquidity) of 0.89. A current ratio of less than 1 implies that the company does not have enough cash to meet its debt burden, raising liquidity concerns.

Zacks Rank

HA currently carries a Zacks Rank #3 (Hold).

Stocks to Consider

Some better-ranked stocks for investors' consideration in the Zacks Transportation sector include SkyWest SKYW and Air Lease AL.

SKYW currently sports a Zacks Rank #1 (Strong Buy) and has an expected earnings growth rate of 787% for the current year.

The company has an impressive earnings surprise history. Its earnings outpaced the Zacks Consensus Estimate in each of the trailing four quarters, delivering an average surprise of 128%. Shares of SkyWest have jumped 101% in the past year.

AL sports a Zacks Rank #1. Air Lease has an expected earnings growth rate of 31.1% for the current year.

The company has an encouraging track record with respect to the earnings surprise, having surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missing once. The average beat is 15.6%. Shares of AL have climbed 11% in the past year.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.