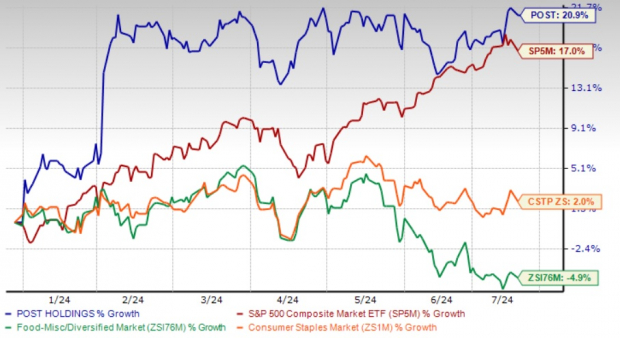

Post Holdings, Inc. POST has shown impressive performance lately, with shares gaining 20.9% year to date, marking a significant contrast to the industry's decline of 4.9%. The leading consumer-packaged goods company has adeptly managed pricing strategies to mitigate the impact of inflationary pressures, particularly sugar and labor costs.

Strategic acquisitions are further expanding Post Holdings' market reach and have been pivotal in enhancing the company's market position and diversifying its revenue streams. Notable acquisitions, such as Perfection Pet, have strengthened the company's portfolio and contributed to its growth trajectory.

Thanks to its robust performance across segments, this Zacks Rank #3 (Hold) company has managed to surpass both the Zacks Consumer Staples sector and the S&P 500's respective gains of 2% and 17%, respectively, in the year-to-date period.

Image Source: Zacks Investment Research

Decoding the Stock's Rally

Post Holdings is experiencing significant momentum driven by strategic initiatives and robust performance in its Post Consumer Brands segment. During the second quarter of fiscal 2024, this segment showcased a remarkable 77.9% rise in revenues, bolstered significantly by $460.7 million in sales from acquisitions. Furthermore, the company's pet food and grocery business delivered impressive results within this segment, driven by the successful expansion of its value offerings.

Buoyed by exceptional manufacturing performance, and strategic carryover pricing, Post Holdings' pet food and grocery business not only met but exceeded market demands, contributing significantly to the company's overall performance. These factors underscore the effectiveness of Post Holdings' growth strategies and its ability to capitalize on market opportunities.

The acquisition of Perfection Pet in December 2023 has significantly benefited Post Holdings, expanding its customer base and strengthening its position in the market. Additionally, other notable acquisitions such as Lacka Foods Limited, PL RTE Cereal Business, Almark Foods, Conagra's Peter Pan peanut butter brand, and select pet food brands from The J.M. Smucker Co have further supported Post Holdings' growth strategy.

These acquisitions have not only expanded the company's brand lineup but also diversified its product offerings, enhancing its competitive edge in the consumer-packaged goods sector.

Unlocking Shareholder Value

Post Holdings' robust cash flows enable it to engage in shareholder-friendly actions. In the second quarter of fiscal 2024, it repurchased 0.1 million shares for $103.88 million. This demonstrates the company's commitment to returning value to shareholders through buybacks.

Overall, these actions underscore Post Holdings' strategic capital allocation approach focusing on enhancing shareholder returns while maintaining financial flexibility for future growth initiatives.

Hiccups on the Path

Despite the positive performance indicators, Post Holdings faces challenges in a tough macroeconomic environment. Escalated SG&A expenses, inflationary pressures, intense competition, declines in restaurant foot traffic, and inventory reductions remain significant concerns for the company. These factors underline the importance of prudent management and strategic decision-making to navigate challenges effectively and maintain sustainable growth amid external pressures.

Additionally, Post Holdings stock is trading at a significant premium compared to the Zacks Food - Miscellaneous industry. Its forward 12-month P/E of 17.48X is higher than the industry's 15.42X.

While Post Holding's strategic initiatives keep it well positioned for further growth, investors might want to wait for a better entry point, given the near-term hurdles and stretched valuation. Post Holdings currently carries a Zacks Rank #3 (Hold).

3 Picks You Can't Miss

Here, we have highlighted three better-ranked stocks, namely, Colgate-Palmolive CL, Church & Dwight Co., Inc. CHD and Ollie's Bargain Outlet OLLI.

Colgate-Palmolive, which manufactures and sells consumer products, currently carries a Zacks Rank #2 (Buy). CL delivered an earnings surprise of 4.4% in the trailing four quarters, on average.

The Zacks Consensus Estimate for Colgate-Palmolive's current fiscal-year sales and earnings suggests growth of 3.8% and nearly 9.3%, respectively, from the year-ago reported numbers.

Church & Dwight Co. develops, manufactures and markets a broad range of household, personal care and specialty products. The company currently carries a Zacks Rank #2. CHD has a trailing four-quarter earnings surprise of 9.6%, on average.

The Zacks Consensus Estimate for Church & Dwight's current fiscal-year sales and earnings suggests growth of 4.6% and 9.1%, respectively, from the year-ago reported numbers.

Ollie's Bargain, the extreme-value retailer of brand-name merchandise, currently carries a Zacks Rank #2. OLLI has a trailing four-quarter earnings surprise of 10.4%, on average.

The Zacks Consensus Estimate for Ollie's Bargain's current financial-year sales and earnings indicates a rise of around 7.9% and 12.0%, respectively, from the year-earlier levels.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.