Royal Caribbean Cruises Ltd. RCL is scheduled to release second-quarter 2024 results on Jul 25, 2024. The company is likely to have benefited from positive customer sentiments bolstered by resilient labor markets, stabilizing inflation and a narrowed gap to land-based vacations.

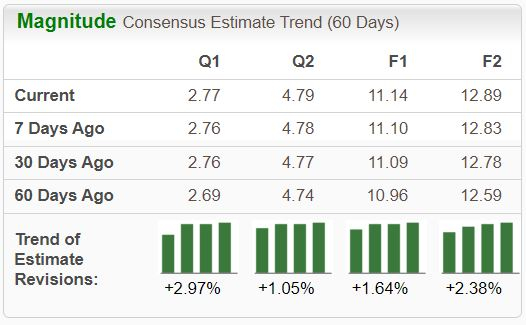

The Zacks Consensus Estimate for RCL's second-quarter earnings per share is pegged at $2.77, suggesting 52.2% growth from $1.82 reported in the prior-year quarter. The consensus mark has increased by 3% in the past 60 days. For quarterly revenues, the consensus mark is pegged at $4 billion, suggesting a 13.4% rise from the year-ago quarter's reported figure.

Image Source: Zacks Investment Research

Earnings Surprise History

The company has a modest earnings surprise history in the trailing four quarters, exceeding earnings expectations on each occasion. It delivered an earnings surprise of 18.3%, on average. In the last reported quarter, the company delivered an earnings surprise of 35.1%.

Image Source: Zacks Investment Research

Q2 Earnings Whispers

Our proven model does not conclusively predict an earnings beat for Royal Caribbean this time around. A stock needs to have a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) to beat on earnings. But that's not the case here.

Royal Caribbean has a Zacks Rank #1 and an Earnings ESP of -0.43%.

Factors to Influence RCL's Q2 Results

Royal Caribbean's second-quarter performance is likely to have benefitted from robust demand, courtesy of its digital initiatives, ship upgrades and enhanced product offerings. This and the strong booking and pricing environment across key itineraries, coupled with continued strength in onboard, are likely to have driven the company's top-line in the second quarter.

Our model estimates second-quarter passenger ticket revenues to rise 6.1% year over year to $2.59 billion. We expect onboard and other revenues to increase 23.3% year over year to $1.33 billion.

Royal Caribbean is enhancing its commerce platform with new technology and artificial intelligence to improve the experience across various distribution channels, build stronger customer loyalty and reduce guest acquisition costs. It is investing in a modern digital travel platform to streamline travel planning, making it easier for guests to book vacations and expand wallet share. The initiatives are likely to have strengthened load factors and improved yields in the second quarter.

The company anticipates net yields to rise 10-10.5% (on a reported basis) and 10.2-10.7% (constant-currency basis) from 2023 levels. Our model predicts second-quarter net yields at $262 million (on a reported basis) and $263 million (constant-currency basis).

Elevated costs concerning fuel and food are likely to have hurt margins in the second quarter. Our model predicts total cruise operating costs to rise 5% year over year to $2.05 billion.

The company expects second-quarter net cruise costs (excluding fuel per APCD) to increase 5.4% (on a reported basis) and 5.5% (constant currency), respectively, on a year-over-year basis. Per our model, second-quarter net cruise costs (excluding fuel per APCD) are estimated at $126.2 million (on a reported basis) and $126.7 million (constant-currency basis).

Price Performance & Valuation

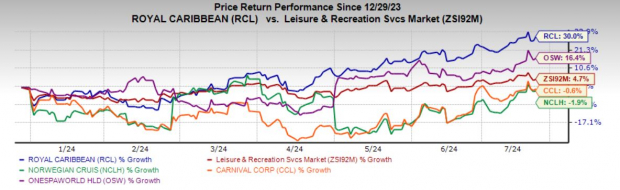

Shares of Royal Caribbean have rallied 30% in the year-to-date period compared with the Zacks Leisure and Recreation Services industry's rise of 4.7%.

Despite disruptions at Eastern Mediterranean sailings, the stock outperformed its peers, including Carnival Corporation & plc CCL, Norwegian Cruise Line Holdings Ltd. NCLH and OneSpaWorld Holdings Limited OSW.

Image Source: Zacks Investment Research

From a valuation perspective, RCL is trading relatively cheap. The company has a forward 12-month price-to-earnings of 13.89X, below the industry average of 16.63X. The company has a Value Score of A.

Image Source: Zacks Investment Research

Investment Considerations

RCL's robust demand, strategic digital initiatives, and enhanced offerings position it favorably for strong second-quarter financial performance. The anticipated revenue and earnings growth reinforces the positive outlook for RCL stock.

While RCL is attractively valued and has strong fundamentals, it may be a good time to buy the stock before the earnings release. The company's robust booking volumes and enhanced onboard spending underscore its ability to capitalize on increasing travel demand.

Strong operational performance, strategic market expansions and innovative product offerings have been a major tailwind for the stock. With a favorable valuation compared with industry peers and upwardly revised earnings projections, RCL is well-positioned to deliver sustained growth and shareholders' value. We believe that RCL stock is an ideal candidate for investors' portfolio addition.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.