The U.S. restaurant industry continues to be impacted by high wages, food cost inflation and traffic woes in 2024 after two years of strong growth. The Zacks defined Retail – Restaurants industry is currently in the bottom 41% of the Zacks Industry Rank. In the past year, the industry has declined 8.4%, while its year-to-date return is negative 12.7%.

The restaurant industry has been facing declining traffic for quite some time. A rapid increase in menu prices is the primary reason behind traffic erosion. Restaurant operators are grappling with the high cost of operations.

Intense competition, high wages and food cost inflation are concerning. The industry continues to bear increased expenses, which have been affecting margins. Higher pre-opening costs, marketing expenses and costs related to sales-boosting initiatives are exerting pressure on the company's margins.

Despite these headwinds, the Department of Commerce, in its June retail sales report, revealed that sales at restaurants and bars increased 4.4% year over year and 0.3% month over month.

Restaurant operators are trying to remain buoyant focusing on digital innovation, sales-building initiatives and cost-saving efforts. Restaurant operators constantly partner with delivery channels and digital platforms to drive incremental sales.

Meanwhile, a handful of restaurant stocks have flourished year to date, defying the industry's weak performance. Investment in these stocks with a favorable Zacks Rank and a possible earnings beat should provide more returns in the near future.

Our Top Picks

We have narrowed our search to two restaurant stocks that are poised to beat on earnings results this month. Each of these stocks carries either a Zacks Rank #1 (Strong Buy) or 2 (Buy) and has a positive Earnings ESP.

Our research shows that for stocks with the combination of a Zacks Rank #3 or better and a positive Earnings ESP, the chance of an earnings beat is as high as 70%. These stocks are anticipated to appreciate after their earnings release.

Texas Roadhouse Inc. TXRH is a full-service, casual dining restaurant chain offering assorted seasoned and aged steaks hand-cut daily on the premises and cooked to order over open gas-fired grills. TXRH operates restaurants under the Texas Roadhouse and Aspen Creek names.

TXRH offers its guests a selection of ribs, fish, seafood, chicken, pork chops, pulled pork and vegetable plates, an assortment of hamburgers, salads and sandwiches. TXRH also provides supervisory and administrative services for other licensed and franchise restaurants. Its second-quarter top line is likely to have been aided by productivity and margin enhancement initiatives and operational excellence across its restaurants.

Texas Roadhouse currently carries a Zacks Rank #2. TXRH reported positive earnings surprises in three out of the last four reported quarters. For second-quarter 2024, it has an Earnings ESP of +3.90%. The company will report on Jul 25, after the closing bell.

Image Source: Zacks Investment Research

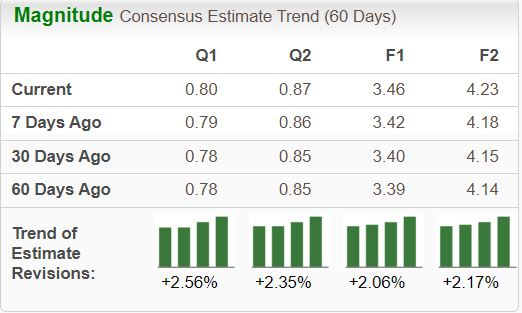

The stock has climbed 40.3% year to date. and has shown positive earnings estimate revisions in the last seven days. TXRH has an expected revenue and earnings growth rate of 15.3% and 33.3%, respectively, for the current year.

Image Source: Zacks Investment Research

Wingstop Inc. WING franchises and operates restaurants. WING's operating segment consists of the Franchise and Company segments. WING offers classic wings, boneless wings, and tenders that are cooked-to-order, and hand-sauced-and-tossed in various flavors.

WING's second-quarter 2024 results are likely to benefit from delivery channel expansion, menu innovation and digital marketing initiatives. Also, its supply-chain strategy and robust unit economics are adding to the positives.

Wingstop currently carries a Zacks Rank #1. WING reported positive earnings surprises in the last four reported quarters. For second-quarter 2024, it has an Earnings ESP of +3.08%. The company will report on Jul 31, before the opening bell.

Image Source: Zacks Investment Research

The stock has jumped 44% year to date. In the last seven days, WING has shown positive earnings estimate revisions. The expected revenue and earnings growth rate is 28.8% and 39.5%, respectively, for the current year.

Image Source: Zacks Investment Research

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.