Thesis: Cooper-Standard CPS is an auto parts supplier focused on sealing systems, fuel/brake delivery, and fluid transfer systems. The company was severely impacted by the downturn in new car volumes from 2018 to 2022 due to chip shortages, with revenues declining from $3.8 billion in 2017 to $2.3 billion in 2021. However, revenue has begun to rebound, reaching $2.8 billion in sales for 2023. In my view, CPS is just at the starting line; as car volumes revert to normalized levels, operating leverage will be significant, as detailed in the valuation section.

Thesis is based upon:

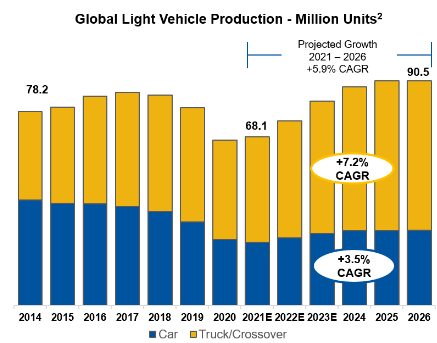

- Pent-up demand and an aging vehicle fleet: Combined with increased chip inflows, these factors are driving the rebound in new car production. The average car age is 12.5 years, marking an all-time high. As chip supply improves, Original Equipment Manufacturers (OEMs) are expected to aggressively compete for market share.

- Significant operating leverage: Cooper-Standard's business model benefits from high fixed costs, suggesting that even a modest revenue recovery can lead to exponential EPS growth.

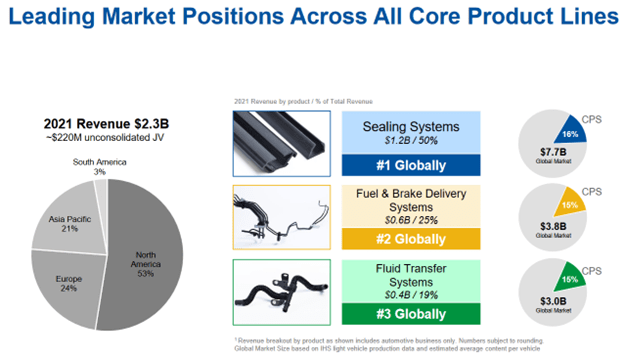

- Strong competitive position: The company has longstanding relationships with all major OEMs, holds the top position in sealing systems, and is ranked second in brake/fuel delivery.

Valuation: If industry volumes revert to normalized levels, Cooper-Standard should achieve their normalized operating numbers. In 2017, they generated $3.6 billion in sales and $125 million in net income. Assuming a trough 10x P/E multiple, the stock would be worth $70. If they hit their peak multiple of 20x normalized earnings, the stock could reach $140. There is clearly upside potential with the catalyst of increasing car volumes.

From 10k

The company achieved profitability with $11 million in net income 2 quarters ago and is expected to increase this figure due to operating leverage. It's important to note that the company now faces increased interest expenses due to refinancing its debt beyond 2026. The current interest expense is $70 million higher than during normalized years. However, this increase will be more than offset by cost reductions. Additionally, the company can carry over losses from last year, significantly lowering its income tax expense.

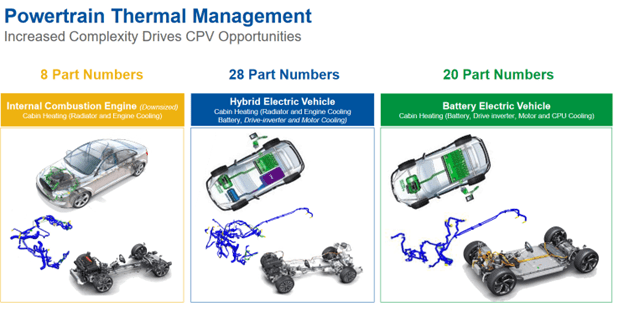

Company Overview: Cooper-Standard operates in three main segments: sealing systems, fuel/brake delivery systems, and fluid transfer systems. They are the global leader in sealing systems, second in fuel and brake delivery systems, and third in fluid transfer systems. They manufacture for most large car manufacturers, including Ford F, GM GM, and Tesla TSLA. Notably, CPS sells more parts for EVs and hybrids than internal combustion engines. This reduces the EV risk for Cooper-Standard and serves as a catalyst for growth. If EVs and hybrids become more popular, CPS's earnings projections may be conservative.

From 10k

Risks:

U.S. recession: A deep recession could decrease new car purchases. However, the average car age is at an all-time high, indicating pent-up demand. OEMs are likely to compete for market share by slashing prices, benefiting consumers. Additionally, new car financing offers lower rates than used car dealers, making new car purchases more attractive.

- Debt refinancing: Cooper-Standard successfully refinanced its debt in January 2022 during a challenging credit market. Assuming continued profitability, refinancing should not be an issue. They have assets to cover the loan, easing creditor concerns. Lowering interest rates over the next few years should also help reduce interest expenses and extend debt maturities.

- I believe Cooper Standard offers an asymmetric risk/reward opportunity to profit from the black swan event of the chip shortage cratering new car volumes.

I do not hold a position with the issuer such as employment, directorship, or consultancy.

I and/or others I advise hold a material investment in the issuer's securities.

Disclaimer:

This stock pitch is provided for informational purposes only and is not intended as investment advice. The analysis and opinions presented here are based on publicly available information as of the date of preparation and may be subject to change. The author, Andrew Marasco, is not a licensed financial advisor, and readers are encouraged to conduct their own research and consult with a qualified financial professional before making any investment decisions.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.