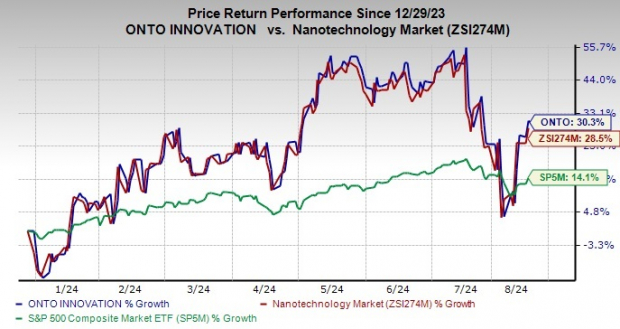

Onto Innovation's ONTO shares have been performing well on the trading front, with a gain of 30.3% year to date compared with the S&P 500 composite's and sub-industry's growth of 14.1% and 28.5%, respectively.

Solid financial performance has been aiding the stock's trajectory. The stock has gained 12% since announcing second-quarter fiscal 2024 results on Aug 8.

ONTO outpaced estimates in each of the trailing four quarters, with the average surprise being 6.6%.

The stock is trading down 16.7% from its 52-week high of $238.13, indicating further upside potential.

Headquartered in Wilmington, MA, Onto Innovation specializes in the design, development, manufacture and support of metrology and inspection tools primarily for semiconductor device fabricators, silicon wafer manufacturers and advanced packaging manufacturers in the semiconductor space.

Image Source: Zacks Investment Research

Factors Driving Growth

Onto Innovation's performance is gaining from increasing demand for its Dragonfly inspection system. Its Dragonfly G3 platform integrates 2D and 3D technologies to identify yield-killing defects and compute features, which are important for advanced front-end and packaging technologies.

The system is witnessing strong adoption owing to higher demand for advanced packaging of AI computing devices.

In the last reported quarter, total revenues of $242.3 million beat the Zacks Consensus Estimate by 2.9%. The top line expanded 27.1% year over year. The uptick was largely driven by the expansion of pilot lines for high-performance computing, which incorporates cutting-edge gate-all-around transistor architecture and high-bandwidth memory to support the growing demand in the AI sector.

Revenues surpassed the high end of the company's guided range of $230-$240 million. Management highlighted record revenues of $164 million from its specialty and advanced packaging customers. This growth was driven by demand from the company's AI packaging customers.

ONTO secured more than $300 million in volume purchase agreements from two major customers. These agreements, which extend through 2025, pertain to investments in AI advanced packaging and gate-all-around technologies.

Healthy momentum in advanced nodes sales was driven by the success of ONTO's Atlas and Iris systems. These systems are pivotal in supporting emerging gate-all-around devices.

In addition, ONTO bolstered its product portfolio with the introduction of the JetStep X500 lithography tool, specifically crafted for next-generation glass substrates used in panel-level packaging. The addition of these sensors will enable its users to collect important data needed to mature their process in a relatively shorter time.

The company remains focused on inventory reduction to boost cash-flow performance. Improvements in supply-chain initiatives are expected to drive margin performance.

For the third quarter, the management expects revenues in the range of $245-$255 million. For the second half, it now expects revenues to be 5-10% stronger than the first half of 2024.

ONTO expects revenues to gain from increasing investments in gate-all-around capacity, and capacity expansions by several high-bandwidth memory and logic packaging manufacturers in 2025.

Headwinds Persist

Nonetheless, weak global macro conditions, forex fluctuations and fierce competition are concerns for this Zacks Rank #3 (Hold) stock.

Increasing expenses is likely to weigh on the margin performance. For the third quarter of 2024, it expects operating expenses in the range of $64-$66 million amid higher research and development expenses.

A Look at Estimates

The Zacks Consensus Estimate for ONTO's 2024 and 2025 revenues is pegged at $968.9 million and $1.1 billion, respectively, indicating growth of 18.8% and 13.4% from the year-ago levels.

The consensus estimate for 2024 and 2025 EPS implies a rise of 37% and 22%, respectively, from the prior-year actuals to $5.11 and $6.24.

The consensus mark for 2024 EPS has increased 2%, in the past 90 days.

Stocks to Consider

Some better-ranked stocks worth consideration in the broader technology space are Badger Meter BMI, Manhattan Associates MANH and ANSYS ANSS. Badger Meter and Manhattan Associates sport a Zacks Rank #1 (Strong Buy) each, while ANSYS carries a Zacks Rank #2 (Buy), at present.

The Zacks Consensus Estimate for Badger Meter's 2024 EPS is pegged at $4.06, up 4.4% in the past 30 days. BMI's earnings beat the Zacks Consensus Estimate in each of the last four quarters, the average surprise being 12.9%. The long-term earnings growth rate is 17.9%. Its shares have risen 17.1% in the past year.

The Zacks Consensus Estimate for ANSS' 2024 earnings is pegged at $9.72, up 3.7% in the past 30 days. ANSS' earnings beat the Zacks Consensus Estimate in three of the last four quarters while missing once, with the average surprise being 4.8%. Its shares have risen 7.7% in the past year.

The Zacks Consensus Estimate for MANH's 2024 EPS is pegged at $4.26. MANH's earnings beat the Zacks Consensus Estimate in each of the last four quarters, with the average surprise being 26.6%. The stock has surged 30.7% in the past year.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.