Canadian Pacific Kansas City's CP operations are being boosted by its robust operational efficiency and cost-cutting initiatives. Shareholder-friendly actions bode well for the company. High fuel costs and weak liquidity are major concerns.

Factors Favoring CP

Canadian Pacific's operational efficiency is commendable, as evidenced by the company's robust performance in the second quarter of 2024. The average terminal dwell decreased by 9%, highlighting improved processing and handling operations. The network's fluidity is demonstrated by a 6% increase in average train speed. Locomotive productivity rose by 10%, while fuel efficiency saw a 2% enhancement, reflecting CP's strong commitment to both operational excellence and sustainability.

The company is benefiting from its proactive cost-cutting initiatives. Labor costs, comprising 26.2% of the overall operating expenses, decreased by 7% year over year in the second quarter of 2024 to $612 million.

CP's commitment to reward its shareholders through dividends amid uncertainties reflects its financial confidence.With dividend payouts increasing from C$507 million in 2021 to C$707 million in 2022 and 2023, its financial growth and a proactive approach to rewarding shareholders is underscored. In the second quarter of 2024, the company paid out a quarterly dividend of 19 cents per share to its shareholders.

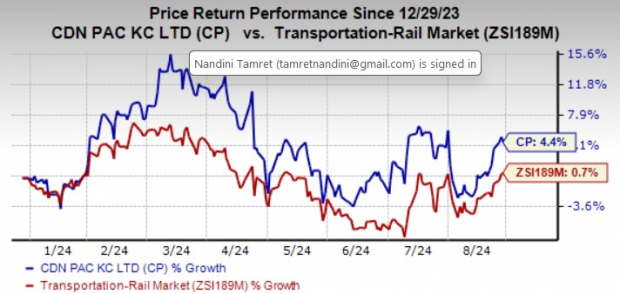

Shares of Canadian Pacific have rallied 4.4% year to date compared with its industry's growth of 0.7% in the same period.

Image Source: Zacks Investment Research

Key Risks Faced by CP

High fuel costs are a worry.In the second quarter of 2024, fuel costs rose by 17% year over year.

Canadian Pacific exited the June end quarter with $557 million in cash and cash equivalents while carrying a current debt load of $3.67 billion. This discrepancy suggests that the company does not have enough cash to meet its short-term obligations.

CP's current ratio (a measure of liquidity) at the end of the second quarter of 2024 was 0.51. A current ratio of less than 1 indicates that the company is likely to struggle to meet its short-term obligations.

CP's Zacks Rank

Canadian Pacific currently carries a Zacks Rank #3 (Hold).

Stocks to Consider

Some better-ranked stocks for investors' consideration in the Zacks Transportation sector include C.H. Robinson Worldwide and Westinghouse Air Brake Technologies.

C.H. Robinson Worldwide currently sports a Zacks Rank #1 (Strong Buy). CHRW has an expected earnings growth rate of 25.2% for the current year.

The company has an impressive earnings surprise history. Its earnings outpaced the Zacks Consensus Estimate in three of the trailing four quarters and missed once, delivering an average surprise of 7.3%. Shares of CHRW have risen 9.9% in the past year.

WAB holds a Zacks Rank #2 (Buy) at present andhas an expected earnings growth rate of 26% for the current year.

The company has an encouraging track record with respect to the earnings surprise, having surpassed the Zacks Consensus Estimate in each of the trailing four quarters. The average beat is 11.8%. Shares of WAB have climbed 46.2% in the past year.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.