Serve Robotics SERV shares have declined 37% in the past month, underperforming the Zacks Computer & Technology sector's gain of 4.5% and the Zacks IT Services industry's return of 3.2%.

Shares of this AI-powered last-mile robot delivery service provider saw significant volatility since its public equity offering on April 18, from when it started trading on the Nasdaq Capital Market under the ticker "SERV."

Since then, SERV shares have jumped 197.8%. However, the sluggish second-quarter 2024 results saw shares dropping 9.8% since Aug. 13.

SERV reported revenues of $0.47 million, significantly better than the $0.06 million reported in the year-ago quarter but plunging 50.5% sequentially.

The massive quarter-over-quarter drop panicked investors despite an 80% jump in second-quarter delivery and branding revenues. Daily Supply Hours surged 28% sequentially.

SERV Shares Lag Sector Past Month

Image Source: Zacks Investment Research

The recent dip in SERV shares brings this question into investors' minds - is this the right time to jump into the stock? Let's dig deep to find out.

Serve Robotics Rides on Strong Last-Mile Delivery Prospects

SERV's long-term prospects ride on growing demand for last-mile delivery of food and other items on partner platforms that include Uber Eats and 7-Eleven. The company, which was spun off from Uber Technologies in 2021, counts NVIDIA, Uber, 7-Ventures and Delivery Hero's corporate venture units as its strategic investors.

SERV's strong liquidity position is expected to help it execute its long-term strategic plan that includes the deployment of 2000 robots across the United States in 2025. It has already completed the design phase for the third-generation robot.

Serve Robotics generated $35.8 million in gross proceeds from the successful public equity offering and $15 million from a private placement. As of June 30, 2024, SERV had cash and cash equivalents of $28.8 million. Most recently, it raised another $20 million.

Serve Robotics believes robots have the potential to reduce the average delivery cost to under $1, lower than the delivery cost by human couriers currently, making on-demand delivery more affordable and accessible in the areas in which it operates.

Per the ARK Invest report, the potential market for food and parcel delivery by robots and drones is expected to hit $450 billion globally in 2030.

SERV's expanding robotics offering is expected to improve its competitive position in the last-mile delivery space currently dominated by the likes of DoorDash and Amazon.

Serve Robotics' expanding partner base that includes Shake Shack, Ouster and Magna are noteworthy. In June 2024, SERV announced the expansion of its delivery operations into Koreatown and began onboarding new local merchants through its partnership with Uber Eats. Its latest partnership with SHAK expands SERV's footprint in Los Angeles.

It expects to deploy 250 robots by the end of the first quarter of 2025 in Los Angeles. Other cities that include its expansion plan are San Diego, Dallas and Vancouver.

Magna has become a contract manufacturer for SERV's technology, and the first robots are expected to roll off the production line by the end of the fourth quarter of 2024.

What Should Investors Do With SERV Stock?

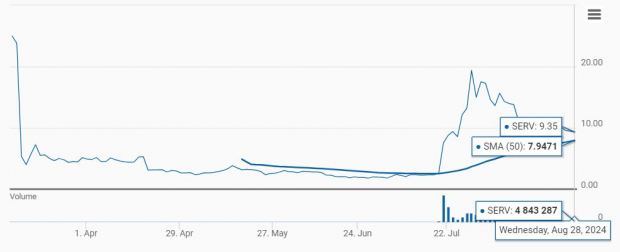

Technical indicator is bullish for SERV as the shares are trading above the 50-day moving average.

SERV Trades Above 50-Day SMA

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for SERV's earnings 2024 have shown improvement as the figure is now expected to be a loss of 85 cents, a penny narrower over the past 30 days.

Serve Robotics Inc. Price and Consensus

Serve Robotics Inc. price-consensus-chart | Serve Robotics Inc. Quote

However, SERV stock is overvalued at this current moment, as suggested by the Value Score of F.

SERV's revenue decline on a sequential basis in the second quarter of 2024 has been a concern. It suffers from customer concentration, with one customer accounting for 74% of accounts receivable as of June 30, 2024.

SERV's expanding robotics fleet bodes well for long-term investors. Hence, investors who already own the stock may expect the company's growth prospects to be rewarding over the long term.

Although the dip looks like an opportunity, we believe SERV is a risky venture right now, given manifold challenges.

Serve Robotics currently has a Zacks Rank #3 (Hold), suggesting that it may be wise to wait for a more favorable entry point in the stock.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.