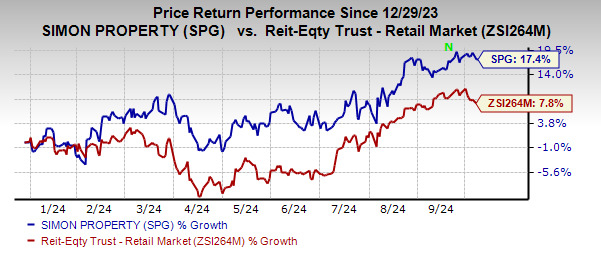

Shares of Simon Property Group SPG have soared 17.4%% in the year-to-date period compared with its industry's growth of 7.8%.

This retail real estate investment trust's (REITs) portfolio of premium retail assets in the United States and abroad, the adoption of omnichannel retailing, focus on mixed-use developments and healthy balance sheet strength have enabled it to ride the growth curve so far.

Image Source: Zacks Investment Research

Let us now decipher the factors behind the increase in the stock price and check whether the trend will last.

Simon Property enjoys a wide exposure to retail assets across the United States. Moreover, the company's international presence fosters sustainable long-term growth as compared with its domestically-focused peers. Its ownership stake in Klépierre facilitates the expansion of its global footprint, which gives it access to premium retail assets in the high barrier-to-entry markets of Europe. We believe that diversification, with respect to both product and geography, will help it grow over the long term.

In the first half of 2024, it signed 572 new leases and 1,251 renewal leases (excluding mall anchors and majors, new development, redevelopment and leases with terms of one year or less) with a fixed minimum rent across its U.S. Malls and Premium Outlets portfolio.

Given the favorable retail real estate environment, this leasing momentum is expected to continue in the upcoming quarters. As of June 30, 2024, the ending occupancy for the U.S. Malls and Premium Outlets portfolio came in at 95.6%, up 90 basis points from 94.7% as of June 30, 2023. We project the 2024 year-end occupancy for this portfolio to be 95.7%.

Simon Property's adoption of an omni-channel strategy and successful tie-ups with premium retailers have paid off well. Its online retail platform, coupled with an omnichannel strategy, is likely to be accretive to its long-term growth. The company is also focused on tapping its growth opportunities by assisting digital brands enhance their brick-and-mortar presence.

Also, its efforts to explore the mixed-use development option, which has gained immense popularity in recent years, has enabled it to tap the growth opportunities in areas where people prefer to live, work and play.

SPG's Balance Sheet & ROE

The retail REIT maintains a healthy balance sheet position and has $11.2 billion of liquidity as of the end of the second quarter of 2024. As of June 30, 2024, Simon Property's total secured debt to total assets was 17%, while the fixed-charge coverage ratio was 4.3, ahead of the required level.

SPG also enjoys a corporate investment-grade credit rating of A- from Standard and Poor's and a senior unsecured rating of A3 from Moody's, rendering it favorable access to the debt market. The company's solid financial footing with ample financial flexibility is likely to support its growth endeavors going forward.

In addition, SPG's trailing 12-month return on equity is 78.14% compared with the industry's average of 6.28%. This reflects that the company is more efficient in using shareholders' funds than its peers.

SPG's Dividend Payments

Solid dividend payouts are a massive enticement for REIT investors, and SPG has remained committed to boosting shareholder wealth. Encouragingly, the company has raised its dividend payout 11 times in the last five years, with the latest hike being announced in August 2024, concurrent with the second-quarter 2024 earnings release.

Given SPG's solid operating platform, opportunities for growth, and decent financial position compared with the industry, we expect the dividend rate to be sustainable in the upcoming period.

Risks Likely to Affect SPG's Positive Trend

rowing e-commerce adoption is likely to adversely impact the market share for brick-and-mortar stores and affect retail REITs including Simon Property. Limited consumers' willingness to spend amid macroeconomic uncertainty poses key near-term concerns for the company.

Stocks to Consider

Some better-ranked stocks from the retail REIT sector are Brixmor Property Group BRX and Tanger, Inc. SKT, each carrying a Zacks Rank #2 (Buy) at present.

The Zacks Consensus Estimate for Brixmor's 2024 FFO per share is pinned at $2.13, suggesting year-over-year growth of 4.4%.

The Zacks Consensus Estimate for Tanger's 2024 FFO per share stands at $2.09, indicating an increase of 6.6% from the year-ago reported figure.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.