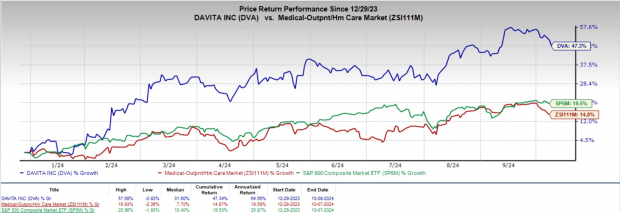

DaVita, Inc. DVA has witnessed strong momentum year to date, with its shares up 47.3% compared with the industry's growth of 14.8%. The S&P 500 composite has risen 19.5% in the same period.

DaVita, carrying a Zacks Rank #2 (Buy) at present, is witnessing an upward trend in its stock price, prompted by the company's business model. The optimism, led by a solid second-quarter 2024 performance and the acquisition of dialysis centers, is expected to contribute further.

DaVita is a leading provider of dialysis services in the United States to patients suffering from chronic kidney failure, also known as end-stage renal disease (ESRD). The company operates kidney dialysis centers and provides related medical services, primarily in dialysis centers and contracted hospitals across the country. Its services include outpatient dialysis services, hospital inpatient dialysis services and ancillary services such as ESRD laboratory services and disease management services.

Image Source: Zacks Investment Research

Catalysts Driving DaVita's Growth

The rally in the company's share price can be attributed to the strength of its dialysis and related lab services. The optimism led by a solid second-quarter 2024 performance and robust business potential are expected to contribute further.

DaVita is experiencing significant growth driven by its patient-centric care approach, leveraging its kidney care services platform to offer a wide range of treatment models and modalities. The increasing prevalence of value-based partnerships in kidney health enables nephrologists, physicians, and transplant programs to collaborate more effectively, enhancing the understanding of individual patient needs and facilitating improved care coordination and early interventions.

A key element of DaVita's growth strategy is the acquisition of dialysis centers and related businesses, as evident from the recent extension of its pilot phase for a supply and collaboration agreement with Nuwellis. Upon completion of this phase, which ends on Aug. 31, 2024, DaVita may extend the agreement for the ongoing provision of inpatient and outpatient ultrafiltration services for up to 10 years.

The company's global market share is also on the rise, with recent agreements to expand operations into Brazil, Colombia, Chile and Ecuador.

In the second quarter of 2024, DaVita reported results that exceeded expectations, showcasing a positive trend in both revenue streams and patient services. The sequential increase in daily United States dialysis treatments and the opening of new centers, along with acquisitions overseas, indicates a strong growth trajectory.

Furthermore, DaVita has raised its earnings projections for fiscal 2024, now forecasting adjusted EPS in the range of $9.25 to $10.05, up from the prior range of $9 to $9.80, which is likely to attract further interest from investors.

Risk Factor

DaVita faces a risk of reduced profitability if patients shift from commercial insurance to government programs, as government reimbursement rates are significantly lower. This shift could be triggered by rising unemployment, impacting DaVita's revenues and profit margins.

A Look at Estimates

The Zacks Consensus Estimate for DaVita's 2024 and 2025 bottom line projects an 18% and 14.4% year-over-year improvement, respectively, to earnings of $9.99 and $11.42 per share.

In the past 30 days, the Zacks Consensus Estimate for the company's 2024 earnings has remained constant at $9.99 per share.

Revenues for 2024 and 2025 are anticipated to rise 5.4% and 4%, respectively, to $12.8 billion and $13.3 billion on a year-over-year basis.

DaVita Inc. Price

DaVita Inc. price | DaVita Inc. Quote

Other Key Picks

Some other top-ranked stocks in the broader medical space are Rockwell Medical RMTI, Quest Diagnostics DGX and RadNet RDNT. While Rockwell Medical carries a Zacks Rank #1 (Strong Buy), Quest Diagnostics and RadNet carry a Zacks Rank #2 each at present.

Rockwell Medical earnings surpassed estimates in each of the trailing four quarters, with the average being 87.9%.

RMTI's shares have gained 79.7% compared with the industry's 10.7% growth year to date.

Quest Diagnostics has an estimated long-term growth rate of 6.8%. DGX's earnings surpassed estimates in each of the trailing four quarters, with the average being 3.3%.

Quest Diagnostics has gained 7.9% compared with the industry's 14.9% growth year to date.

RadNet's earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 98.2%.

RDNT's shares have gained 93.7% year to date compared with the industry's 14.8% growth.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.