American Tower Corporation's AMT extensive and geographically diversified communication real estate portfolio positions it well to ride the growth curve amid rising capital spending by wireless carriers on the incremental demand from global 4G and 5G deployment efforts.

Its expansionary efforts and disciplined capital-allocation strategy augur well for long-term growth. However, customer concentration poses a key concern for the company.

What's Aiding AMT Stock?

With the advancement in mobile technology, such as 4G and 5G networks, and the proliferation of bandwidth-intensive applications, mobile data usage has increased significantly globally. The excessive use of network-intensive applications for video conferencing, cloud services and hybrid-working scenarios is likely to fuel the rise.

This has led to greater capital spending by wireless carriers due to the incremental demand from global 4G and 5G deployment efforts, growing wireless penetration and spectrum auctions, driving demand for AMT's wireless communication infrastructure. This upbeat trend is likely to continue in the upcoming period, boosting demand for the company's assets and driving healthy leasing activity.

American Tower has a solid track record of delivering healthy performance due to the robust demand for its global macro-tower-oriented asset base. It has witnessed strong growth in key financial metrics while continuing platform expansion.

In the second quarter of 2024, the company recorded healthy year-over-year organic tenant billings growth of 5.3% and total tenant billings growth of 6.1%. Also, in the second quarter, revenues from the property segment and adjusted EBITDA increased 4.6% and 8.1% on a year-over-year basis, respectively. Between 2013 and 2023, American Tower's revenues from the property segment and adjusted EBITDA witnessed a CAGR of 12.8% and 12.5%, respectively. Amid secular growth trends in the wireless industry, the healthy performance is expected to continue in 2024 and beyond.

To capitalize on the secular trends of the industry, AMT is consistently focusing on macro-tower investment opportunities and expansionary efforts across global markets. For 2023, the company shelled out approximately $168 million to acquire communications sites, previously subleased sites in the United States and other communications-related infrastructure globally.

AMT's Ample Liquidity

Apart from having a robust operating platform, American Tower has ample liquidity to support its debt servicing. Its consistent adjusted EBITDA margins and revenue growth, as well as favorable return on invested capital, indicate strength in its underlying core business and support its ability to manage its near-term obligations.

As of June 30, 2024, the company had $9.17 billion in total liquidity, and its net leverage ratio was 4.8. In addition, with a weighted average remaining term of debt of 5.8 years, it has decent financial flexibility.

AMT's Sustainable Dividend Payouts

American Tower has a disciplined capital allocation strategy and remains committed to increasing shareholder value through regular dividend hikes. In the last five years, American Tower increased its dividend 17 times, and the annualized dividend growth rate for this period is 12.74%. Moreover, it has a lower dividend payout compared with its industry. Such disbursements highlight its operational strength and commitment to rewarding shareholders handsomely.

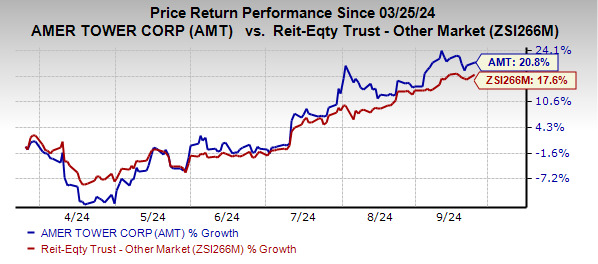

Shares of this Zacks Rank #3 (Hold) company have rallied 20.8% in the past six months, outperforming the industry's growth of 17.6%.

Image Source: Zacks Investment Research

What's Affecting AMT Stock?

American Tower has a high customer concentration, with T-Mobile, AT&T and Verizon Wireless contributing 17%, 16% and 12%, respectively, of its property revenues for 2023. The loss of TMUS, T or Verizon Wireless as customers, consolidation among them or reduction in network spending could adversely impact the company's top-line growth.

The merger between T-Mobile and Sprint, which closed in April 2020, resulted in tower site overlap for American Tower. During the first half of 2024, the churn was roughly 2% of its tenant billings, mainly driven by the churn in its U.S. & Canada property segment.

Given the contractual lease cancellations and non-renewals by T-Mobile, including legacy Sprint Corporation leases, management expects the churn rate in its U.S. & Canada property segment to remain elevated through 2025.

Although the Federal Reserve has announced a rate cut, the interest rate is still high and is a concern for American Tower. Elevated rates imply a higher borrowing cost for the company, which would affect its ability to purchase or develop real estate. American Tower has a substantial debt burden, and its total debt, as of June 30, 2024, was approximately $38.97 billion.

Stocks to Consider

Some better-ranked stocks from the broader REIT sector are Lamar Advertising LAMR and Four Corners Property Trust FCPT, each carrying a Zacks Rank #2 (Buy) at present.

The Zacks Consensus Estimate for Lamar's 2024 FFO per share is pinned at $8.09, suggesting year-over-year growth of 8.3%.

The Zacks Consensus Estimate for Four Corners' 2024 FFO per share stands at $1.73, indicating an increase of 3.6% from the year-ago reported figure.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.