The holiday-shortened first week of July provided a solid reversal, however, and traders will be undoubtedly be keenly watching each earnings report for signs of where markets go from here. Any early mixed results are almost certain to keep volatility high unless a series of strong cross-sector beats emerges.

Sentiment: Negative

Volatility: Moderate (VIX 23-37)

Direction: Highly Negative

[Click to Enlarge/ Weekly ETF Analyses/ Prior Monthly Summaries/ Mrkt Rotation Selections]

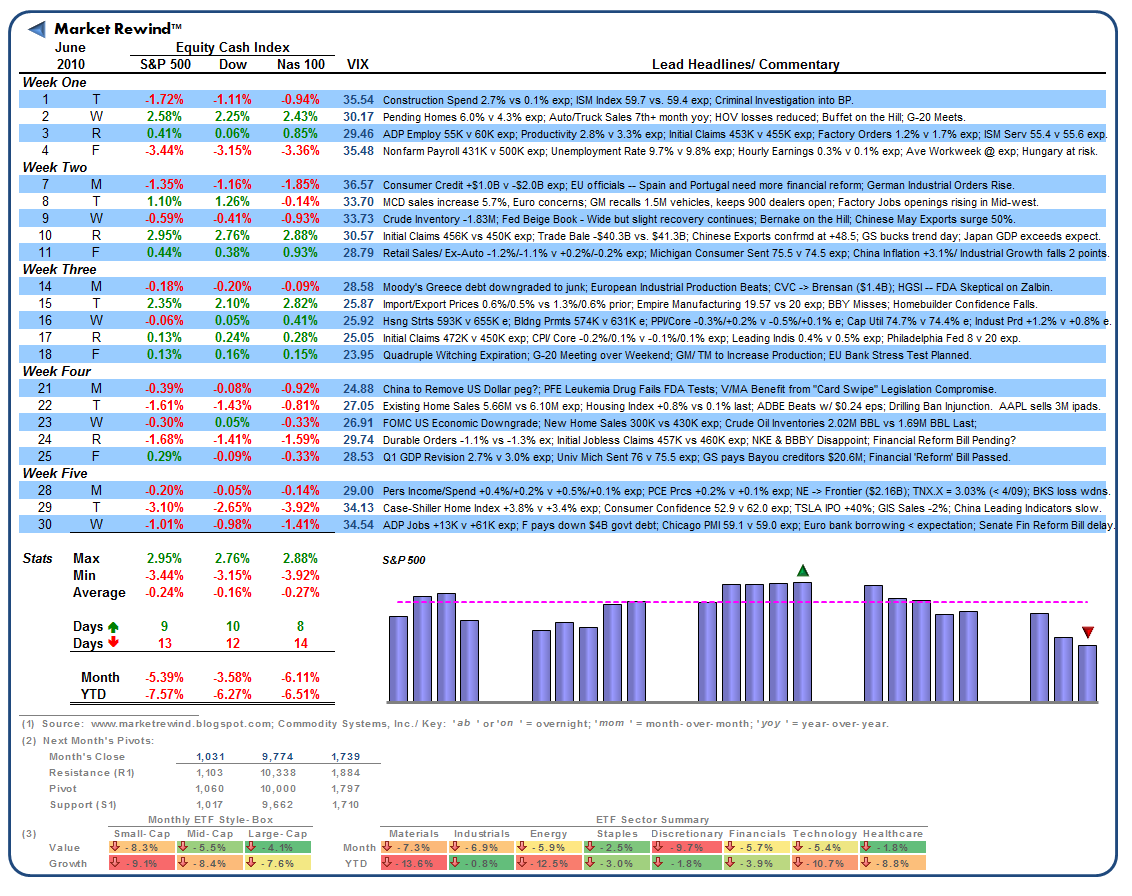

The Style-Box was calculated using the following PowerShares™ ETFs: Small-Growth (PWT), Small-Value (PWY), Mid-Growth (PWJ), Mid-Value (PWP), Large-Growth (PWB), and Large-Value (PWV). The Sector-Ribbon was calculated using the following Select Sector SPDR™ ETFs: Materials (XLB), Industrials (XLI), Energy (XLE), Staples (XLP), Discretionary (XLY), Financials (XLF), Technology (XLK), and Healthcare (XLV). The Standard & Poors 500, Dow Jones Industrial Average and NASDAQ 100 may be traded through ETF proxies, including the SPY or IVV, DIA and QQQQ, respectively.

PWPPerella Weinberg Partners

$23.02-2.66%

PWVInvesco Large Cap Value ETF

$59.76-0.58%

XLBMaterials Select Sector SPDR

$88.51-0.84%

XLESPDR Select Sector Fund - Energy Select Sector

$90.74-0.55%

XLFSPDR Select Sector Fund - Financial

$51.16-0.73%

XLISPDR Select Sector Fund - Industrial

$137.43-0.85%

XLKSPDR Select Sector Fund - Technology

$234.82-0.64%

XLPSPDR Select Sector Fund - Consumer Staples

$80.39-0.28%

XLVSPDR Select Sector Fund - Health Care

$146.500.32%

XLYSPDR Select Sector Fund - Consumer Discretionary

$223.54-0.11%

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in