Year 4, Week 9 Major Position Changes

To see historic weekly fund changes click here OR the label at the bottom of this entry entitled 'fund positions'.

Cash: 62.6% (v 63.7% last week)

18 long bias: 25.2% (v 25.9% last week)

7 short bias: 12.1% (v 10.4% last week) [Note: Long bond, long dollar, and volatility positions considered 'short']

25 positions (vs 29 last week)

Weekly thoughts

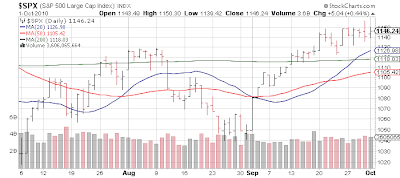

Same old story - all news is good news as long as the Bernanke Put is in play. The questions go forward is how much is QE2 now in the market after a big run, and how many times can we rally on the same backdrop? Economic data picks up this week, and earnings season kicks off although just a few names- the market is well overdue for at least a modest pullback, but until the psychology changes it is hard to front run. Key levels on S&P 500 are now 1118 (up from 1116) [the 200 day simple moving average], 1131, and 1150. Over 1150, 1170 comes into play... below 1116, 1090 comes into play.

Last week some of the leadership stocks - massively overextended - finally took a bit of a break, but speculators simply rolled into the energy complex, driving up oil itself, solars stocks and some of the oil and oil service names. Natgas (reliant on U.S. demand) remains a disaster.

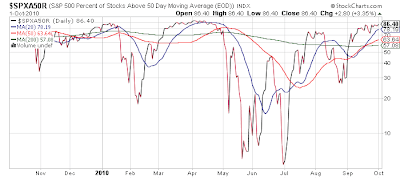

Complacency is high at this point, as those looking for "a pullback" the previous 2-3 weeks appear to have thrown in the towel. This is a necessary step in the sentiment turn. The percent of S&P 500 stocks trading over their 50 day moving average is now reaching extreme levels - closing in on 90%.

Other than the very atypical period of mid March - mid April when the "V shaped" recovery was still the calling card of the bulls, this type of condition does not usually last too long. So now we see what is more powerful - the pledge of free money from the Fed to manipulate asset prices upward (current thesis) or the belief by the majority that a normalized return to economic activity was right around the corner (late winter/early spring 2010 thesis)

-------------------------------

Economic data continued to matter little last week as good news = good news, and bad news = more QE. This will continue until it doesn't - as simple minded as it seems. At some point weaker economic news will matter, and many economic data points have stagnated or retreated to the worse levels of the past 6-7 months. This week the 2 key reports will be ISM Services (much more an indicator of U.S. activity than ISM Manufacturing) and the labor data on Friday. Thus far the U.S. has created "net" 800K jobs in 2010... but if you sniff around the birth death model and added up all the "gains" in businesses too small to count, I bet it would come in around 800K year to date.

Monday: (10 AM) Factory Orders (10 AM) Pending Home Sales

Tuesday: (10 AM) ISM Non Manufacturing

Wednesday: (premarket) ADP Employment

Thursday: (premarket) Weekly jobless claims (3 PM) Consumer Credit

Friday: (premarket) Monthly labor data

-------------------------------

Portfolio

The market did not go anywhere last week on the whole, but it remained a difficult environment to make any ground on the short side. The biggest wins were in a few of the "superstar" stocks that finally fell back but the timing had to be precise as those were the same stocks crushing shorts for 5 weeks straight. The dollar continued to be crushed, and most commodities continued to rally - even the maligned energy sector picked up as speculators rotated into lagging groups. Much like the "hot money" left the tech stock superstars once they were 'marked up' at quarter end, so did they leave agricultural commodities Friday. We'll see if it's a 1 day wonder or a canary in the coal mine.

In the portfolio weightings were similar to previous week with a small uptick in short exposure - almost all short exposure at this time are pseudo shorts (long bond, long dollar, long volatility) because betting against the market in any form has been extreme pain for the past month. A break of S&P 1116 will have me looking for a 'big win' trade down to 1090, and that along with a SPY put position should help us make some gains on the downside when the day comes. Most likely the move will come in premarket so I expect it to be hard to catch. On the long side I cut some longer term positions that have simply run so far, and even on a decent pullback are far too expensive. With earnings season coming many of these stocks have to perform to perfection to avoid some implosions. Expectations are off the chart, based on stock prices.

On the long side:

On the short side:

To see historic weekly fund changes click here OR the label at the bottom of this entry entitled 'fund positions'.

Cash: 62.6% (v 63.7% last week)

18 long bias: 25.2% (v 25.9% last week)

7 short bias: 12.1% (v 10.4% last week) [Note: Long bond, long dollar, and volatility positions considered 'short']

25 positions (vs 29 last week)

Weekly thoughts

Same old story - all news is good news as long as the Bernanke Put is in play. The questions go forward is how much is QE2 now in the market after a big run, and how many times can we rally on the same backdrop? Economic data picks up this week, and earnings season kicks off although just a few names- the market is well overdue for at least a modest pullback, but until the psychology changes it is hard to front run. Key levels on S&P 500 are now 1118 (up from 1116) [the 200 day simple moving average], 1131, and 1150. Over 1150, 1170 comes into play... below 1116, 1090 comes into play.

Last week some of the leadership stocks - massively overextended - finally took a bit of a break, but speculators simply rolled into the energy complex, driving up oil itself, solars stocks and some of the oil and oil service names. Natgas (reliant on U.S. demand) remains a disaster.

Complacency is high at this point, as those looking for "a pullback" the previous 2-3 weeks appear to have thrown in the towel. This is a necessary step in the sentiment turn. The percent of S&P 500 stocks trading over their 50 day moving average is now reaching extreme levels - closing in on 90%.

Other than the very atypical period of mid March - mid April when the "V shaped" recovery was still the calling card of the bulls, this type of condition does not usually last too long. So now we see what is more powerful - the pledge of free money from the Fed to manipulate asset prices upward (current thesis) or the belief by the majority that a normalized return to economic activity was right around the corner (late winter/early spring 2010 thesis)

-------------------------------

Economic data continued to matter little last week as good news = good news, and bad news = more QE. This will continue until it doesn't - as simple minded as it seems. At some point weaker economic news will matter, and many economic data points have stagnated or retreated to the worse levels of the past 6-7 months. This week the 2 key reports will be ISM Services (much more an indicator of U.S. activity than ISM Manufacturing) and the labor data on Friday. Thus far the U.S. has created "net" 800K jobs in 2010... but if you sniff around the birth death model and added up all the "gains" in businesses too small to count, I bet it would come in around 800K year to date.

Monday: (10 AM) Factory Orders (10 AM) Pending Home Sales

Tuesday: (10 AM) ISM Non Manufacturing

Wednesday: (premarket) ADP Employment

Thursday: (premarket) Weekly jobless claims (3 PM) Consumer Credit

Friday: (premarket) Monthly labor data

-------------------------------

Portfolio

The market did not go anywhere last week on the whole, but it remained a difficult environment to make any ground on the short side. The biggest wins were in a few of the "superstar" stocks that finally fell back but the timing had to be precise as those were the same stocks crushing shorts for 5 weeks straight. The dollar continued to be crushed, and most commodities continued to rally - even the maligned energy sector picked up as speculators rotated into lagging groups. Much like the "hot money" left the tech stock superstars once they were 'marked up' at quarter end, so did they leave agricultural commodities Friday. We'll see if it's a 1 day wonder or a canary in the coal mine.

In the portfolio weightings were similar to previous week with a small uptick in short exposure - almost all short exposure at this time are pseudo shorts (long bond, long dollar, long volatility) because betting against the market in any form has been extreme pain for the past month. A break of S&P 1116 will have me looking for a 'big win' trade down to 1090, and that along with a SPY put position should help us make some gains on the downside when the day comes. Most likely the move will come in premarket so I expect it to be hard to catch. On the long side I cut some longer term positions that have simply run so far, and even on a decent pullback are far too expensive. With earnings season coming many of these stocks have to perform to perfection to avoid some implosions. Expectations are off the chart, based on stock prices.

On the long side:

- Monday, started Chinese Home Inns & Hotel Management (HMIN) on a technical breakout - if I was a very short term trader I could have been in and out of this position with a quick 6% gain, as the chart had laid out. But once it did that, it stalled and fell back.

- Tuesday, Cleveland Cliffs (CLF) was sold as it was stalling. However, as speculators moved into lagging names the stock ran with the 'energy' complex late in the week so thus far a bad sale.

- As the S&P 500 fell back to 1131 area of support, I bought some SPY Calls with intent to sell 10-15 points higher (from 1133). This played out very quickly, indeed within hours - but my fill price on the options was horrid and a 30%+ some gain was barely double digits.

- Added to Spreadtrum Communications (SPRD) on a sharp pullback to the 20 day moving average.

- Thursday at the open, closed out 3 "market general" positions in Netflix (NFLX), Amazon.com (AMZN), Priceline.com (PCLN). In retrospect shorting all 3 would have worked out quite well, but you never know when these sort of stocks will finally exhaust themselves...

- Closed Thoratec (THOR) for non performance and reversing a breakout.

- Sold 20% of BorgWarner (BWA) to lock in gains, and 66% of Powershares DB Double Long Gold (DGP) as the commodity has been on fire.

- Added to Acme Packet (APKT) on a pullback to the 20 day moving average.

- A limit order for Salesforce.com (CRM) hit at a "gap" which coincided with the 50 day moving average; a tight stop loss was put in in case this is part of a larger move down.

On the short side:

- Goldman Sachs downgraded Intuitive Surgical (ISRG), so Monday half the position was covered, and Tuesday the other half - together about a 3% gain. Not much but in this market it's a victory to make money on anything on the short side.

- Wednesday, shorted a second leg in Whirpool (WHR) as the stock reached closer to resistance levels. The company actually warned on the year the next day, but speculators did not care as the stock barely budged.

- Restarted a position in the much hated U.S. dollar with Powershares DB U.S. Dollar (UUP) - this is being used as a hedge and for a trade, not a long term position.

BWABorgWarner Inc

$29.49-2.51%

CLFCleveland-Cliffs Inc

$11.35-5.26%

CRMSalesforce Inc

$310.39-2.52%

DGPDB Gold Double Long ETN due February 15, 2038

$81.46-0.19%

ISRGIntuitive Surgical Inc

$591.79-2.44%

NFLXNetflix Inc

$1002.27-2.17%

UUPInvesco DB USD Index Bullish Fund ETF

$29.080.35%

WHRWhirlpool Corp

$104.80-1.20%

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted In:

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in