The world's greatest contrarian/fundamentalist investor, Warren Buffet, spoke about derivatives in 2002 at a Berkshire Hathaway annual report. Mr. Buffet was well aware of the increasing volatility and wealth destruction of Exchange Traded Funds (ETFs) regarding all major global market places. After May's flash crash, when the machines took over, his thesis and sentiment is gaining support, considering the NYSE's ETF volume amounts to 70-80% of all volume on the exchange.

In his 2002 Berkshire Hathaway annual report, Warren Buffet wrote: “I view derivatives as time bombs, both for the parties that deal in them and the economic system.” Elsewhere, “Unless derivatives contracts are collateralized or guaranteed, their ultimate value also depends on the creditworthiness of the counter-parties to them.” Buffet also notes, “In my view, derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal.”

What is a ETF?

An ETF is fund that tracks an index, but can be traded like a stock. ETFs always bundle together the securities that are in an index; they never track actively managed mutual fund portfolios (because most actively managed funds only disclose their holdings a few times a year, so the ETF would not know when to adjust its holdings most of the time). Investors can do just about anything with an ETF that they can do with a normal stock, such as short selling. Because ETFs are traded on stock exchanges, they can be bought and sold at any time during the day (unlike most mutual funds). Their price will fluctuate from moment to moment, just like any other stock's price, and an investor will need a broker in order to purchase them, which means that he/she will have to pay a commission. On the plus side, ETFs are more tax-efficient than normal mutual funds, and since they track indexes they have very low operating and transaction costs associated with them. There are no sales loads or investment minimums required to purchase an ETF, according to InvestorWords.com

Historical Significance

The first exchange traded fund (ETF) appeared in the United States as the S&P 500 Depository Receipts SPY in 1993. Before this U.S. entry, the very first ETF was in Canada as the Toronto Index Participation Fund. By 2002 there were 246 domestic and foreign ETFs across the globe, and the United States had 102, or 41% of ETFs outstanding. By the end of 2008, there were 747 ETFs, and 164 ETFs were launched in 2008 alone.

ETF Designers

ETF assets comprised approximately $534 billion, by the end of 2008 alone. Three ETF designers that had a virtual oligopoly over the industry (approximately 86%) were The Vanguard Group, SSgA, and Barclays Global Investors. Up-and-coming ETF companies like iShares, RevenueShares, and Direxion have also been making their derivative presence known, especially within the 200 and 300 percent leveraged ETFs that are gaining popularity.

Types of ETFs

Actively Managed ETFs

Bond ETFs

Commodity ETFs or ETCs

Currency ETFs or ETCs

Exchange Traded Grantor Trusts

Index ETFs

Leveraged ETFs

Why Leveraged ETFs Are Wealth Destroyers

Leveraged Exchange Traded Funds (ETFs) such as FAZ, FAS, and SKF are designed to multiply the daily percentage change of the underlying index by factors of 2 or 3. They are thus toxic to your wealth and must not be held long-term, although they often mirror the short-term movements of their underlying assets.

Here is a simple explanation of why. Take the FAS, which is the 3X leveraged ETF of XLF, an unleveraged financial sector ETF. When XLF rises 1% in a day, the FAS is supposed to rise 3%. When things are going your way, therefore, everything is fine. But when the XLF drops, very bad things happen to FAS.

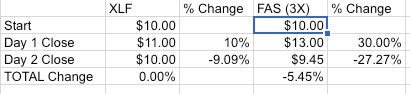

Have a look at this table:

On day 1, XLF rose 10% so FAS rose 30%. Great, you are e in the money.

But on day 2, XLF dropped back down to its starting price of $10.00, a decline of 9.09%. The bad news is that FAS declined 3X this amount or -27.27%. This takes its share price down to $9.45 instead of the $10 that you might otherwise expect.

So whereas XLF is unchanged after 2 days, FAS is down 5.45% after those same two days.

Why? The power of daily compounding instead of cumulative compounding. Leveraged ETFs are structured so that they compound on daily percent changes, not cumulative price changes. The second day declines of FAS should only be 23.08% to take it back to its original $10.00 per share price. But because it is 3X of XLF's daily change, instead it declines 27.27%.

Said another way, the leveraged ETFs operate on the daily percent change not on the price of the underlying index.

Clearly, this is definitely not a buy and hold investment! Not even for one overnight trade. Traders beware: set tight stop-losses!

Read More About Leveraged ETF Destruction.

On day 1, XLF rose 10% so FAS rose 30%. Great, you are e in the money.

But on day 2, XLF dropped back down to its starting price of $10.00, a decline of 9.09%. The bad news is that FAS declined 3X this amount or -27.27%. This takes its share price down to $9.45 instead of the $10 that you might otherwise expect.

So whereas XLF is unchanged after 2 days, FAS is down 5.45% after those same two days.

Why? The power of daily compounding instead of cumulative compounding. Leveraged ETFs are structured so that they compound on daily percent changes, not cumulative price changes. The second day declines of FAS should only be 23.08% to take it back to its original $10.00 per share price. But because it is 3X of XLF's daily change, instead it declines 27.27%.

Said another way, the leveraged ETFs operate on the daily percent change not on the price of the underlying index.

Clearly, this is definitely not a buy and hold investment! Not even for one overnight trade. Traders beware: set tight stop-losses!

Read More About Leveraged ETF Destruction.

On day 1, XLF rose 10% so FAS rose 30%. Great, you are e in the money.

But on day 2, XLF dropped back down to its starting price of $10.00, a decline of 9.09%. The bad news is that FAS declined 3X this amount or -27.27%. This takes its share price down to $9.45 instead of the $10 that you might otherwise expect.

So whereas XLF is unchanged after 2 days, FAS is down 5.45% after those same two days.

Why? The power of daily compounding instead of cumulative compounding. Leveraged ETFs are structured so that they compound on daily percent changes, not cumulative price changes. The second day declines of FAS should only be 23.08% to take it back to its original $10.00 per share price. But because it is 3X of XLF's daily change, instead it declines 27.27%.

Said another way, the leveraged ETFs operate on the daily percent change not on the price of the underlying index.

Clearly, this is definitely not a buy and hold investment! Not even for one overnight trade. Traders beware: set tight stop-losses!

Read More About Leveraged ETF Destruction.

Market News and Data brought to you by Benzinga APIs

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted In:

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in