A more favorable policy background and stable Yuan outlook have helped Macau Gaming stocks not to only re-rate, but also to outperform the market by 10 percent in what’s gone of 2016. However unlike the past couple of years, shares moved in very different directions. While Wynn Macau is up more than 46 percent year-to-date, Melco Crown Entertainment Ltd (ADR) MPEL has lost almost 16.5 percent.

Analysts at Goldman Sachs believe, “Sector valuation looks fair at close to mid-cycle now.” Nonetheless, they “still see beta and alpha generation opportunities.”

Having said this, the analysts recommended investors to behave selectively, keeping a close eye on sector trends and earnings revisions. The firm anticipates:

- 1) “Slow VIP GGR on regional competition, bad debt risk and closer scrutiny on junkets”

- 2) Faster growth in mass market, with novelty and cluster effects following a few more casino openings

- 3) Higher contribution of non-gaming to overall profit, driven by retail, although “oversupply could pressure rents at existing properties near term (i.e. Venetian).”

As per Goldman Sachs’ fiscal 2017 estimates, Wynn could post EBITDA 25 percent above consensus, while Galaxy and Sands China could miss by 6 percent. Despite the upgrades seen in recent weeks, the experts believe Wynn could deliver further upside, “as the market assumes Wynn Palace will only add 1-2% market share with a table yield 40% below the industry avg. a year later,” an estimate that Goldman analysts consider conservative, given the company’s track record.

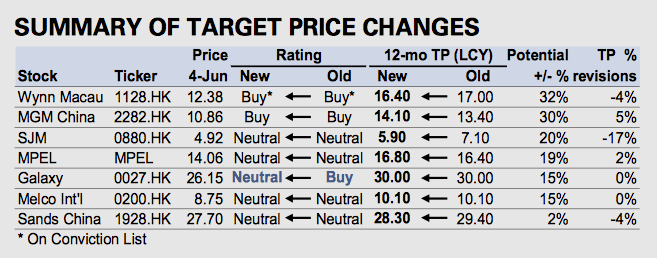

The firm revised its ratings and price target on Macau Gaming stocks as illustrated in the chart below:

Source: Goldman Sachs

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.