Stocks and bonds rallied Friday although maintained recent ranges after the April jobs report felt like the three bears’ third bowl of porridge—not too hot to raise interest rate fears, and not too cold to rekindle worries about the economic outlook.

Although Friday seemed to represent a seismic sentiment shift, action in the equities market could very well remain data-driven—meaning still vulnerable—because of the implications of strong or weak economic numbers for Federal Reserve interest rate policy. On that front, the economic calendar is back-loaded this week (see figure 2). It kicks off with a monthly retail sales report on Wednesday that’s likely to revive the Fed debate. This particular measure of retail spending, the economy’s major driver, has been spotty at best over recent months.

Will renewed hiring perk up spending? Friday headlines revealed that the U.S. economy added 223,000 jobs last month, a bounce from March and basically in line with industry economist expectations. Wage growth remained subdued, however. Buzz among Wall Street analysts suggested the report may have justified blaming March payrolls on the weather. The report all but took a June Fed interest rate hike off the table, but likely keeps a September move alive and well, the Street majority argues.

Keep Tabs on Market Interest Rates

Stocks and bonds don’t always move in lockstep, but neither had performed well in the days leading up to Friday’s employment-data release. Investors had watched anxiously as Treasury bonds suffered a series of losses, nosing benchmark 10-year yields—one way to watch the interest rate picture—to one-month highs of 2.2%.

Meanwhile, the broad-based S&P 500 (SPX) was down 1.3% for the week through Thursday and had trimmed its 2015 gain to a slim 30 points. In fact, the index had dropped 38 points from its fresh record high of 2,025 struck just a few weeks ago. But the jobs headlines proved to be ample fodder for the bulls, and the stampede sent the SPX rallying for a 28-point gain Friday.

When the dust settled, the SPX had erased any pre-employment report losses and finished the week with an 8-point gain. Let’s keep in mind that the SPX has been in a range from basically 2060 to 2120 since March 15 and in a tighter 2080 to 2120 since April 1. From that perspective, the broader stock market simply went from the low end of that recent range to the high end of the range in trade surrounding the jobs report. From a technical perspective, I don’t think much has changed. However from a psychological perspective, I think Friday’s number helped the bulls significantly.

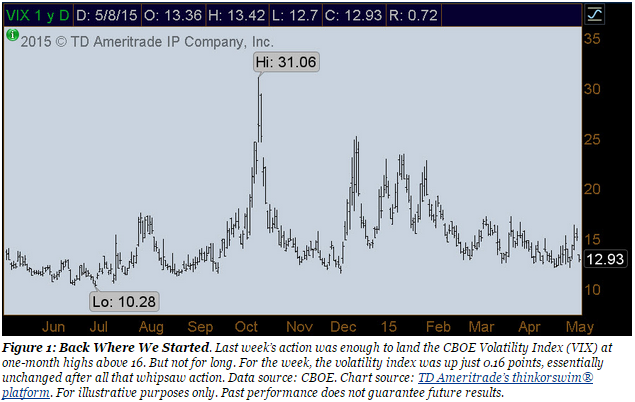

It was a roller coaster ride for the CBOE Volatility Index (VIX) as well. The index, affectionately known as the market’s “fear gauge,” finished Friday at 12.7 and at the lower end of its 2015 range (figure 1). The index hit a one-month high of 16.36 Wednesday and at the closing bell Thursday was at 15.35. That move proved fleeting once Friday’s relief rally sent the index tumbling 2.27 points, or 15%, to 12.86.

Retail Earnings Add to the Story

The pace of earnings is slowing, but this week’s list includes a few names from that closely watched retail sector. Gap GPS is out with same-store sales results on Monday, while JCPenney JCP and Macy’s M issue quarterly earnings figures on Wednesday.

Dow component Cisco CSCO reveals its earnings on Wednesday. The tech giant’s conference call can sometimes shed light on global tech-buying health, making this report a de facto economic indicator.

Fellow Dow component Boeing BA hosts an analyst day on Tuesday. That day includes the closely watched crop report from the Department of Agriculture, a release that can influence agricultural and commodities-based stocks. And because the U.S. does not operate in a vacuum, markets will be checking in on Wednesday’s releases for Eurozone GDP and China’s retail sales. China said Sunday it would cut benchmark interest rates for the third time in six months as it looks to help revive the economy.

Good trading,

JJ

TD Ameritrade, Inc., member FINRA/SIPC. Commentary provided for educational purposes only. Past performance of a security, strategy, or index is no guarantee of future results or investment success. Inclusion of specific security names in this commentary does not constitute a recommendation from TD Ameritrade to buy, sell, or hold.

Options involve risks and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before investing. Supporting documentation for any claims, comparison, statistics, or other technical data will be supplied upon request.

The information is not intended to be investment advice and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade. Clients must consider all relevant risk factors, including their own personal financial situations, before trading.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.