This article was originally published on Grit Capital and appears here with permission.

Ah, the American dream.

Then: Work hard, marry your high school sweetheart, buy a big house with a white picket fence, have a couple of kids, then fade into your golden years funded by your massive pension.

Now: Become an influencer, sell an options-trading course, YOLO your savings into a picture of an ape, have it actually hit, YOLO again into a shitcoin, lose all your money, rent a studio apartment the rest of your life because you’ll never afford a house at these prices, blame avocado toast.

It feels like a boatload of Deja Vu every time you boot up a local newspaper and hear about houses going for 20-30% over asking, set off by bidding wars.

But the tides are now changing. Listings that used to have 30+ bids now have 3 or 4, mortgage rates spiked in March, and there seems to be a much more real affordability issue.

What are the underlying factors at play, and where do we go from here?

This week, in <5 minutes, we’ll cover the housing market spike:

-

Overview 👉 What’s going on in the market?

-

The Impact of Interest Rates 👉 Higher rates = lower qualifying mortgage

-

The Supply Side 👉 Underbuilding in recent years tightening supply

-

Where does it go from here? 👉 Policy tools available to cool the market

Let’s get started!

1. Overview 👉 What’s going on in the market?

For the purpose of framing this discussion, I’m going to spend the majority of time on the housing market in my own backyard: Canada.

As bad as the headlines have been about the housing bubble in the US, it’s worse in Canada…much worse.

The friendly neighbours to the north have seen some of the most rapid climbs in housing values in the world.

I’ve been directly involved in the Toronto real estate market by owning condos, townhouses, multi-unit residential, and single-family detached. Every single time I buy a property, I say to myself, “damn, I overpaid” yet every time I’ve sold a property I say, “I can’t believe I got that much for it.”

Despite a more muted slowdown in 2008, since the turn of the millennium housing prices have had one helluva run. This is primarily fueled by lower interest rates (more on this below).

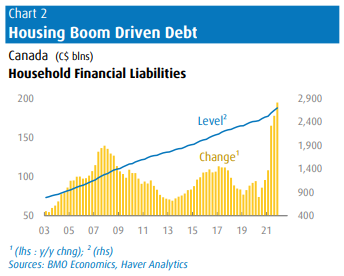

Many Canadians have binged heavily on debt, which has accelerated especially over the most recent quarters.

Debt doesn’t necessarily have to be a bad thing. When you can lever a purchase up, and instead deploy that capital into something like the stock market, as long as the return on your net capital exceeds the borrowing cost (assuming no change in the value of the underlying asset) it is the factually correct decision to make by a longshot.

The problem with this is the layer of assumptions you have to make. When you use leverage, your returns are magnified to both the upside and the downside. The blind assumption that a lot of Canadians are making is that housing prices can only go up.

And this has paid off for the average homeowner as they’re making cash hand over fist right now. But there becomes a point where enough is enough.

A good proxy for affordability is the level of household income vs the value of the home. Out of the G7 countries, Canada is by far the worst when it comes to this measurement:

2. The Impact of Interest Rates 👉 Higher rates = lower qualifying mortgage

Interest rates matter.

Policy rates and home prices have a strong inverse relationship, as lower rates lead to accelerating price gains and higher rates lead to lower housing prices.

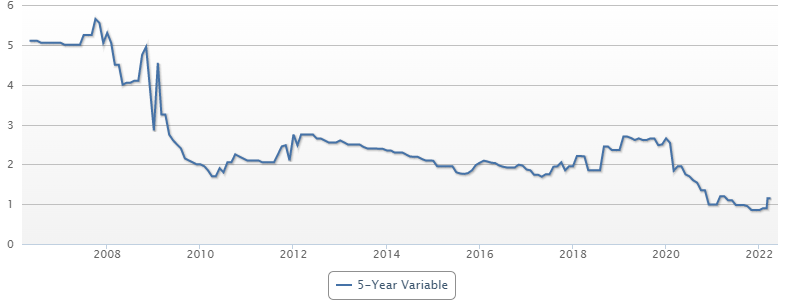

Below is a chart of the variable rate based on a 5-year mortgage in Canada since 2000

The most tangible impact of the mortgage rate during the purchasing decision is the effect that it has on the monthly payment, which affects the lender’s assessment of the ability to pay. Quite simply: the higher the interest rate, the higher the monthly payment.

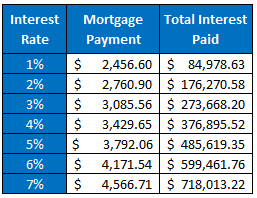

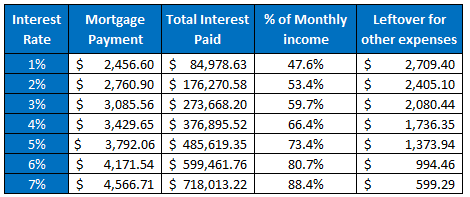

Let’s take the average Canadian house price of $815,000 (up 20% YoY), and assume the purchaser is putting 20% down, which leaves us with a mortgage of $652,000. Let’s also assume the pay frequency is monthly and the amortization period is 25 years with a 5-year term.

So let’s think about this for a second. The median after-tax income of Canadian households is around $62,000 or $5,166/month. A general rule of thumb is to keep your mortgage payment around 40% of your after-tax income.

Let’s also add a couple of columns to this chart like mortgage payment as a percentage of monthly income and the amount leftover. See how it stacks up

As you can see, the monthly mortgage payments are well out of the range of 40% even at 1% rates!! Using these assumptions, interest rates only need to move up 3% (from 1% to 4%) to cut in half the amount left over for all other expenditures in the average Canadian household.

Now, I understand that using both medians and averages doesn’t tell the whole picture because averages include outliers while medians do not. There are also obviously different dynamics between living in a popular city like Toronto or Vancouver (higher wage paying possibilities) and more rural areas (lower house prices, lower wages). But no matter how you parse the data, it doesn’t look good.

What the average Canadian is drastically underprepared for is a prolonged increase in interest rates. Remember, in the late 1970s/early 1980s, the 5-year fixed rate was around 16-20%. These events can and do happen. I’m not saying rates will get as high as that period, but they don’t need to in order to have a drastic impact on housing affordability.

Interest rate increases are a double whammy for existing homeowners. Not only do your monthly payments increase on a variable rate (or interest portion increase on a fixed rate), but fewer buyers start coming to the market which lowers the value of the home.

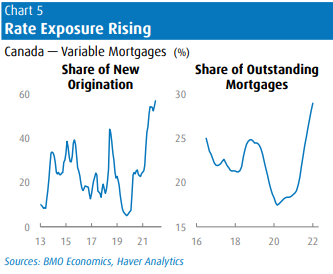

The variable rate component is particularly concerning due to these two charts:

Nearly 30% of outstanding mortgages are exposed to an increase in interest rates over the coming hiking cycle.

Look out below.

But first, let’s check in with our Outrageous Chartered FinMEME Analyst Dr. Patel!

3. The Supply Side 👉 Underbuilding in recent years tightening supply

As we all know, there are two components that set price: demand and supply. While demand for housing is mostly fueled by interest rates, speculation, and net immigration, supply is set by new builds (policy-influenced) and existing inventory going on the market (common used metric of “months of inventory”).

It’s important to look at the supply build-out in context relative to population growth:

The trend since 2008 has been down to a significant degree. Since Canada is well known for its pro-immigration policy, a lot of demand growth has come from this section. However, as we can see in this chart, new home completion is not keeping up with overall population growth.

In terms of existing supply, there is a commonly used metric called months of inventory. This is the number of months it would take to sell the current inventory, if no new homes were added to the market, at the current rate of sales activity.

We’re currently at an average of 1.6 months of inventory on a national basis in Canada. The long-term average for this number is around 5 months, while during the 2008 collapse it ballooned up to 12 months.

So the conclusion on the supply side is that we are still in an incredibly tight supply market, but we’ll see how this evolves as rates rise.

4. Where does it go from here? 👉 Policy tools available to cool the market

I think we are about to experience a real affordability issue in Canada as we go through this rate hiking cycle. There will be a lot of moving pieces to consider, but the most important is the longevity and velocity of rate hikes.

If higher for longer occurs, the housing market is in big trouble.

This is an issue that affects every single person in the country which also makes it a political hot topic and one of the favourites for local politicians to pander to ahead of elections.

The most important thing the government must do at this stage is to increase supply through these avenues:

-

Accelerating the delivery of land ready for development;

-

Shortening the approval process for building permits and re-zoning;

-

Improving the transparency and certainty about the steps involved in the approval process;

-

Ensuring development plans are time-limited to avoid construction delays;

-

Re-evaluating rent control policies to improve the supply of rental properties and give households more dwelling choices; and

-

Assessing incentives for developers to build more purpose-built rentals with a view to encouraging a more balanced mix of rental supply.

Wrapping Up…

With such a massive portion of overall total wealth that the average Canadian has locked up in their homes, this is the most important issue for the average Canadian consumer.

But what is the alternative to house ownership? Renting? No chance: renting is probably the single greatest wealth destroyer for anyone with sufficient funds to afford a downpayment.

Consider house ownership at this stage in the cycle more of a necessary evil rather than an investment. But there is a silver lining. For those that have entered the housing market and are looking to upgrade - a downmarket is what you want when upsizing.

Buckle up.

Until next time. Always Yours. Incessantly Chasing ROI,

-Genevieve Roch-Decter, CFA

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.