Stocks made new record highs, with the S&P 500 reaching a closing high of 4,894.16 on Thursday and an intraday high of 4,906.69 on Friday. For the week, the S&P rose 1.1% to close at 4,890.97. The index is now up 2.5% year to date and up 36.7% from its October 12, 2022 closing low of 3,577.03.

One of the hottest debates in the markets right now is if and when the Federal Reserve will pivot from its very hawkish stance and start cutting interest rates.

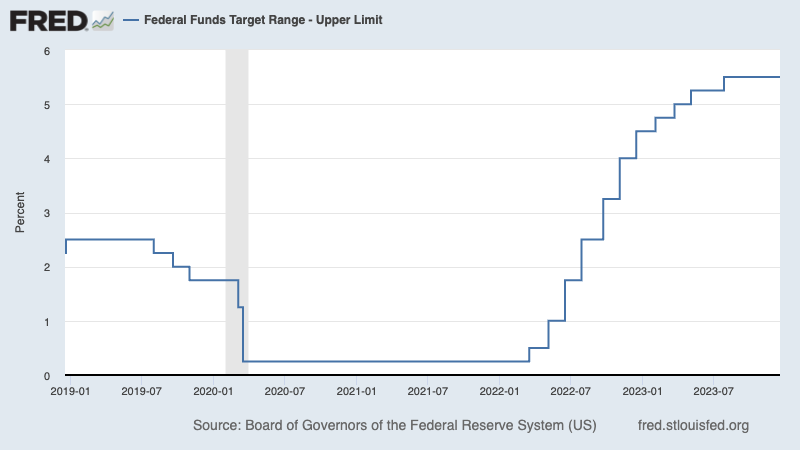

If you’re a little behind: The Fed began hiking rates aggressively in early 2022 in its effort to get inflation under control. It’s been on hold since last summer. And in its December summary of projections, the central bank signaled that it could cut rates three times in 2024. The present question for Fed watchers has been about when that first rate cut will happen.

The Fed spent much of the past two years hiking rates. Are rate cuts near? (Source: FRED via TKer)

For a while, futures traders were betting that the first rate cut would come with the monetary policy meeting this coming March. But more recently, those bets have been pared back with traders now assigning a 47% chance of a March rate cut, down from 83% a month ago.

A popular view is that rate cuts would be bullish for risk assets like stocks. So any developments that lower the odds of a rate cut in the near term would therefore be bearish. All other things being equal, this view makes sense.

But the world is complicated, and all other things are never equal.

The World Has Changed Since Fed Rate Decisions Were A Much Bigger Deal

I’m no monetary policy economist. But as I discussed on the Investopedia Express podcast earlier this month, I think concerns about the Fed’s next move on interest rates are a bit overblown.

First of all, we’re talking about a potential 25-basis-point cut from a range of 5.25% to 5.5%. Sure, that’s not insignificant. But that’s nowhere near as big a deal as it was when we were talking about 25-, 50-, and 75-basis-point rate hikes from near 0%.

Upgrade to paid

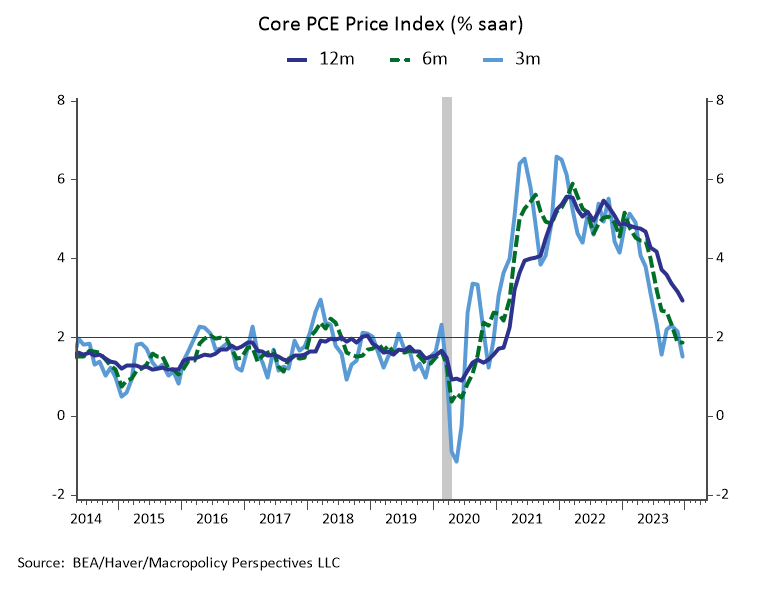

Second, all those big rate hikes early in the hike cycle were happening amid an intensifying inflation crisis. The economy was a complicated mess in 2022. Today, that crisis is largely behind us with inflation rates hovering near the Fed’s target levels. On Friday, we learned that the core PCE price index, the Fed’s preferred inflation gauge, fell to its lowest level in nearly three years.

In other words, the stakes for the upcoming Fed policy meetings aren’t nearly as high as they were in 2022 and 2023.

The Fed’s preferred measure of inflation has cooled significantly. (Source: @JC_Econ)

Third, we have to keep in mind that rate cuts and rate hikes — in and of themselves — aren’t the real issue. Rather, they represent reactions to real issues.

Putting it another way, whether or not the Fed cuts rates is not the right question. Here’s an excerpt of what I said to Investopedia’s Caleb Silver earlier this month:

… As far as whether or not they actually pivot and begin to cut or hold or whatever, I think that's really not the right question. The question [should] be, “If they don't cut, then why are they not cutting as they suggested in their dot plots?” Right? Is it possible that the economy heats up more than they initially modeled? Yeah, maybe that's a good reason to not cut because they're concerned that inflation is going to be bubbling up again.

From an investor perspective and from an economic perspective, that's not exactly the worst thing in the world that the economy isn't falling apart. Because remember, a lot of these assumptions when it comes to the Fed pivot, in addition to inflation cooling, are also tied to the idea that the economy is also cooling — that growth is slowing and decelerating and that a lot of people have recessions on their mind. So maybe the Fed doesn't pivot because the economy's picking up? That's really not that big a deal.

To reiterate, the Fed’s projection that it would cut rates in 2024 was accompanied by assumptions that economic growth would slow significantly and inflation rates would take another leg lower during the year.

That’s to say if the Fed were to change its outlook for rate cuts, it may also be the case that its outlook for the economy and inflation have changed as well.

Economic Reality Is Proving Stronger Than Expected

The recent reduction in March rate-cut odds followed better-than-expected monthly reports on retail sales, industrial production, housing construction, and consumer sentiment. For more, read last week’s review of the macro cross currents.

On Thursday, we learned GDP grew at a 3.3% rate in Q4, which was much stronger than the 2.0% rate expected.

GDP grew at a 3.3% rate in Q4. FRED

Also on Thursday, we learned orders for nondefense capital goods excluding aircraft — a.k.a. core capex or business investment — rose 0.3% to a record $74.33 billion in December.

Business investment activity remains strong. FRED

Core capex orders are a leading indicator, meaning they foretell economic activity. While the growth rate has leveled off a bit, they continue to signal economic strength in the months to come.

On Friday, we learned personal consumption expenditures — which represents about 69% of GDP — increased 0.7% month over month in December to a record annual rate of $19.0 trillion.

FRED

The confluence of data we’ve gotten over the past several weeks suggest economic activity is tracking stronger than many expected.

Of course, the worry is that hot economic activity could fan the flames of inflation again, which would explain why those rate hike odds are coming down — traders are betting that the Fed will keep monetary policy tighter for longer to rein in the economy to contain inflation risks.

But on balance, all this is not necessarily a bad thing.

Remember, all of 2023 was about an economy performing better than expected, avoiding a recession many expected. Meanwhile, inflation cooled amid tight monetary policy.

Importantly, the stock market rallied for much of the year, with the S&P 500 surging 24%.

The Bottom Line

I think we’ll probably continue to hear pundits warn that rate-cut odds are coming down and argue this is bearish for stocks.

But before buying into that argument, we have to understand the economic circumstances that would cause the Fed to put off rate cuts.

If it’s because the economy is proving to be stronger than expected, then it’s no sure thing that keeping monetary policy tight is necessarily bad news — as we learned all of last year. By the way, it is the case that the economy has been proving stronger than expected as inflation rates continue to cool. And even as the odds of a rate cut have declined, the S&P 500 has been hitting fresh record highs.

And amid all this, the debate is over a relatively small move in the Fed’s benchmark interest rate. That is to say maybe the Fed's next move just isn't that big of a deal.

As always, context matters — especially when we’re thinking about developments that appear bullish or bearish for stocks.

One More Quick Thought

While we’re on the subject, we should also consider the possible scenario the Fed begins cutting rates because the economy takes a significant turn for the worse. As Carson Group’s Ryan Detrick observed, rate cuts that were intended to stimulate the economy amid a recession came with the S&P 500 falling an average of 11.6% in the year that followed.

This is a scenario where the rising odds of a rate cut is not necessarily a bullish signal. Another reminder that context matters.

A version of this post was originally published on Tker.co.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.