Offering unbiased reviews and tailored advice to ensure you're not being taken advantage of.

Most people consider life insurance as an investment for their family's financial future. But the truth is that life insurance only works when it clearly meets the goals you have for your financial future.

Many consumers are left under-protected without even knowing it. LifeInsuranceReview.com (LIR), a consumer-focused life insurance review service since 2011, led by attorney James Burns and life insurance analyst expert John Nguyen, aims to change this dynamic by empowering individuals to protect themselves from being shortchanged.

The Front-End Problem: Pressure to Buy, But Not the Best Buy For You

The life insurance sales industry uses a strong sales approach, which often leaves consumers feeling pressured into purchasing policies they may not fully understand. Yes, protecting your family is important, but are you being shown the correct or all the life insurance options for your needs at the best cost?

"Most people are not experts on life insurance. They turn to a salesperson who represents a company and offers them coverage that might sound great. But they have no idea if the salesperson is incentivized to sell them a certain product, instead of the one that meets their goals and needs the best," says Nguyen.

Many buyers walk away from meetings with agents or brokers confident they've made a sound decision, only to later realize that they could have secured a better policy for the same cost—or even less.

"You're thinking, ‘I finally have life insurance!' but you don't realize, ‘I could've gotten 30-50% more coverage and with better benefits,'" Burns adds.

This discrepancy isn't always due to malicious intent on the part of agents or brokers, but rather an industry focus on closing sales without considering whether the policy truly meets the consumer's long-term needs. Agents and brokers often believe that as long as they are able to sell life insurance protection, it's good enough.

Burns explains that the life insurance industry is structured in a way that incentivizes agents and brokers to prioritize new sales over serving existing clients.

He says, "Agents and brokers sell policies that might not be the best fit. They are often just commissioned sales people, not insurance experts."

The Back-End Problem: Lack of Follow-Up

The challenges don't end once a policy is purchased. Many consumers find that after the initial sale, their relationship with their agent becomes distant, with little to no follow-up to ensure that their coverage still aligns with their needs.

Nguyen reminds: "Advisors don't really do reviews because they are structured to be compensated on the front end of a policy sale, rather than servicing the policy."

This leaves consumers in a precarious position. Without regular reviews, policyholders might not realize when their coverage is no longer adequate—or worse when they are paying too much for a policy that underperforms.

One common scenario that Nguyen has seen involves clients who continue to pay into policies for years without realizing they could have secured better returns or higher death benefits elsewhere.

"The consumer is ‘sold' on the front end, and nobody's helping them review what they were sold on the back end to make sure that it's performing like it was originally sold to them," Nguyen says.

The lack of a proactive review process results in missed opportunities for policyholders to adjust or optimize their coverage as their financial situation or goals change.

LifeInsuranceReview.com: The Consumer Advocate

Burns and Nguyen led LifeInsuranceReview.com as an advocate for consumers. LIR is run entirely by fiduciaries who operate with the consumer's best interests in mind. They offer unbiased reviews and advice to ensure that policyholders are getting the most out of their coverage.

"Life Insurance Review exists as that valued second opinion, being on the consumer's side," Burns explains. "If your current policy doesn't meet your needs, we will research other options."

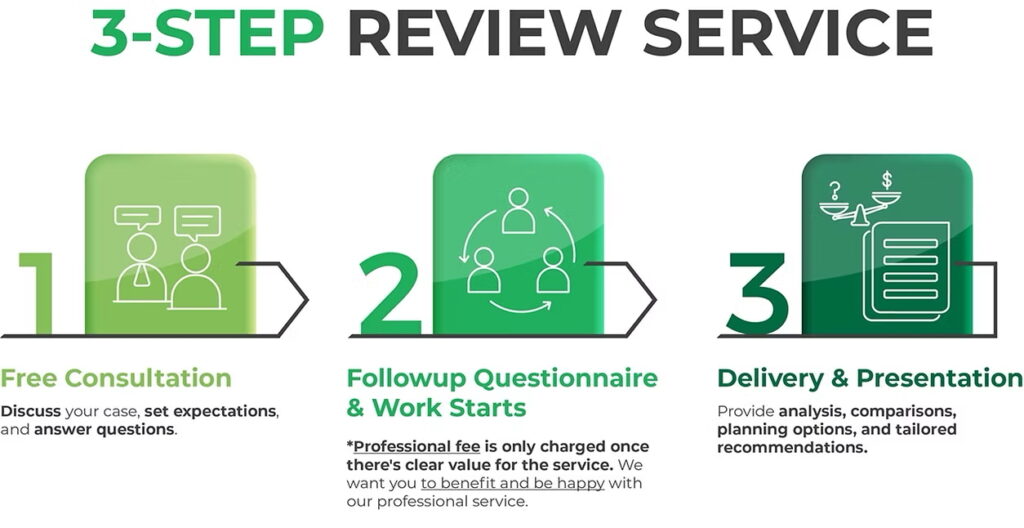

The company offers a comprehensive 25-point assessment of existing life insurance policies, helping clients identify gaps in coverage, overcharges, or better alternatives.

"Our mission is simple: empower the consumer to explore, compare, and verify for themselves," Nguyen says.

LIR is a resource for consumers to safeguard their financial future and avoid being locked into policies that don’t best serve their needs.

Why Regular Policy Reviews Matter

LifeInsuranceReview.com encourages regular policy reviews—something that many traditional agents and brokers overlook. Burns stresses the importance of revisiting life insurance policies every few years.

"Even in just a few years, your situation and financial goals can change drastically. We can also solve that problem for people so that they can understand the options that exist," he shares.

Nguyen says life insurance is not a "set it and forget it" product. As consumers' financial goals and life circumstances evolve, so too should their life insurance policies. For instance, a term life policy purchased in a consumer's 30s may no longer be appropriate as they near retirement age. Similarly, changes in the life insurance market could mean that more competitive or flexible policies have become available, providing better coverage and benefit protections at a lower cost.

Protecting Yourself from Being Shortchanged

Nguyen and Burns both emphasize that consumers need to be vigilant when it comes to life insurance—both when buying a new policy and managing existing ones. LIR's services ensure that consumers are not often left navigating the complexities of life insurance on their own, vulnerable to being sold suboptimal products.

"We are a team of life insurance experts like none other. But more importantly, we are fiduciaries," Nguyen says. "Consumers finally have a resource to turn to that's truly on their side, someone who will represent their best interests."

For Burns and Nguyen, the ultimate goal is to help consumers avoid being shortchanged on both the front and back ends of their life insurance experience. By providing expert reviews, educational resources, and a commitment to transparency, LifeInsuranceReview.com is a leader in providing unbiased reviews for consumers.

As Burns succinctly puts it: "Be empowered, don't be sold."

With LifeInsuranceReview.com, consumers finally have a tool and resource to protect themselves from the pitfalls of the life insurance sales industry—ensuring that their financial future is secure without the worry of being taken advantage of.

Whether you’re buying life insurance for the first time or reevaluating an existing policy, it pays to take the time to explore your options. Visit LifeInsuranceReview.com today to see how you can improve your life insurance strategy and ensure you’re getting the best value.

This post was authored by an external contributor and does not represent Benzinga's opinions and has not been edited for content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.