Supergiants like Exxon are focused on big offshore venues like Guyana and Namibia, leaving behind prime onshore natural gas assets in Europe – a region that is now desperate for affordable domestic resources that aren't controlled by Russian Gazprom.

Prior to Russia's invasion of Ukraine, Gazprom was calling the energy shots in Germany.

Those days are over.

But Germany, the European Union's biggest economy, still needs natural gas, even if this winter's storage is nearly full. It's not full as a result of domestic sources. Germany has traded one form of dependence for another. The filling up of winter storage has come at a high price tag thanks to expensive LNG imports, which are now at risk, as well, due to the Biden administration's pause on new LNG export projects. At the height of the crisis, the European Union was paying some 40% more for U.S. LNG imports than it was for Russian piped gas.

While Germany is busy building grandiose, high-dollar LNG receiving terminals, there is a far cheaper domestic alternative, and it's found in assets abandoned by the supergiants who are off chasing bigger oil and gas dreams offshore.

What's too small for Exxon and others, could be of huge potential value to smaller industry players.

That's what MCF Energy MCF MCFNF is focusing on. OilPrice.com believes this is the first new public company providing investors with exposure to European natural gas since Russia invaded Ukraine.

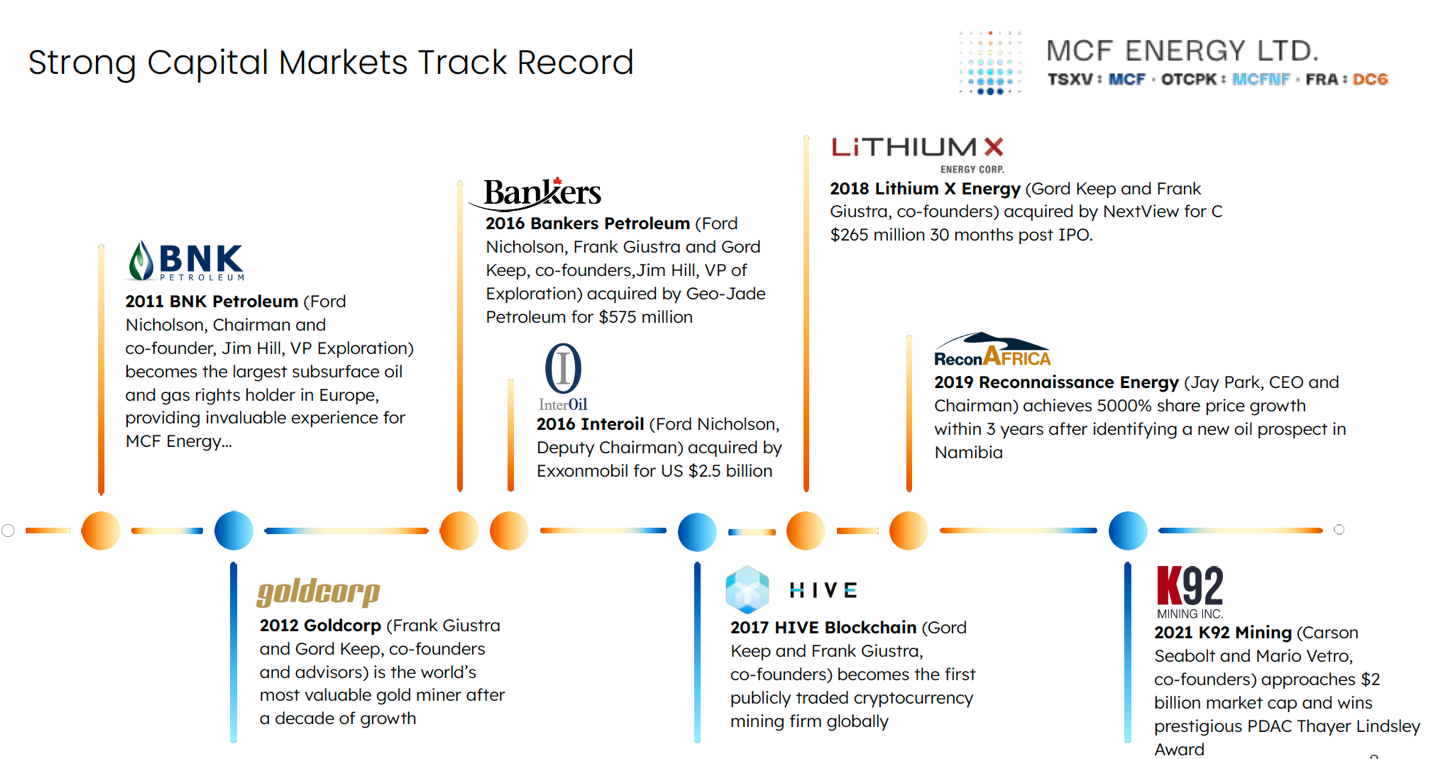

The big names behind MCF Energy have a clear track record in developing energy assets for top-dollar exits, and they see the timing as the most propitious yet.

The Top People in the Industry for Europe's Energy Reset

The company is no stranger to Europe's energy industry.

It was co-founded by oil and gas investor Ford Nicholson who has a track record of developing billion-dollar international assets and offloading them for top dollar to giants such as Exxon. In total, Ford has exited around $4.5 billion in energy assets in Europe and Asia.

In the 1990s, after the fall of the Soviet Union, Nicholson launched an energy company in Kazakhstan that was sold in 2006 for approximately $1.6 billion. In 2004, he co-founded a company that developed Europe's largest heavy oilfield, in Albania (Bankers Petroleum Albania, Ltd) worth about $2.25 billion by 2011.

The story here is one that MCF Energy could be aiming to repeat in today's Europe, which is in the middle of an energy reset worth trillions of dollars–and the biggest near-term prize is natural gas.

With its world-class team, Bankers Petroleum saw production grow by over 2,000% between inception in 2004 and 2015. Only 13 months after launch, its enterprise value increased by over 1,000% before being acquired by Geo-Jade Petroleum in 2016. But the story didn't end there. BNK Petroleum was spun out of Bankers Petroleum in 2008 to explore for shale gas in Europe and developing gas assets in the United States. Between 2009 and 2011, BNK saw a market valuation increase of over 4,000% and became one of the largest holders of oil and gas rights in Europe.

In 2017, as Deputy Chairman, Nicholson sold another oil and gas company, InterOil, to Exxon for approximately $2.6 billion.

Now he's back with MCF Energy MCF OTC: MCFNF), which has rapidly acquired a portfolio of attractive natural gas projects in Germany and Austria. They have just started drilling in one of their most prospective areas.

Ford is backed by an impressive executive team and board, which includes former NATO Supreme Allied Commander of Europe, General Wesley Clark, who is committed to helping ensure Europe's energy security and independence from Russian oil and gas.

MCF's CEO is James Hill, the geologist behind BNK Petroleum which delivered major wins for early investors. The executive chairman is Jay Park, a renowned international energy lawyer based in London and Istanbul. Park is also the former Chairman of Reconnaissance Energy Africa, which is exploring one of the biggest emerging oil plays in the world, in the African frontier of Namibia.

Finally, director Richard Wadsworth, also a former Bankers Petroleum figure, is a 30-year petroleum engineer veteran who most recently led and developed a 55,000 bopd oilfield in Iraq that has a development plan for 230,000 bopd.

Key Assets Where Europe Needs It Most

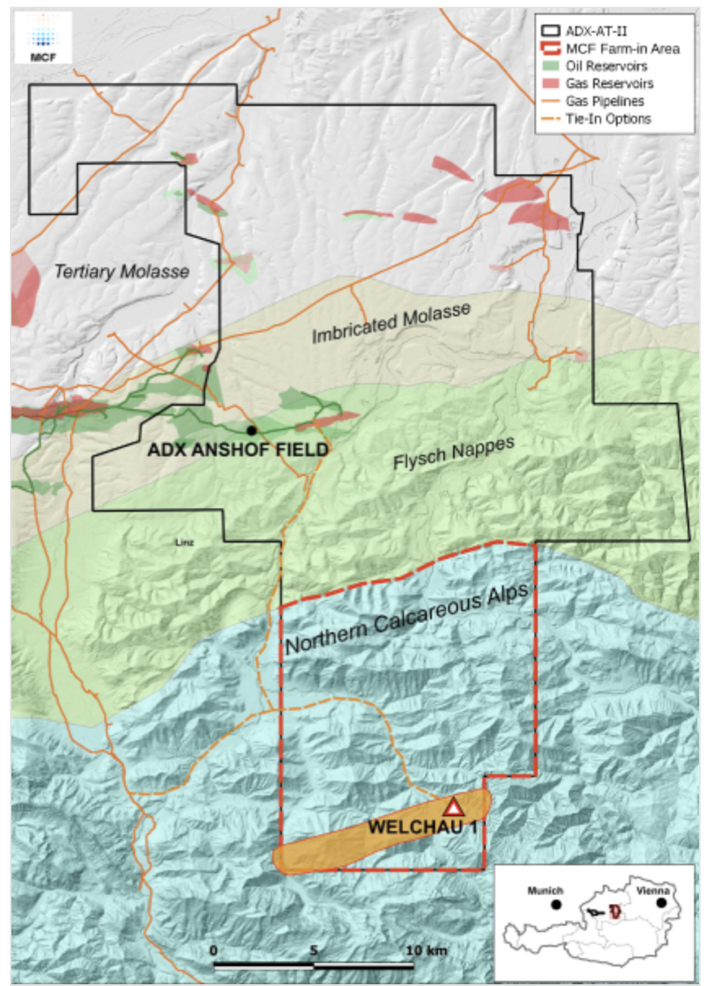

The first drill, that will launch next week, is in Austria, at MCF Energy's Welchau prospect near the Austrian Alps. This prospect is analogous to large anticline structures discovered in the Kurdistan Region of Iraq and the Italian Apennines.

Welchau is adjacent to an up-dip from a discovery that intersected at a gas column of at least 400 meters, testing condensate rich for pipeline quality gas. A national gas pipeline network is only 18 kilometers away, making for a short, cheap tie-in option for getting product to domestic markets.

MCF will earn a 25% interest for exploration drill costs estimated and capped at 2.55 million euros.

In Germany, MCF Energy MCF MCFNF has licenses secured for six large-scale project areas in the country's northern and southern regions, with the Company stating that drill testing set to launch immediately after the Austrian drill is aimed to be completed.

These key projects are the result of MCF Energy's strategic 100% acquisition of Germany's Genexco GmbH. Genexco was established in 2014 by some of Europe’s largest energy producer insiders. It carefully assembled a portfolio of exploration and developments assets when few others were paying attention.

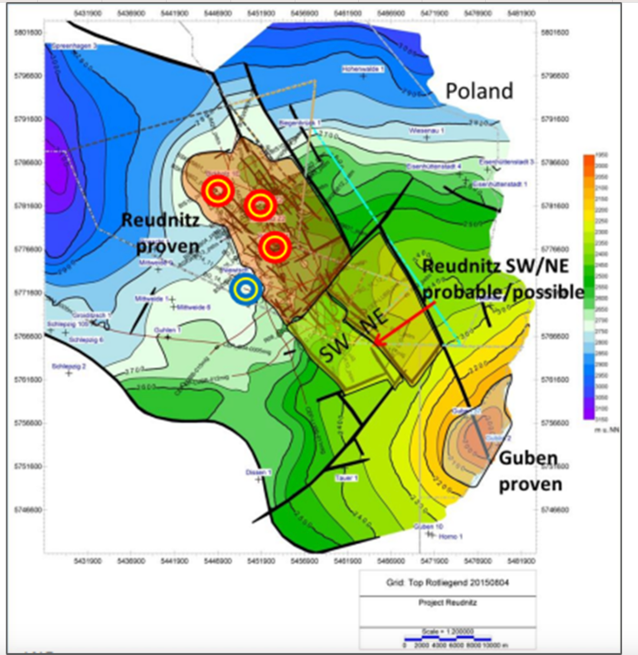

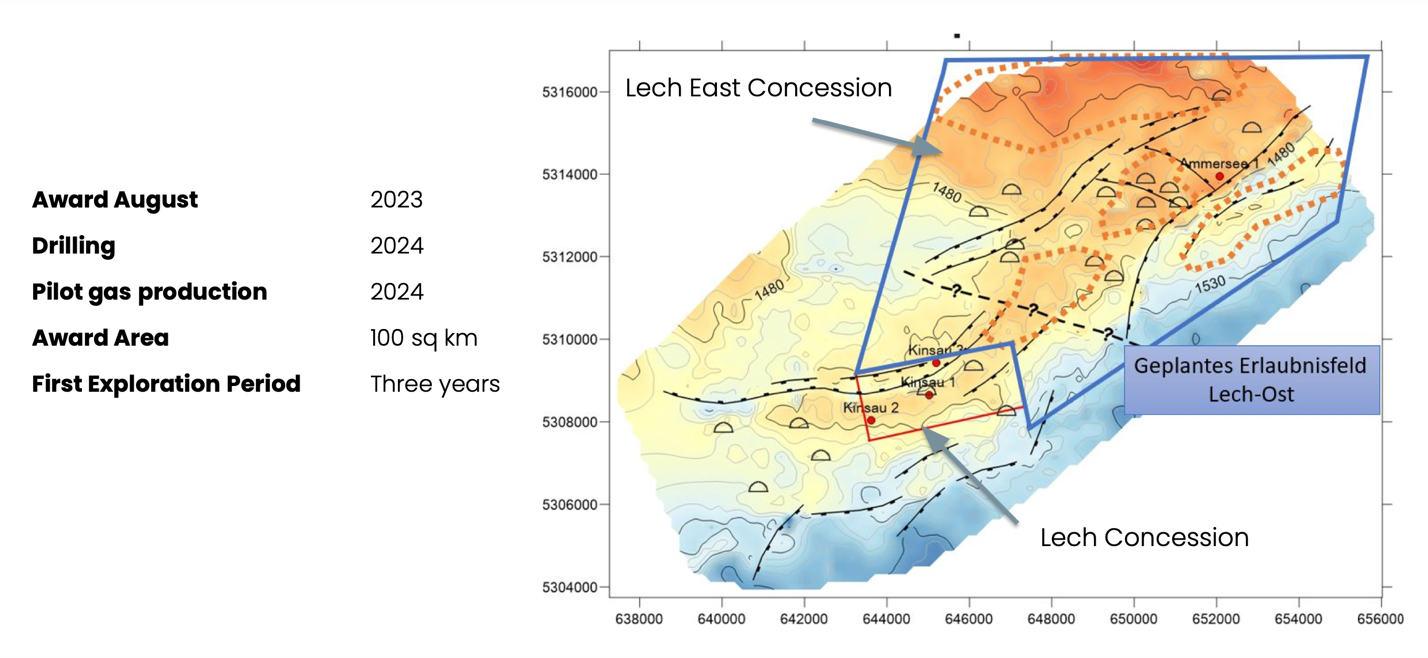

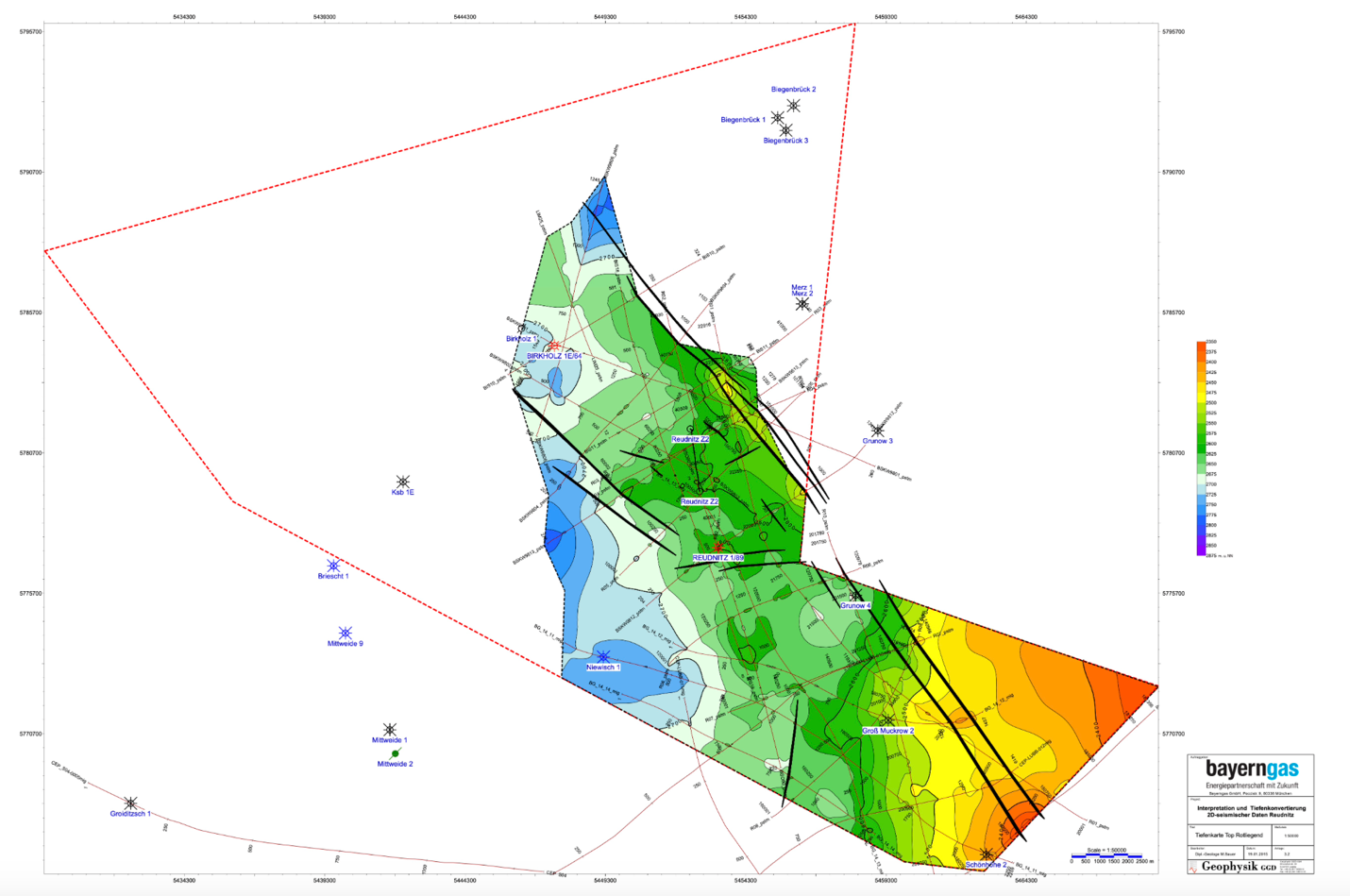

The Genexco acquisition gave MCF Energy four key assets that include previously drilled wells and two discoveries. MCF got its hands on Reudnitz, a proven, large-scale natural gas development that also contains an oil exploration target. They also acquired the Lech concession, a 10-square-kilometer play with three previously drilled wells and two discoveries; Lech East, which directly offsets the discoveries on the Lech block is much larger, around 100 square kilometers; and the Erlenwiese concession in the Rhein Graben which covers about 80 square kilometers.

Reudnitz, some 70 km southeast of Berlin, was initially discovered in 1964 with multi-zone hydrocarbon potential and proven phases of Helium (~0.2%), methane (14-20%) and like most fields in northern Germany high nitrogen content (>80%).

According to the company, pilot test production will start this year. After testing development is planned using cryogenic technology for helium and nitrogen sequestration. The Company announced an independent assessment best estimate (P50) at 118.7 billion cubic feet (BCF) of methane, 1.06 BCF of helium and 4.4 million barrels of oil.

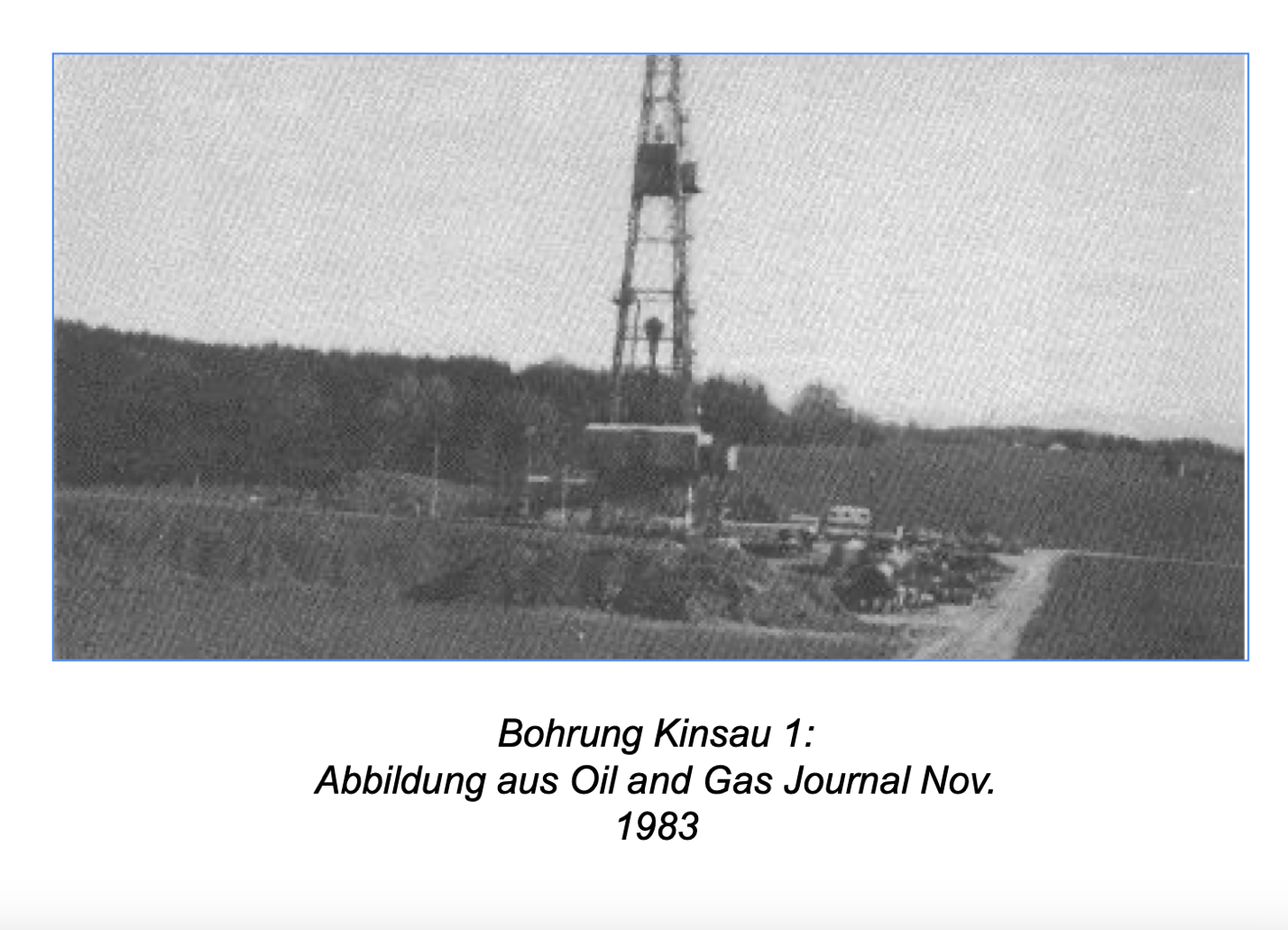

But the next drill, right after Austria, currently scheduled in March, will be MCF Energy's Bavarian concession, Lech, where they will re-enter the Kinsau #1 well. Back in 1983, this same well tested at a maximum flow rate of 24 MMCFD. MCF's 20% interest in this concession (through its Genexco acquisition) means it won't be paying for the cost of drilling, which the Company estimates to be up to 5 million euros.

The Kinsau #1 well, originally drilled by Mobil in the ‘80s, encountered a primary gas reservoir with associated condensate.

In a recent interview with Oilprice.com, James Hill said Mobil (now Exxon) abandoned the well because "back then, it probably wasn't economic".

Gas wasn't worth anything, so they drilled another well to a deeper target and got about 180 barrels of oil a day out it. This was followed by a third well which hit the oil/water contact. They didn't pursue it much further at the time because oil prices were at the bottom of the barrel. But for some reason, they shot 3D after they drilled these three wells, which we have then inherited the information from," Hill said.

MCF has spent a significant amount of time analyzing the cores from these wells, and Hill isn't just eyeing recoverable gas with associated condensates; he's also eyeing an oil zone, noting that in the ‘80s, using only a vertical well, as the technology of the day afforded, this well-produced almost 200 bpd. MCF is studying going back in and recreating this with a horizontal well to stimulate a zone that they know contains hydrocarbons already.

The infrastructure is already in place, as well. There is a pipeline connection less than two kilometers away, and a local pipeline company that potentially will connect up at zero cost in return for dedicated gas for the pipeline.

Right next door, in southwest Bavaria, lies Lech East, a vast 100-square-kilometer expanse solely under the ownership of MCF Energy. The company is now preparing for an ambitious 4.6-million-euro exploration program.

For the Lech concessions, MCF has 120 square kilometers of 3D and it's identified using the latest AI, machine learning analysis and multiple firm locations. If they hit, they are potentially looking at multiple development locations from each of these.

At MCF's Erlenwiese concession, 2D seismic has been acquired and is being reprocessed, with 3D on the way, along with AI analysis.

Beyond this, MCF Energy's Genexco acquisition gives it a proprietary database for 10 additional project areas, including geological, seismic, and well data, which is being used as the basis of further acquisitions.

Is This Western Europe's Last Chance at Domestic Natural Gas?

Right now, Western Europe is importing expensive gas from all over the world. It's even gone back to dirty coal in its quest to shed Russia's weaponized energy.

Europe requires a safe, domestic source of energy, and since we are in the midst of an energy transition, it will have to be cleaner than coal. Natural gas is the obvious bridge fuel. Renewables alone are up to capacity, which Europe learned when Russia invaded Ukraine and Western sanctions sent the continent's energy supply into a state of crisis.

The fallout from that crisis had cost the European Union an estimated $1 trillion as of December 2022, according to Bloomberg.

The only medium-term answer for Europe is domestic natural gas, with the gaps filled in with LNG.

Europe's under-investment in natural gas has been laid bare, and now we are in the middle of a historical energy reset, with trillions of dollars up for grabs. Natural gas is being reclassified as green and sustainable, which is a boon for the development of MCF Energy's assets.

LNG imports at huge volumes are not sustainable, and once China's post-COVID economic recovery is complete, Europe will find itself priced out.

MCF Energy already has a large portfolio of high-quality gas projects in Europe, with significant prospects in Austria and Germany at various stages of testing and development. And their world-class team has a long-running track record of billion-dollar exit transactions.

With drilling planned in multiple projects this year and next, and Europe desperate for domestic natural gas, MCF MCF MCFNF is expecting to gain a fair amount of attention. "Once the hydrocarbons start lighting up all over the 3D seismic in Germany, in the middle of winter, it's going to get people's attention in a big way," says Hill.

Image sourced from Shutterstock

This post was authored by an external contributor and does not represent Benzinga’s opinions and has not been edited for content. This contains sponsored content and is for informational purposes only and not intended to be investing advice.

**IMPORTANT! BY READING THE ABOVE CONTENT YOU EXPLICITLY AGREE TO THE FOLLOWING. PLEASE READ CAREFULLY**

Forward-Looking Statements

This publication contains forward-looking information which is subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ from those projected in the forward-looking statements. Forward looking statements in this publication include that large oil and gas companies will continue to focus on offshore natural gas resources; that domestic onshore natural gas assets in Europe will provide a more affordable energy source than offshore resources; that demand for natural gas will continue to increase in Europe and Germany; that Russia will not supply the majority of natural gas in Germany and Europe; that natural gas will continue to be utilized as a main energy source in Germany and other European countries and demand for natural gas, and in particular domestic natural gas, will continue and increase in the future; that MCF Energy Ltd. (the "Company") can replicate the previous success of its key investors and management in developing and selling valuable energy assets; that the natural gas projects of the Company will be successfully tested and developed; that the Company can develop and supply a safe, domestic source of energy to European countries; that natural gas will be reclassified as sustainable energy which will support the development of the Company's assets; that imports of liquified natural gas will not be sustainable for Europe and that European countries will need to rely on domestic sources of natural gas; that the Company expects to obtain significant attention due to its upcoming drilling plans combined with Europe desperate for domestic natural gas supply; that the upcoming drilling on the Company's projects will be successful; that the Company's projects will contain commercial amounts of natural gas; that the Company can finance ongoing operations and development; that the Company can achieve its business plans and objectives as anticipated. These forward-looking statements are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information. Risks that could change or prevent these statements from coming to fruition include that large oil and gas companies will start focusing on the development of domestic natural gas resources; that the natural gas resources of competitors will be more successful or obtain a greater share of market supply; that offshore liquified natural gas assets will be favored over domestic resources for various reasons; that alternative technologies will replace natural gas as a mainstream energy source in Europe and elsewhere; that demand for natural gas will not continue to increase as expected for various reasons, including climate change and emerging technologies; that political changes will result in Russia or other countries providing natural gas supplies in future; that the Company may fail to replicate the previous success of its key investors and management in developing and selling valuable energy assets; that the natural gas projects of the Company may fail to be successfully tested and developed; that the Company's projects may not contain commercial amounts of natural gas; that the Company may be unable to develop and supply a safe, domestic source of energy to European countries; that natural gas may not be reclassified as sustainable energy or may be replaced by other energy sources; that the upcoming drilling on the Company's projects may be unsuccessful or may be less positive than expected; that the Company's projects may not contain commercial amounts of natural gas; that the Company may be unable to finance its ongoing operations and development; that the Company can achieve its business plans and objectives as anticipated; that the Company may be unable to finance its ongoing operations and development; that the business of the Company may be unsuccessful for various reasons. The forward-looking information contained herein is given as of the date hereof and we assume no responsibility to update or revise such information to reflect new events or circumstances, except as required by law.

DISCLAIMERS

This communication is for entertainment purposes only. Never invest purely based on OilPrice.com's communication. Oilprice.com has not been compensated by MCF Energy Ltd. for this article but may in the future be compensated to conduct investor awareness advertising and marketing for MCF Energy Ltd. While the opinions expressed in this article are based on information believed to be accurate and reliable, such information in OilPrice.com's communications and on its website has not been independently verified and is not guaranteed to be correct. The content of this article is based solely on OilPrice.com's opinions which are based on very limited analysis and are not professional analysts or advisors.

SHARE OWNERSHIP. The owner of Oilprice.com owns shares of MCF Energy Ltd. and therefore has an incentive to see the featured company's stock perform well. The owner of Oilprice.com will not notify the market when it decides to buy more or sell shares of MCF Energy Ltd. in the market. The owner of Oilprice.com will be buying and selling shares of this issuer for its own profit. Accordingly, Oilprice.com's views and opinions in this article are subject to bias, and why you should conduct your own extensive due diligence regarding the Company as well as seek the advice of your professional financial advisor or a registered broker-dealer before you consider investing in any securities of the Company or otherwise.

NOT AN INVESTMENT ADVISOR. Oilprice.com is not registered or licensed by any governing body in any jurisdiction to give investing advice or provide investment recommendations. You should not treat any opinion expressed herein as an inducement to make a particular investment or to follow a particular strategy, but only as an expression of opinion. The opinions expressed herein do not take into account the suitability of any investment with your particular objectives or risk tolerance. Investments or strategies mentioned in this article and on OilPrice.com's website may not be suitable for you and are not intended as recommendations.

ALWAYS DO YOUR OWN RESEARCH and consult with a licensed investment professional before making any investment. This communication should not be used as a basis for making any investment in any securities. Past performance is not indicative of future results.

RISK OF INVESTING. Investing is inherently risky. Do not trade with money you cannot afford to lose. There is a real risk of loss (including total loss of investment) in following any strategy or investment discussed in this article or on OilPrice.com's website. This is neither an offer to purchase, nor a solicitation of an offer to sell, subscribe for or buy any securities or the solicitation of any vote in any jurisdiction. No representation is being made as to the future price of securities mentioned herein, or that any stock acquisition will or is likely to achieve profits.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.