Buying a home is a significant milestone, yet myths and misinformation often shroud the mortgage process. This blog aims to dispel the top 15 mortgage myths that borrowers frequently hear, especially first-time homebuyers. We’ll differentiate fact from fiction using data, examples, and credible sources to ensure you're well-informed as you navigate your home loan journey.

Before diving into some of the popular myths out there, we'll use two hypothetical scenarios to demonstrate why distilling fact from fiction is important. Not understanding those distinctions may have real-life impact on your financial future!

Why is Understanding Fact from Fiction Important?

Understanding fact from fiction in the mortgage process is crucial because it directly impacts your financial decisions and overall homeownership experience. Misconceptions can lead to missed opportunities, higher costs, and unnecessary stress. On the other hand, being well-informed enables you to make strategic choices that save money, optimize benefits, and secure better terms.

HYPOTHETICAL EXAMPLE#1: UNDERSTANDING A FACT VS. BELIEVING A MYTH

Let’s compare two hypothetical first-time homebuyers: Sarah and John.

Sarah: Believing the Myth

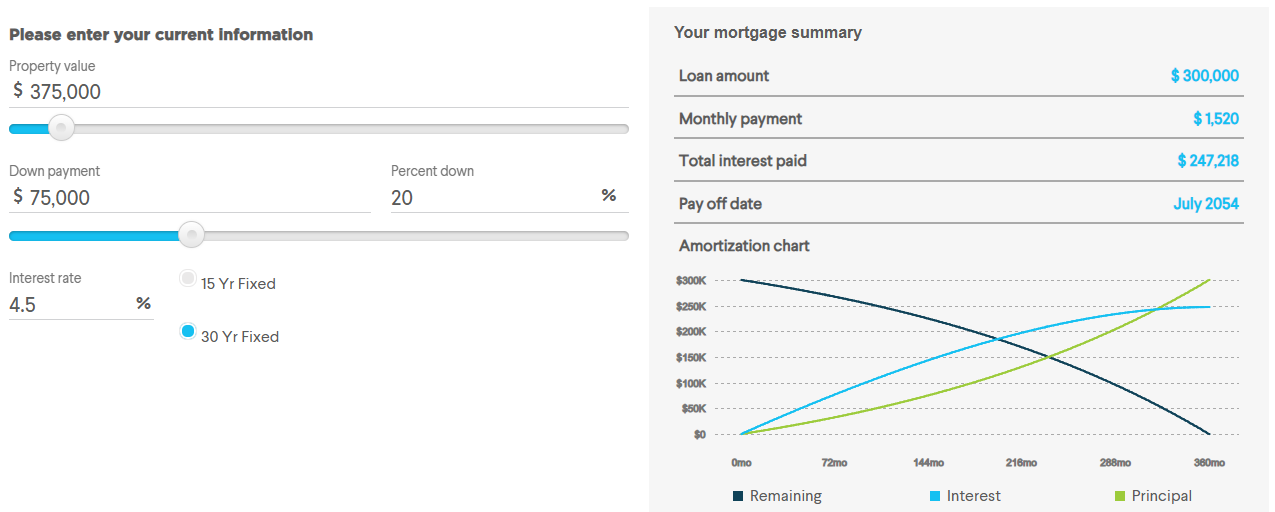

Sarah believes the myth that she needs a 20% down payment to buy a home. With her target home priced at $300,000, she thinks she needs to save $60,000 for the down payment. This misconception discourages her from exploring her options, delaying her home purchase by several years as she tries to save up the amount.

John: Knowing the Facts

John, on the other hand, understands that he doesn’t need a 20% down payment. He learns that with a SoFi offering, he can secure a mortgage with a downpayment of as little as 3%. For the same $300,000 home, John only needs $9,000 for the down payment.

Financial Impact Comparison

- Down Payment:

- Sarah (20% myth): $60,000

- John (3% fact): $9,000

- Loan Amount:

- Sarah: $240,000

- John: $291,000

Assuming both secure a 30-year fixed-rate mortgage at 4% interest:

- Monthly Mortgage Payments:

- Sarah: Approximately $1,145

- John: Approximately $1,388

Over the first five years:

- Total Payments Made:

- Sarah: $1,145 * 60 = $68,700

- John: $1,388 * 60 = $83,280

- Principal Paid (Approximate):

- Sarah: $11,700

- John: $14,300

- Interest Paid (Approximate):

- Sarah: $57,000

- John: $68,980

Equity and Financial Position After Five Years

Equity Built (Home Value Appreciation at 3% Annual):

- Home Value after 5 Years: $300,000 * (1.03^5) ≈ $347,800

- Sarah’s Remaining Loan Balance: $228,300

- John’s Remaining Loan Balance: $276,700

- Sarah’s Home Equity: $347,800 – $228,300 ≈ $119,500

- John's Home Equity: $347,800 – $276,700 ≈ $71,100

Conclusion

- Sarah: By waiting to save the 20% down payment, Sarah missed out on potential equity gains and spent years renting without building home equity.

- John: By understanding the fact, John bought a home sooner, paid less upfront, and started building equity earlier, despite slightly higher monthly payments and total interest paid over the first five years. Despite having less equity, John saved $36,420 ($128,700 – $92,280) over five years compared to Sarah. He can use this saved amount for other investments, emergency funds, or home improvements, potentially providing greater financial flexibility and growth opportunities.

Busting this myth highlights the importance of distinguishing fact from fiction. John's informed decision allowed him to enter the housing market earlier, build significant equity, and enjoy the benefits of homeownership without the prolonged delay and financial strain Sarah experienced due to her misconception.

Fixed Versus Variable – Understanding Fact from Fiction to Make Informed Decisions

When deciding between a fixed-rate and a variable-rate mortgage, understanding the facts is crucial. Fixed-rate mortgages offer stable payments, while variable-rate mortgages can offer lower initial rates that may change over time. Misconceptions about these options can significantly impact your financial stability and long-term costs.

HYPOTHETICAL EXAMPLE: UNDERSTANDING A FACT VS. BELIEVING A MYTH

Let’s compare two hypothetical homebuyers: Emily and Michael.

Emily: Believing the Myth

Emily believes the myth that fixed-rate mortgages are always better than variable-rate mortgages because they provide stability and predictability. She opts for a fixed-rate mortgage without considering her short-term plans and the potential savings of a variable rate.

Michael: Knowing the Facts

Michael understands the fact that while fixed-rate mortgages offer stability, variable-rate mortgages can be beneficial if he plans to sell or refinance within a few years. Michael opts for a 5/1 ARM (adjustable-rate mortgage), which has a fixed rate for the first five years and then adjusts annually.

Financial Impact Comparison

- Home Price: $300,000

- Down Payment: 10% ($30,000)

- Loan Amount: $270,000

- Mortgage Terms:

- Emily: 30-year fixed-rate mortgage at 4%

- Michael: 5/1 ARM at 3% for the first five years, then adjusts

- Monthly Mortgage Payments:

- Emily: Approximately $1,288

- Michael: Approximately $1,138 (for the first five years)

Over the first five years:

- Total Payments Made:

- Emily: $1,288 x 60 = $77,280

- Michael: $1,138 x 60 = $68,280

- Principal Paid (Approximate):

- Emily: $21,100

- Michael: $22,000

- Interest Paid (Approximate):

- Emily: $56,180

- Michael: $46,280

After the Initial Fixed Period (Assuming Rate Increases to 5% for Michael):

- Monthly Payment (Years 6-30):

- Michael: Approximately $1,405

- Payments Made (Years 6-30):

- Michael: $1,405 * 300 = $421,500

- Total 30-Year Payments:

- Emily: $1,288 * 360 = $463,680

- Michael: $68,280 (first 5 years) + $421,500 = $489,780

Equity and Financial Position After Five Years

- Home Value Appreciation at 3% Annual:

- Home Value after 5 Years: $300,000 * (1.03^5) ≈ $347,800

- Remaining Loan Balance:

- Emily: $248,900

- Michael: $248,000

- Equity Built:

- Emily’s Home Equity: $347,800 – $248,900 ≈ $98,900

- Michael's Home Equity: $347,800 – $248,000 ≈ $99,800

Conclusion

- Emily: By choosing a fixed-rate mortgage, Emily enjoys stable payments but pays more each month initially compared to Michael.

- Michael: By choosing a variable-rate mortgage with the plan to sell or refinance within five years, Michael saves approximately $9,000 in the first five years and builds slightly more equity. However, if he stays beyond the initial fixed period without refinancing, his monthly payments increase, potentially costing him more in the long run.

This comparison illustrates the importance of understanding the facts about fixed versus variable-rate mortgages. Michael’s informed decision to use a 5/1 ARM, aligned with his short-term plans, allowed him to save money and build equity faster. Conversely, Emily's decision, based on the myth of fixed-rate superiority, resulted in higher initial costs but provided long-term stability. Knowing the facts enables you to align your mortgage choice with your financial goals and timeline, optimizing your homeownership experience.

Popular Mortgage Myths Busted

Now, let’s look closely at some of the more common mortgage myths out there, and separate fact from fiction so you can make informed decisions.

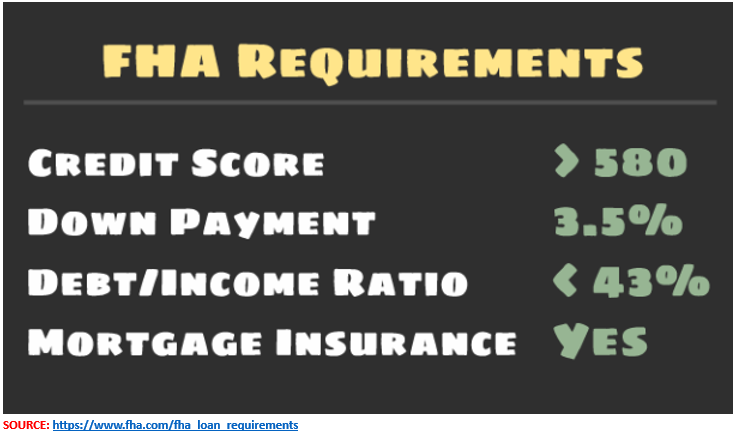

MYTH 1: YOU NEED A 20% DOWN PAYMENT

Fact: While a 20% down payment can avoid private mortgage insurance (PMI), it is not a requirement. Many lenders offer loans with significantly lower down payments.

The Federal Housing Administration (FHA) data shows that the average down payment for first-time buyers may be as low as 3.5%. Lower down payment options exist too. For instance, SoFi offers mortgages with down payments as low as 3%, making homeownership more accessible.

MYTH 2: ONLY PEOPLE WITH PERFECT CREDIT SCORES GET APPROVED

Fact: A perfect credit score isn’t mandatory for mortgage approval. Lenders consider a range of scores, and many borrowers secure loans with scores as low as 620. The Consumer Financial Protection Bureau (CFPB) reports that borrowers with mid-600 credit scores often qualify for mortgages with competitive rates. Most private lenders offer competitive rates, and welcome applicants with diverse credit backgrounds.

MYTH 3: PRE-QUALIFICATION AND PRE-APPROVAL ARE THE SAME

Fact: These terms are often confused, but they differ significantly. Pre-qualification is an initial assessment based on self-reported information, while pre-approval involves a thorough evaluation by the lender. Pre-approval holds more weight as it includes a credit check and detailed financial analysis, providing a clearer picture of your borrowing potential.

MYTH 4: THE LOWEST RATE IS ALWAYS THE BEST OPTION

Fact: The lowest interest rate might not always save you the most money. Borrowers must also consider other factors, including loan terms, fees, and lender points and credits. A loan with a slightly higher rate but lower fees can sometimes be more economical in the long run. It's important to only consider offers with transparent loan terms, helping you make a well-rounded decision.

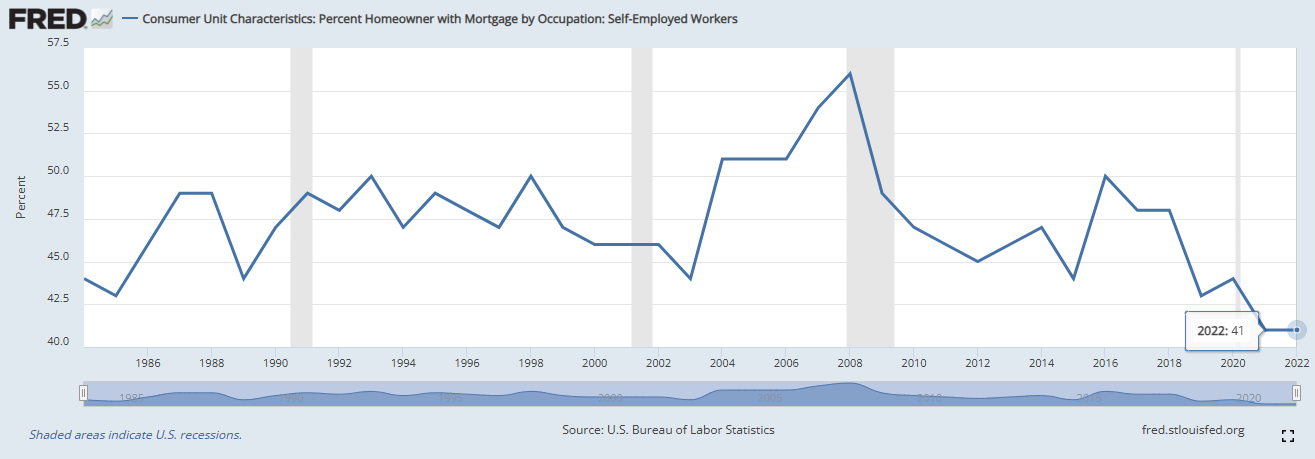

MYTH 5: SELF-EMPLOYED INDIVIDUALS CAN’T GET MORTGAGES

Fact: Self-employed borrowers can indeed qualify for mortgages. They might face additional documentation requirements, but many private lenders cater to their needs.

According to statistics from the US Fed, self-employed individuals comprised about 41% of all home buyers in recent years.

MYTH 6: YOU SHOULD PAY OFF ALL DEBT BEFORE APPLYING FOR A MORTGAGE

Fact: While reducing debt can improve your debt-to-income (DTI) ratio, it’s not necessary to pay off all debt. Lenders look at your overall financial health. A balanced approach, maintaining some debt while managing it well, can be more beneficial. Many lenders offer useful tools and resources to help you understand and optimize your DTI ratio.

MYTH 7: FIXED-RATE MORTGAGES ARE ALWAYS BETTER THAN ADJUSTABLE-RATE MORTGAGES

Fact: We've covered this myth in detail in one of our hypothetical scenarios earlier in this blog. Fixed-rate mortgages offer stability, but adjustable-rate mortgages (ARMs) can be advantageous in certain situations, especially if you plan to move or refinance within a few years. Analyzing your financial situation and future homeownership plans can help determine the best fit. Most lenders provide both options, along with guidance to choose the right one.

MYTH 8: IT’S BEST TO GET A MORTGAGE FROM YOUR BANK

Fact: While banks are a common source, shopping around can uncover better deals. Non-bank lenders often provide competitive rates and terms. Many fintech lenders provide excellent customer service and educational resources, making them the preferred contenders in the mortgage market.

MYTH 9: YOU CAN’T REFINANCE IF YOUR HOME VALUE HAS DROPPED

Fact: Refinancing options exist even if your home’s value has decreased. The Federal government has designed programs, like the Home Affordable Refinance Program (HARP), for this purpose. Look for a lender who offers various refinancing solutions tailored to different scenarios, ensuring you can benefit from lower rates or better terms.

MYTH 10: MORTGAGE INSURANCE IS PERMANENT

Fact: Mortgage insurance isn’t always for the life of the loan. Conventional loans allow for PMI cancellation once you reach 20% equity. Review your options and look for flexible loan terms that make it easier to reach this milestone, helping you eliminate PMI faster.

MYTH 11: RENTING IS ALWAYS CHEAPER THAN BUYING

Fact: While renting might be cheaper in the short term, buying can be more cost-effective over time due to equity building and tax benefits. For example, if you rent for $1,500 per month, you pay $18,000 annually with no return on investment. Conversely, with a mortgage, part of your monthly payment goes towards building equity in your home.

MYTH 12: YOU CAN’T GET A MORTGAGE IF YOU’VE HAD A FORECLOSURE

Fact: It’s possible to get a mortgage after a foreclosure, though you’ll likely need to wait a few years and demonstrate improved financial health. The FHA offers loans to borrowers three years post-foreclosure or a deed-in-lieu of foreclosure (DIL) action, provided they’ve reestablished good credit. SoFi also considers applicants with complex financial histories.

MYTH 13: YOU MUST STAY IN YOUR HOME FOR AT LEAST FIVE YEARS FOR IT TO BE WORTHWHILE

Fact: The five-year rule is a general guideline, but it isn’t a strict requirement. Market conditions, home appreciation, and your personal circumstances can affect this. If your home’s value increases significantly, selling before five years could still be profitable. Many lenders provide tools to help assess your home’s value and market trends.

MYTH 14: THE MORTGAGE PROCESS IS TOO COMPLICATED

Fact: While the mortgage process involves several steps, it doesn’t have to be overwhelming. Many lenders have streamlined the process with user-friendly online applications and support.

By educating yourself and working with a reputable lender, you can navigate the process smoothly and efficiently.

MYTH 15: YOU CAN'T GET A MORTGAGE IF YOU HAVE STUDENT LOANS

Fact: Having student loans doesn’t disqualify you from getting a mortgage. Lenders consider your overall debt-to-income ratio, including student loans. For example, a borrower with a monthly income of $5,000 and total debts (including student loans) of $1,500 would have a DTI ratio of 30% ($1,500 / $5,000), which is often acceptable for mortgage qualification. It's advisable to work with an adviser who understands the impact of student loans and offers tailored advice for managing them alongside your mortgage.

SoFi’s Competitive Mortgage Offerings

Amidst debunking these myths, it's important to highlight that SoFi offers competitive mortgages with low down payments, transparent terms, and excellent customer support. With SoFi, you'll not only be working with a lending partner that's recognized as a Top Mortgage Lender by CNBC, but also with a leading fintech company that's changed the mortgage lending landscape.

Using cutting edge technology for speed and convenience, the company offers a variety of mortgage options including conventional mortgages (both conforming and jumbo), FHA mortgages, VA mortgages, and HELOCs. They also offer fixed-rate mortgages with terms of 10, 15, 20, and 30 years.

Unraveling Common Misconceptions for Smarter Home Buying Decisions

Understanding the facts behind common mortgage myths empowers you to make better decisions. Remember, a 20% down payment isn’t mandatory, you don't need a perfect credit score, and shopping around for the best rates and terms can save you money. Don't believe all the myths and hype around mortgages. Equip yourself with accurate information, and embark on your home buying journey with confidence.

Featured image sourced from Shutterstock

This post was authored by an external contributor and does not represent Benzinga’s opinions and has not been edited for content. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice. Benzinga does not make any recommendation to buy or sell any security or any representation about the financial condition of any company.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.