Stocks ticked lower last week with the S&P 500 shedding 0.2% to close at 4,450.32. The index is now up 15.9% year to date, up 24.4% from its October 12 closing low of 3,577.03, and down 7.2% from its January 3, 2022 record closing high of 4,796.56.

I spent the past week at FutureProof and Excell, two leading industry conferences for financial advisors.

I like attending events like these because I inevitably meet people I’d probably never cross paths with under normal circumstances. That means I get exposed to a wide array of views, some of which might affect the way I think about things.

One topic that came up in many of my conversations was holistic thinking.

When you think about your financial situation holistically, you realize it isn’t characterized just by the assets you hold in your portfolio, but also the industry in which you work. For example, you may be a young professional with a little bit of savings conservatively invested in a broadly diversified S&P 500 index fund. But if you work at a VC-backed startup and it’s your only source of income, then you are far more financially exposed to speculative risk than your 401(k) statements might suggest.

Speaking more broadly, it’s always treacherous to consider any piece of data in isolation. In the markets and the economy, there almost isn’t enough context to take into account when considering specific metrics.

The Richer You Get, The Less You Need To Save

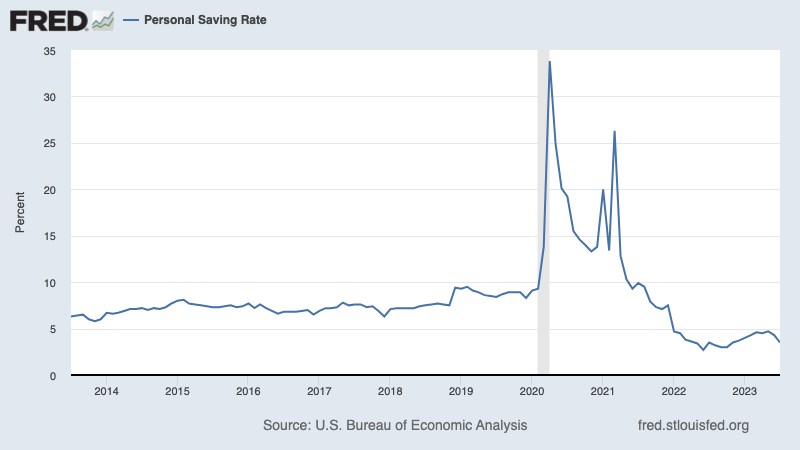

One unsettling metric that often gets misinterpreted and taken out of context is the personal saving rate — the percentage of disposable income that’s saved, not spent — which has been trending below pre-pandemic levels over the past two years.

The personal saving rate is relatively low. FRED

Does a low saving rate mean households are going broke as they use more of their incomes for spending instead of saving?

The short answer is no. As we’ve discussed repeatedly at TKer, household finances are quite strong. People have money.

In fact, a declining saving rate may be a reflection of household finances getting even stronger.

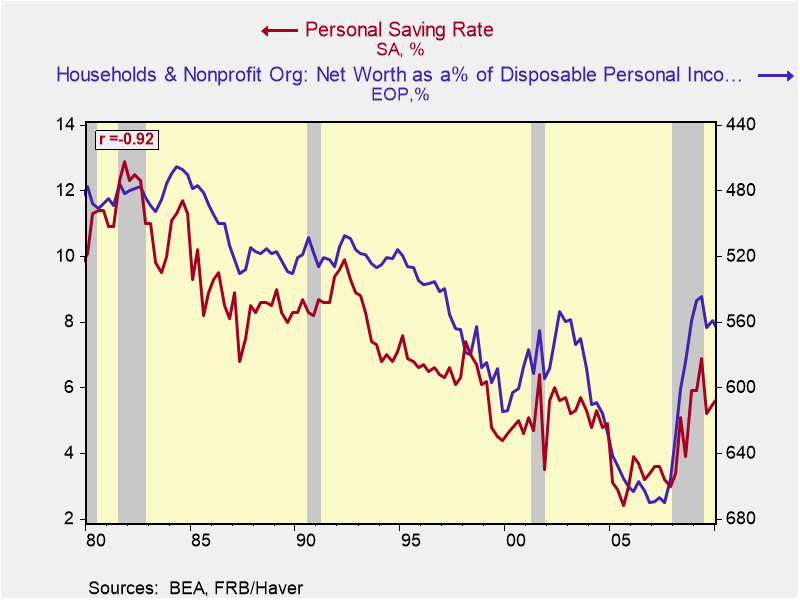

Renaissance Macro’s Neil Dutta recently reviewed the historical relationship between the personal saving rate and net worth. His findings were a bit counterintuitive.

“From the 1980s to 2000s, there was a pretty neat and clean relationship: as net worth rose relative to income, the household saving rate declined,” Dutta observed in a September 8 note. “This made sense as households saw rising asset values as a low risk form of wealth creation. When you are ‘loaded,’ you have less reason to save.“

From the 1980s to 2000s, the personal saving rate had an inverse relationship with net worth. (Source: Renaissance Macro)

This relationship broke down in the wake of the global financial crisis.

“While net worth rose relative to incomes, the saving rate ended up rising about 2ppts over the decade, ending close to 9% in 2019,” Dutta noted. “Households were highly sensitive to the previous asset deflation, boom-bust, and rising asset prices, while welcomed, did not build the confidence in folks to actually save less (after all, household balance sheets needed to be repaired).“

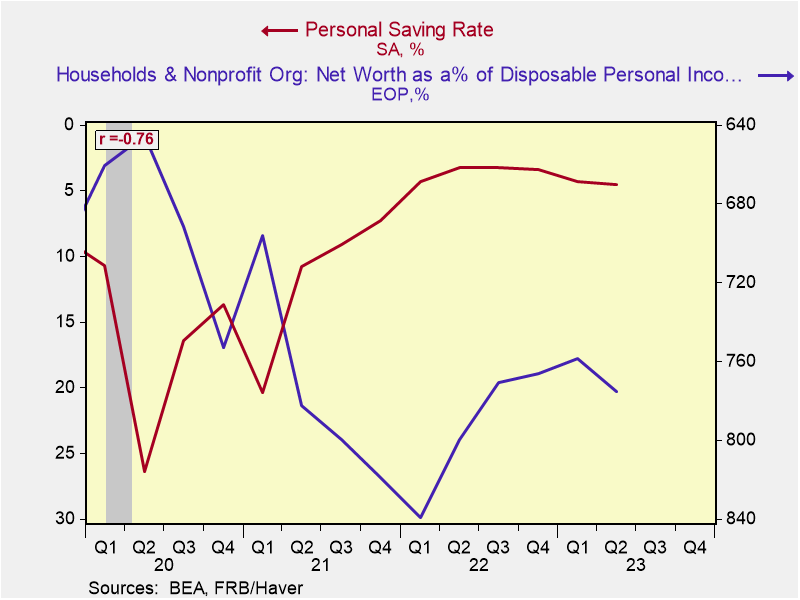

However, Dutta now argues that we may be returning to that pre-financial crisis trend, with home prices near record levels and stock prices rising sharply from their lows.

“If my stock portfolio is rising and home prices are climbing, I don't feel like I need to be saving as much,” he said (emphasis added). “This would be an argument supporting the idea that there is not anything ‘wrong’ with a saving rate at 3.5%. Moreover, it is not immediately clear why people need to take their savings rates up to pre-pandemic levels either.“

Why save more when my net worth is already rising? (Source: Renaissance Macro)

It’s Never Ceteris Paribus

Ceteris paribus — Latin for “all other things being equal” — a falling saving rate doesn’t seem like good news.

But as we often see, things are never ceteris paribus. Read more here and here.

Similar to when companies face challenges, the question is not whether a development is bad. Rather, the question is whether companies can keep earnings growing despite the development.

With regard to household finances, the question is not whether a falling saving rate in itself is bad. Rather, the question is: Does this mean household finances are deteriorating?

The world is complex. But it can be complex in good ways. Because sometimes something might seem bad, when in reality that something might actually reflect something good.

A version of this post was originally published on Tker.co

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.