The following post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga.

By better understanding the various investment and property classifications available to them, commercial real estate investors can achieve a much clearer understanding of what to expect both during the lifetime of an investment as well as upon a project’s completion.

While every commercial real estate property has its own unique characteristics that investors should research when considering a potential deal, most private real estate investments can be classified according to certain overarching characteristics. These classifications fall under two umbrellas: one focusing on the investment characteristics and the other relating to the property itself.

Below, we will look at these two classification metrics and explain how these breakdowns are crucial when evaluating potential real estate investments.

Profiling An Investment

Most property investments fall into four broad categories that each characterize an investment’s unique risk and return profile. These profiles include:

- Core: a lower risk/return investment that focuses on stable, fully leased, multi-tenant properties within strong, diversified markets that require minimal leverage to fully realize

- Core Plus: a moderate risk/return investment into a similar property as core, but utilizing a greater degree of borrowed capital to increase the property’s net operating income through modest property improvements

- Value-add: a medium-to-high risk/return investment that involves utilizing leverage to significantly improve a damaged, outdated or otherwise underperforming commercial property to increase both its value and net operating income

- Opportunistic: a high risk/return investment that requires significant leverage to enhance effectively non-operating properties, these generally also carry a medium-to-long-term time horizon to fully realize

Simply put, higher-risk strategies will potentially yield low or negative cash flow in the initial stages of the project, but may deliver a higher return on investment once the property improvements are reflected in its lease operations and property value. On the other hand, lower risk projects will potentially deliver steady passive income throughout the lifetime of the investment, but the final yield may be more modest.

Due to the high property values and low capitalization rate (a property’s net operating income divided by its purchase price) of the current commercial real estate, institutional real estate investors are increasingly interested in the higher risk/return investment approaches. The 2019 “CBRE Americas Investor Intentions Survey” shows that active real estate investors are consistently more interested in value-add and opportunistic investments as opposed to less risky core investments (the secondary and distressed categories are debt investments).

While this is not an endorsement of any particular strategy, since each investor needs to choose investments based on his or her own objectives, the results speak to the current investment environment. Higher risk/return real estate strategies are currently being rewarded, while core investments lack the incentives to draw capital away from more profitable assets, even if they are marginally riskier.

Why We Focus On Value-Add Investments

Investments listed on the iintoo platform generally fall into the value-add category within middle-market commercial properties. These properties and their sponsors are highly vetted and extensively researched by our team and each investment represents what we feel is the best opportunity to reposition the property to a higher and better use.

Generally speaking, our value-add investments are funneled into meaningful property upgrades or operational improvements that require only moderate repositioning, re-tenanting or redevelopment. Our end goal is to increase the net operating income of the property without significantly disrupting its current income-generating operations, potentially leading to the property appreciating in value.

Of course, the value-add strategy necessarily involves greater risk than core or core-plus approaches, although it also offers potentially higher return objectives. While this risk/return dynamic is at the core of all asset investing, our aim when researching property investments is to find opportunities that can best mitigate risk while displaying the fundamental characteristics that position the property to outperform expectations. This is also why we often focus on growing or undervalued markets that display strong and consistent demographic trends.

In addition to this vetting, we also strive to remain transparent about the specific costs and anticipated return that we expect will accompany renovations within each property. Because the value-add strategy generally involves taking on some amount of debt capital or interrupting the income-generating operations of a property, it’s important for investors to understand where that capital is intended to go and how it should ultimately return. For example, an investment with a more extensive development plan will include details that highlight how the initial cash flow of the property will likely fluctuate, but will also include details about the appreciation potential of those renovations.

Nevertheless, investors who are interested in the value-add strategy should always bear in mind that any return estimates, even the best or most conservative, are still only estimates. Real estate is an inherently higher risk/return investment compared to other multi-year investment assets and it generally works best as part of a well-rounded and diversified investment portfolio. Investors need to determine on their own which strategy aligns with their level of risk tolerance and their overall investment goals.

Investing in real estate? Visit iintoo for the latest offer

The A, B, Cs Of Property Classification

Apart from the investment strategy, properties themselves are classified—or graded—according to their specific architectural and ownership characteristics as either Class A, Class B or Class C properties. The grades generally consider things like the age of a building and its amenities, the demographics of its location, and the value of its rental income and clientele.

While there is no precise formula by which properties are placed into classes, the breakdown can generally be thought of as follows:

- Class A: generally newer properties built within the last 15 years with top amenities, high-income earning tenants, and low vacancy rates. Class A buildings are well located in a market and are typically professionally managed. They typically demand relatively high rents and have very few deferred maintenance issues.

- Class B: These properties are generally older, tend to have lower-income tenants and may or may not be professionally managed. Rental income is typically lower than Class A, and the properties may have some deferred maintenance issues. Generally, however, these buildings remain relatively well maintained. These are often properties that sponsors seeking “value-add” opportunities may tend to chase because through renovation and common area improvements the property can often be repositioned to be marketed at higher rental rates. Buyers are generally able to acquire these properties at higher cap rates (i.e., lower purchase price relative to net operating income) than for Class A properties.

- Class C: properties that are typically more than 20 years old and located in less than desirable locations. The properties are generally in need of renovation, including updates of a building’s infrastructure, and tend to have lower rental rates compared to other local properties. Some Class C properties need significant redevelopment work before they can be expected to provide steady cash flows.

What Does Property Classification Mean For Investors?

As you might have gleaned from their descriptions, these classifications can serve to illustrate a property’s overall risk/return profile in a similar way as the overarching investment strategy. While property grades should absolutely factor into an investor’s return objectives, it’s good to think of them more as the starting point for the overall investment approach, rather than the driving force behind the investment. After all, each investor’s return objective should inform what class of property they should seek out.

For instance, a Class A property will generally be a core or core plus investment simply because its property value and income-generating activities are already near the top of the market. While these properties often appreciate in value under robust economic conditions, barring a massive addition that may push the investment into the value-add category, improvements to a Class A property may generate marginally lower returns from an investment standpoint, relative to a ‘fixer-upper’ project.

Since Class B and C properties have more fundamental areas for improvement, they will generally fall into higher risk/return investment strategies. Class C properties are typically the riskiest, with some Class C properties requiring significant redevelopment work before they can be expected to provide steady cash flows.

However, Class B properties are often targeted by investors since buyers can acquire these properties at higher cap rates (i.e., lower purchase price relative to net operating income). Through basic renovation and common area improvements, some Class B properties can appeal to Class A tenants and significantly improve their net operating income.

If I Were to Invest in Commercial Real Estate Today, Where Should I Look?

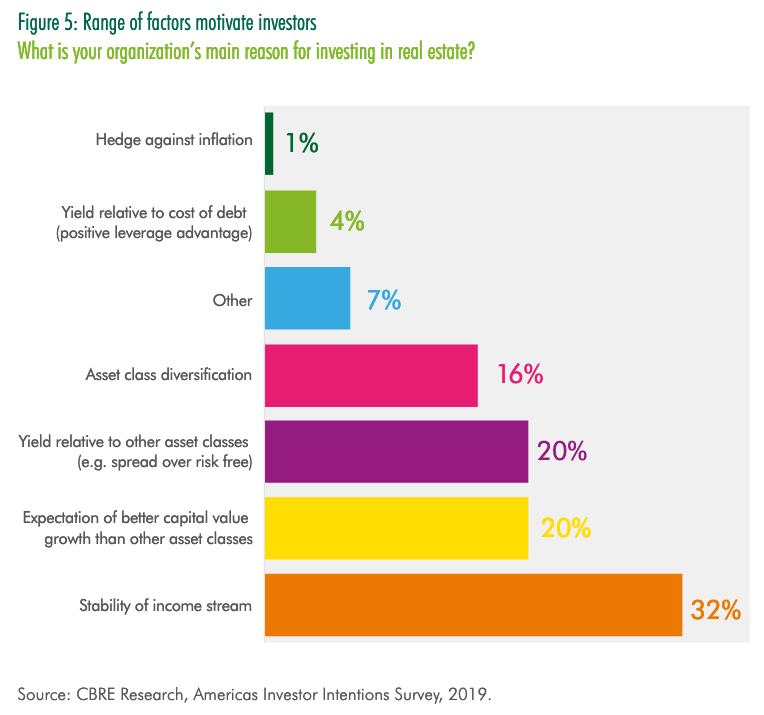

A recent study by CBRE indicates that plurality of investors chose to get into commercial real estate due to their interest in diversifying into a stable income stream over the entire investment lifetime.

With these priorities in mind, it stands to reason that an investment strategy focusing on Class B properties with light to moderate renovations may offer potential upsides. Even after they are renovated, these properties can often provide renters with a valuable alternative to newly constructed properties.

Furthermore, CBRE research suggests that there is currently very little in the way of free rent or other concessions being offered on Class B properties. In this way, these properties seem to be well-positioned relative to higher-end Class A buildings, where such concessions are frequently offered in response to competition coming from newly constructed complexes.

Class A properties can potentially produce strong returns for investors for long stretches and provide a degree of capital preservation for individual and institutional alike, but during periods of economic uncertainty this property class can be a riskier investment, as renters tend to move to less expensive apartments when under financial duress and owners have to lower rents to compete in the market. For this reason, Class A properties have the highest vacancy rate among apartment buildings. Therefore, investors should be cognizant of the timing of their decisions, as well as the submarket demand and supply dichotomy, particularly given the fact that the bulk of recent development activity has tended to be in high-end Class A properties.

As always, it’s important for investors to conduct their own due diligence. At iintoo, we pride ourselves in our vigorous deal pre-vetting process, through which less than 1% of screened deals are made eligible to be offered to our investors. And while we make this process as thorough as possible and offer complete project oversight and progress reports throughout each investment’s life cycle, we want our investors to be cognizant of the underlying commercial real estate classes they can choose from, as well as the variables that factor into making a successful investment decision. After all, we’re in the business of lasting value creation and community-building. To that end, we’re proud of everything we’ve accomplished together to date.

This is an advertisement for iintoo.com. Securities offered through Dalmore Group LLC, a registered broker-dealer and member of FINRA/SIPC. This is not an offer to buy, sell or trade securities. Investments are not FDIC insured, have no bank guarantee, and may lose value. For more information please read our full disclaimer.

The preceding post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga. Although the piece is not and should not be construed as editorial content, the sponsored content team works to ensure that any and all information contained within is true and accurate to the best of their knowledge and research. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.