An interviewer once asked Warren Buffett about the worst trade he’d ever made… and he didn’t hesitate to answer…

Buying Berkshire Hathaway.

When Buffett scooped up majority ownership of the company in 1964, it was a failing textile manufacturer. At first, he tried to salvage the textile business model… while expanding into other businesses. For example, he added the first insurance business in 1967.

Eventually, however, Buffett realized it was a lost cause. He divested the textile assets… and pivoted his company towards insurance.

Buffett says he learned an important lesson from that “worst investment ever”…

“If you want to be known as a good manager, buy a good business,” he said.

As we now know, Buffett was able to turn that initial investment around. Over the years, he’s grown Berkshire into one of the largest publicly traded companies in the U.S.—a global conglomerate that has outperformed the market by a staggering margin.

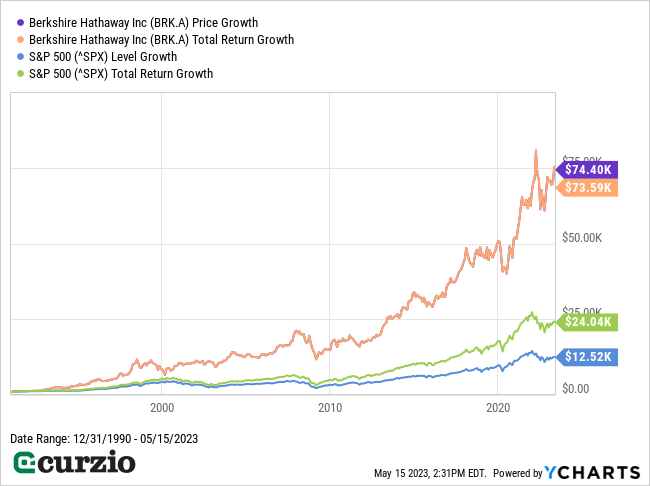

As you can see from the chart below, $1,000 invested in the market at the end of 1990 would be worth more than $24,000 today (with all dividends reinvested ).

The same amount invested in the shares of Berkshire Hathaway would be worth almost $74,000 today.

Buffett didn’t turn Berkshire around by sheer luck…

He did it by following a very specific investment philosophy that goes back to that initial lesson of “buying good businesses”:

Invest in (and hold) businesses that dominate their sectors… and have the means to keep growing their success.

In fact, all of Buffett’s biggest long-term successes have been businesses that are less dependent on the economy or the whims of consumers than their peers. And each one possesses a unique set of qualities that set it apart from the competition, like a strong brand name, established business relationships, or having access to certain natural resources.

These advantages allow the business to grow its customer base… collect more consistent revenues… and generate more reliable profits (which it can pass along to shareholders via growing dividends and share buybacks).

Let’s take a look at three of Buffett’s current favorite holdings as examples…

1. Coca-Cola KO

Buffett loves Coca-Cola. I don’t mean the soft drink (although he does love that, too); I mean the stock. Berkshire Hathaway owns 400 million shares of KO, which it spent seven years accumulating… completing the purchases in August 1994.

It’s no surprise KO is one of Buffett’s favorite “buy-and-hold-forever” stocks. The king of soft drinks is the quintessential sector dominator. Thanks to its brand name, massive distribution network, and marketing prowess, the company has built an empire that expands far beyond its namesake drink.

Buffett spent $1.3 billion on his KO stake back in the mid-’90s. Today, with the stock trading around $64 (near its all-time highs), the total value of those 400 million shares is $25.6 billion. Altogether, Buffett has made almost 20x his original investment on KO.

Plus, the stock’s dividend has consistently grown over the years, rising by 64% over the past decade alone. While Berkshire collected $75 million in KO dividends in 1994… in 2022, it collected $704 million.

Even investors who haven’t owned KO as long as Buffett have been rewarded nicely with price appreciation and growing dividends. As you can see in the chart below, KO’s share price rose more than 50% over the past decade. And if you take dividends into consideration, your return would more than double that number (106%).

2. American Express AXP

Like Coca-Cola, American Express is one of the best-known brand names in its industry—in this case, financial services.

Also like Coca-Cola, Buffett’s love for American Express goes back several decades. He began building this position in the 1960s, reaching his current stake of 151 million shares in 1995. Altogether, the stock cost him about $1.3 billion. Today, it’s worth more than $22 billion.

And the dividends Berkshire collects from AXP have also grown substantially over that time frame, from $41 million (per year) to $302 million.

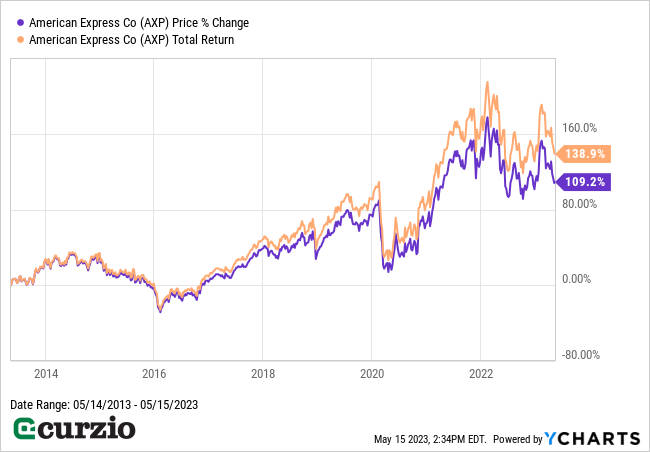

As you can see from the chart below, collecting and reinvesting dividends added an extra 40% to AXP’s total return over the past 10 years. The stock returned almost 110% in price appreciation… and 139% with dividends.

Buffett has loved this company since the 1960s, when it was a rare credit card processing pure-play. But even as more competition emerged, AmEx carved out a key niche in the industry by focusing on the wealthier part of the population.

In short, while American Express isn’t the only credit card and merchant processor in the U.S., it has all the characteristics Buffett looks for in a stock.

3. DaVita DVA

Healthcare company DaVita is much smaller than either Coca-Cola or AmEx. Its market cap is less than $9 billion… vs. $277 billion for KO and $112 billion for AXP.

Still, Buffett is DaVita’s largest shareholder: Berkshire owns more than 36 million shares of the company—almost 40% of all shares outstanding.

That’s because, despite its smaller size, DaVita has a dominant position in a niche market. The company accounts for a third of all U.S. dialysis treatments.

In 1972, Medicare was extended to all patients of any age with irreversible kidney failure—and to this day, dialysis remains one of the largest Medicare programs. While kidney failure and dialysis account for only 1% of all Medicare recipients, they make up more than 7% of the Medicare budget.

Owning a dominant company in such a critical segment with a guaranteed customer (Medicare) is a no-brainer for Buffett.

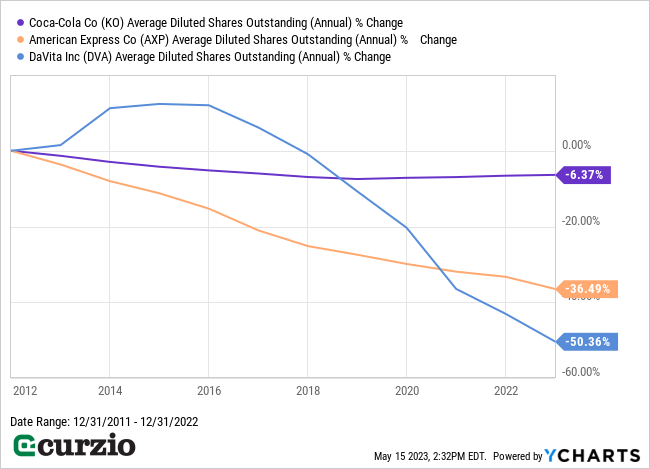

While DaVita doesn’t pay a dividend, it rewards shareholders by actively buying back shares. As you can see below, since 2011 (when Buffett first started accumulating a stake in DaVita), the company has repurchased more than 50% of its stock.

Think of stock repurchases as a way of increasing each owner’s claim on profits at no additional cost to shareholders. When the share count goes down, your personal stake in the business goes up. All else equal, a company that buys back its own stock is a better long-term investment than a company that keeps issuing shares.

Conclusion

When it comes to investing in “good businesses,” Buffett looks for a few key qualities that set him up for success every time.

He likes strong, sector-dominating businesses that will continue to deliver profits over the long term across all business conditions… These are the companies that can—and do—reward their shareholders with growing dividends and share buybacks—the type of companies you’d want to see in your own portfolio, too.

These criteria might seem overly simple… But as Buffett’s track record shows us, they can help your portfolio outperform over the long term.

This content is for informational purposes only and is not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.