Zinger Key Points

- 4 energy stocks to watch for 2025 with strong fundamentals, dividends, and demand.

- Our government trade tracker caught Pelosi’s 169% AI winner. Discover how to track all 535 Congress member stock trades today.

Energy independence has always been crucial to national security, and that has become even more highlighted in the wake of Russia's invasion of Ukraine and the ongoing fighting in the Middle East.

While energy prices in the United States have moderated in the last few years, energy independence remains a bipartisan political issue, and U.S. domestic oil production is currently at all-time highs.

But despite these gains in energy production, the sector hasn't reaped the benefits in 2024. The SPDR Energy Select ETF XLE is up just 10% year-to-date compared to a 28% gain from the S&P 500.

President-elect Donald Trump has promised to cut regulations to help oil and gas companies, and renewable energy companies continue to make strides toward lowering costs and expanding market share.

Today, we look at four energy stocks that could break the sector out of its doldrums in 2025.

How We Chose

If you're looking for explosive growth in the energy sector similar to tech, you'll likely be left disappointed. The energy sector is highly dependent on factors beyond the control of companies and governments, such as locating potential patches, equipment and production costs, and OPEC machinations.

The energy stocks we selected share a few common factors: strong balance sheets with income growth and low costs, a sustainable dividend, and solid demand for their products and services. These companies also have strategies to manage volatile commodity prices and unpredictable markets. It’s also wise for investors to diversify across industries, so we've included traditional oil and gas, renewables, and storage firms in our list.

Top 4 Energy Stocks for 2025

Here are the four stocks we picked for next year based on the abovementioned factors. We attempted to diversify across the sector with companies in different industries while keeping the core themes of sound fundamentals, dividend yield, and promising business outlook.

Diamondback Energy Inc. FANG

Owner of one of the best stock tickers on the exchanges, Diamondback Energy is an oil and gas mining company that also claims over 4,000 acres of valuable land in Texas's oil-rich Permian Basin. Founded in 2007 and trading publicly since 2012, Diamondback has been a prolific acquirer of companies. In September, the company completed a $50 billion merger with Endeavor, and this trend could continue with a more M/A-friendly administration taking the White House next January.

FANG shares have given up most of their 2024 gains in the last six months, but the stock appears to have found support at the current $165 level. The stock also has all the features you want in an oil and gas company: steady dividends, quality management, and access to valuable reserves. The stock's dividend yield is 2.16% with a nearly 30% growth rate over the last three years, but the payout ratio remains just 20.6%, indicating a growing but stable dividend. FANG also has a reasonable P/E ratio of 9.96 and shows 34 on a Relative Strength Index (RSI), indicating that the stock could be approaching oversold status.

ConocoPhillips COP

ConocoPhillips is one of the world’s largest oil and gas companies, a remainder from the initial split of Standard Oil almost 100 years ago. It is headquartered in the United States but has operations expanding around the globe. Like most large-cap stocks in the energy sector, it had a rough performance in 2024 (it's basically traded flat for two years), but the stock is also poised to bounce back thanks to its LNG pipelines and expanding cash flows.

President-elect Donald Trump has promised to cut regulations and be more friendly to LNG projects than President Biden, which could finally boost ConocoPhillips from its seemingly endless bout of rangebound trading. The stock has a low P/E (12.39), a high-yielding dividend (2.99%), and support from analysts like JPMorgan, which recently made it one of its more prominent upgrades. Overall, COP is a consensus Buy based on an aggregate of 27 different analyst ratings with an average price target of $135, which implies more than 30% upside from the current market price.

December 15th is your last chance: Study proven patterns, learn precise entries, and analyze past winners up to +1,452%. SAVE MY FREE SPOT

Brookfield Renewable Corp. BEPC

Despite Trump's promises to roll back federal EV mandates and general ambivalence to clean energy, renewables growth is likely here to stay. Brookfield Renewable Corp is one company to consider based on this trend, with divisions in the United States, Europe, and South America.

Unlike many of its clean energy peers, BEPC stock pays a dividend with a robust 4.65% yield. The company has a relatively small market cap, approaching $5.5 billion, and coverage is only from two major analysts: JP Morgan (Hold) and Wells Fargo (Buy). However, both investment banks think the stock has an upside based on their price targets ($32 for JPMorgan and $34 for Wells Fargo). The chart also looks appealing; after a three-year downtrend in price, a double-bottom pattern formed between the October 2023 and April 2024 lows, with a breakout occurring shortly after the second bottom. Keep an eye on this stock chart over the next 12 months.

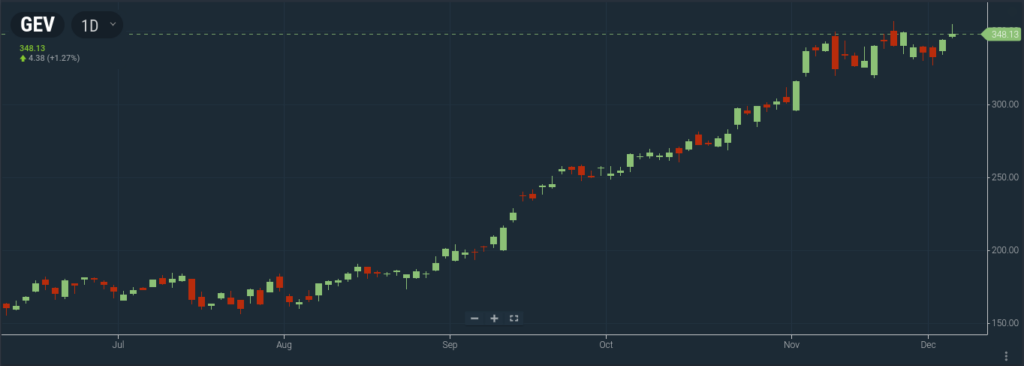

GE Vernova Inc. GEV

GE Vernova was spun out of General Electric when the firm decided to split its business divisions into their own companies. Formerly GE Power and GE Renewables, GE Vernova began trading as a public company in 2023 and has been one of the few bright spots for the energy sector in 2024. GE Vernova currently operates in four segments: Power, Wind, Electrification Systems, and Electrification Software. The company recently received a large contract from the French government to build a $338 million power substation, and another contract bid in Germany to help stabilize the power grid.

Analysts have long favored the stock, but even after more than doubling up in 2024, bullish reports continue to pour in. The three most recent reports come from Wolfe Research, Guggenheim, and Barclays, and each applied a Buy rating on the stock with respective price targets of $403, $400, and $420. From a technical standpoint, the stock trades well above its 50- and 200-day moving averages and reads 61 on the RSI, which indicates the stock still hasn't reached oversold status. GEV doesn't pay a dividend, but its sales growth trajectory and bounty of public projects make it a difficult energy stock to ignore heading into 2025.

Prepare Now for 2025's Biggest Q1 Trade

Image via Wikimedia Commons

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.