My wife and I just had a baby boy on May 8, so

I'll be taking a short break from the Resource Prospector. I've asked

Andy Crowder, a seasoned technical analyst and options trader to fill in

while I'm away. He has a very unique view on the commodity markets and

I'll think you'll find his viewpoint interesting and

insightful.

Is Now the Time to Sell

Oil?

Most investors have a commonly held belief that oil speculators are to blame for high oil prices.

Certainly there is some anecdotal evidence to

suggest that speculators can move the markets. After a 20 percent run-up

in crude oil since December, long-term commodity bull Goldman

Sachs GS recently warned clients to take some profits

off the table. The large investment bank estimates suggest speculators

are inflating the price of crude as much as $27 a barrel.

Goldman is certainly right about one thing,

speculators have pushed the price of oil to levels not seen since

September 2008. But does that mean you should liquidate all of your

oil-related holdings?

I thought it might be interesting to look at what happens to the price of oil in the weeks and months AFTER lots of oil speculators flood the markets with long positions.

This is what I came up with.

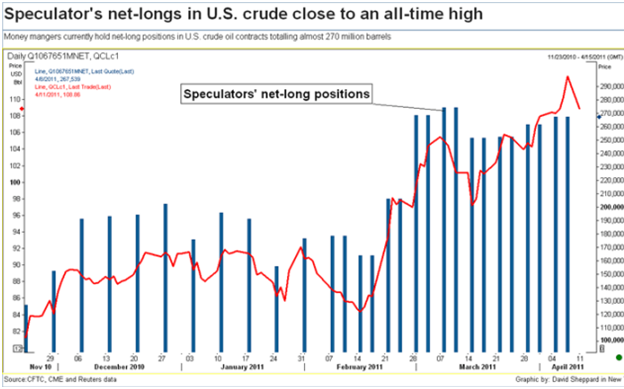

***According to the U.S. Commodity Futures Trading

Commission (CFTC) large speculators are nearing the net-longest in the

history of crude oil futures. Contrary to what the talking heads

would have you believe historically, extreme net-long positions in oil

futures have not been a consistent indicator.

This chart shows that speculators have more long

positions than at any point over the past 9 months. Everyone is betting

one way - so it might stand to reason that a good contrarian investor

should bet the other way.

After looking at the chart there is no denying

that speculators have jumped in with both feet, pushing their net long

position to one of the largest in history.

As a general rule of thumb, taking the other side

of speculator extremes in commodities is a workable strategy. You

have to be careful since commodities can get stuck in supply/demand

imbalances that will overrule anything else, but as a rule of thumb it's

pretty good.

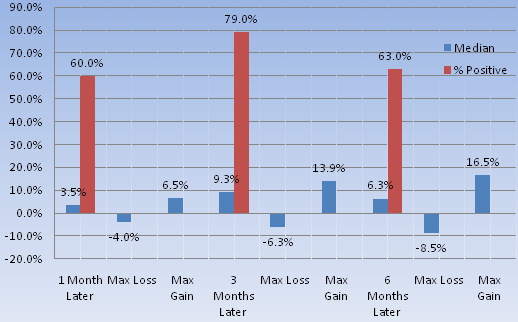

So we might expect to see negative returns when

looking at crude oil's future performance after large speculators become

extremely net long. Let's check, going back to 1986:

After Large Speculators Have Reached Extreme Net Long Positions in Crude Oil Futures

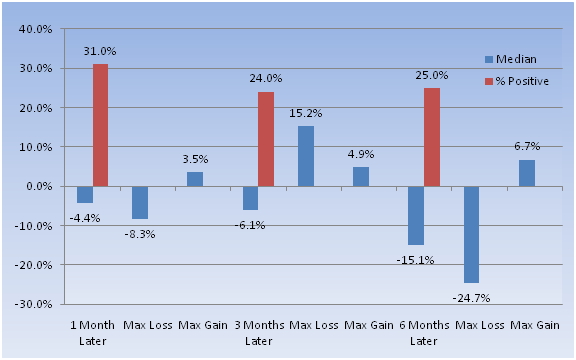

After Large Speculators Have Reached Extreme Net Short Positions in Crude Oil Futures

***Well, that's surprising.

Crude's future returns were precisely the

opposite of what one might expect. Three months after

speculators had become the net longest in at least three years, crude

sported gains 79 percent of the time, and had a median maximum gain that

was twice as large as the maximum loss.

The opposite was also contrary to

expectations. When speculators were extremely net short, we would

expect crude to bounce. But three months later, it was positive

only 25 percent of the time, and had exceptionally negative average

returns.

Volatility in all cases was extremely high.

Something else to note is that when speculators were extremely net long,

like now, much of the maximum loss happened right away - within the first

month after the extreme. Same goes for the opposite; when

speculators were extremely net short, much of the knee-jerk bounce

occurred within the first month.

So if we're going to look at this in a contrary way, then we'd probably best be served by watching for an immediate reaction, since we don't really have any historical legs to stand on longer-term.

So far this conclusion is true. After speculators

hit the latest net-long extreme oil has taken a bit of a reprieve losing

4.5 percent over the past week.

Now we will have to wait and see if the statistics hold true over the next six months.

Investment implications: if you're looking for a

time to build or add to a position in an oil investment, you should wait

for a time when there are lots of net-long positions, as there are now.

Buy your investment on dips during this period, and higher priced oil

should reward you handsomely.

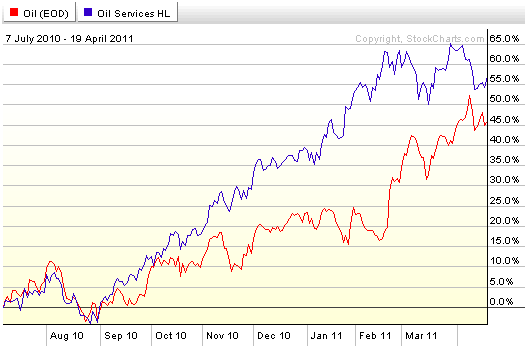

If you're looking for an investment with the best

upside to higher oil prices, I would suggest the oil services ETF. These

companies typically become more profitable the higher oil's price

goes.

The Oil Services ETF (OIH) is comprised of the top

14 companies within the oil services industry. Besides commodity futures,

oil services are the most levered to higher oil prices. Simply put, they

are the most direct and lucrative way to take advantage of price

increases in crude oil.

Investing in OIH relieves you of the difficult

task of stock picking. The ETF provides excellent exposure to an energy

sub-sector that will benefit from increased global demand and upcoming

inflation.

If you have any questions about this topic or any other commodity investment, drop me a line at editorial@resourceprospector.com.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.