Wave the green flag. Earnings season is underway.

It all got started today with JPMorgan Chase & Co. (NYSE:JPM) and Citigroup Inc (NYSE:C) delivering fresh sets of results hot off the press. The overall market has a mixed tone, with Nasdaq 100 (NDX) futures higher but other indices trending lower overnight after yesterday’s incredible rally.

It’s the start of Amazon.com, Inc.’s (NASDAQ:AMZN) Prime Day, and Apple Inc. (NASDAQ:AAPL) has an event later where it’s expected to reveal its new iPhones.

Major indices took a bump down early last night after Johnson & Johnson (NYSE:JNJ) paused its Covid-19 vaccine trial due to an “unexplained illness,” but now it looks like JPM is helping bring us back.

Bank Earnings Solid Across The Board

JPM beat Wall Street’s average top- and bottom-line estimates and saw shares rise slightly in pre-market trading.

On the earnings side, JPM’s Q3 tally of $2.92 came in way above the average estimate of $2.23, while revenue of $29.94 billion was about $1 billion more than analysts had expected. To double profits from the previous quarter is amazing. Revenue was down year over year, but not by much.

One thing many had expected was strong results from JPM’s trading business, and those didn’t disappoint. Fixed-income trading revenue rose 29% and stock trading revenue rose 32%. Not bad at all, and a reflection of continued volatility in the market that’s likely to help all the big investment banks.

The most surprising news was JPM setting aside just $611 million for possible loan losses, down from about $9 billion last quarter. The total size of those reserves still rounds out to $34 billion, CEO Jamie Dimon pointed out in the press release, and he cited “significant economic uncertainty and a broad range of potential outcomes.”

Remember, the entire banking sector’s profits have been handicapped almost all year as they built reserves to protect themselves from loans that might go bad. For JPM to cut back so dramatically on adding to the pile arguably sends a message that one of the largest and most influential banks might see less of a credit threat. You could read this as a nice endorsement of the economy getting better, especially considering some analysts had expected JPM to raise reserves by a lot more.

Another thing to remember is JPM’s call with investors this morning, where Mr. Dimon’s observations could carry a lot of weight for the overall market. He’s one of the people investors tend to listen to closely for an overall perspective on the economy. Stay tuned.

It was also a nice quarter for Citigroup, where earnings per share of $1.40 looked good compared with analysts’ average estimate of $0.92. Revenue of $17.3 billion was down from a year ago but ahead of Wall Street’s average $17.22 billion estimate.

Trading at C was up again, and the company’s mortgage and wealth management businesses delivered good results.

More good results came from BlackRock, Inc. (NYSE:BLK), which surpassed analysts’ expectations, too. Barron’s called their earnings, “outstanding,” and earnings per share rose 29% from a year ago. That was an amazing result.

In the midst of earnings from the banks, we also got an indication of where inflation is. The Consumer Price Index (CPI) for September, released this morning, was in line with expectations—up 0.2%. This was mostly due to an increase in used car and truck sales. People are looking to buy used cars as an alternative to taking public transportation. This sort of rise in CPI probably won’t be enough to get people worried about any inflation comeback.

FAANGs Back On Center Stage, Literally For AAPL

The bank earnings are only one aspect of the corporate news flow today following a late summer and early fall when Wall Street focused more on geopolitics.

Yesterday’s late-breaking corporate news of Walt Disney Co (NYSE:DIS) announcing a reorganization received a nice round of applause from investors, who sent shares to a quick 4.5% rally after the closing bell. The DIS move is expected to give more priority to its streaming division, news reports said, pushing those units closer to the heart of the company. These have been hard times, obviously, for the company’s traditional theme park, resort, and movie businesses.

The corporate headlines continue today when AAPL hosts what it’s calling its “hi speed” event starting early in the afternoon East Coast time. Many analysts believe AAPL is going to announce a long-rumored upgrade that would allow the iPhone to connect to the new 5G wireless network that’s currently being rolled out by carriers in the United States and abroad.

It’s also expected to reveal the first major redesign of the iPhone exterior since 2017, CNBC reported. Some analysts think today represents a significant day for the company, and their optimism might have fueled some of the buying yesterday.

Optimism surged Monday as AAPL shares posted a one-month high ahead of the event, rolling up their biggest daily gains since July. Remember, though, that AAPL shares slid after the company’s last event, so beware that things could go up or down depending on how happy investors decide they are with AAPL’s new offerings. With the stock up so dramatically yesterday, there’s also the chance this could become a “buy the rumor, sell the fact” kind of situation even if investors do like what they hear from Tim Cook and company.

Today is also AMZN’s Prime Day, accompanied by sales at some of its competitors, too. One thing that might be interesting to monitor is pace of sales vs. a year ago, considering how much worse the economy is now. It’s also possibly meaningful that this Prime Day takes place a lot closer to the holidays than normal. Does that help or hinder? It’s possible that the pace of sales at AMZN and some of its huge online sales competitors this week could give investors some clues about what we might expect this holiday shopping season.

Going into Prime Day and then the holidays, there does seem to be a lot of pent-up consumer demand, according to analysts. Whether that demand extends into the last part of the year might depend on whether another round of stimulus gets approved, because all the recent layoffs aren’t exactly lifting spirits.

Back-to-Quarantine Trade Or Treatment Optimism? Maybe Both

There was plenty of spirit in the market Monday, and it was probably a combination of things. First of all, you had excitement over AAPL’s event today and AMZN’s Prime Day. The market often rallies into these.

Then there’s still hope for a fiscal stimulus and maybe not as much fear over the election. However, next week the election could start grabbing more attention.

One school of thought looks at the huge lead by the technology-packed Nasdaq (COMP) yesterday and suggests this is a resumption of the “quarantine” trade that was so popular last summer and lifted the so-called “mega-caps” like AAPL and AMZN. That argument says fall is here and winter is getting close, making people more interested in going back toward “defensive” plays in the FAANGs since those stocks seem to do well even during a shutdown. Caseloads have been rising in the U.S. and Europe lately, raising fears of a possible “second wave.”

If that’s true, it’s kind of ironic that another thing possibly playing into the market’s positive mood could be the president’s apparent quick recovery from his case of COVID-19.

While doctors tell the media that President Trump isn’t necessarily out of the woods yet, his quick release from the hospital might have helped raise hopes that treatments could be effective and that maybe people can go out and about without as much fear. Obviously, it’s way too early to base so much optimism on one person’s experience, however prominent that person is. But when investors want to be optimistic, it’s sometimes a wave that’s hard to stop.

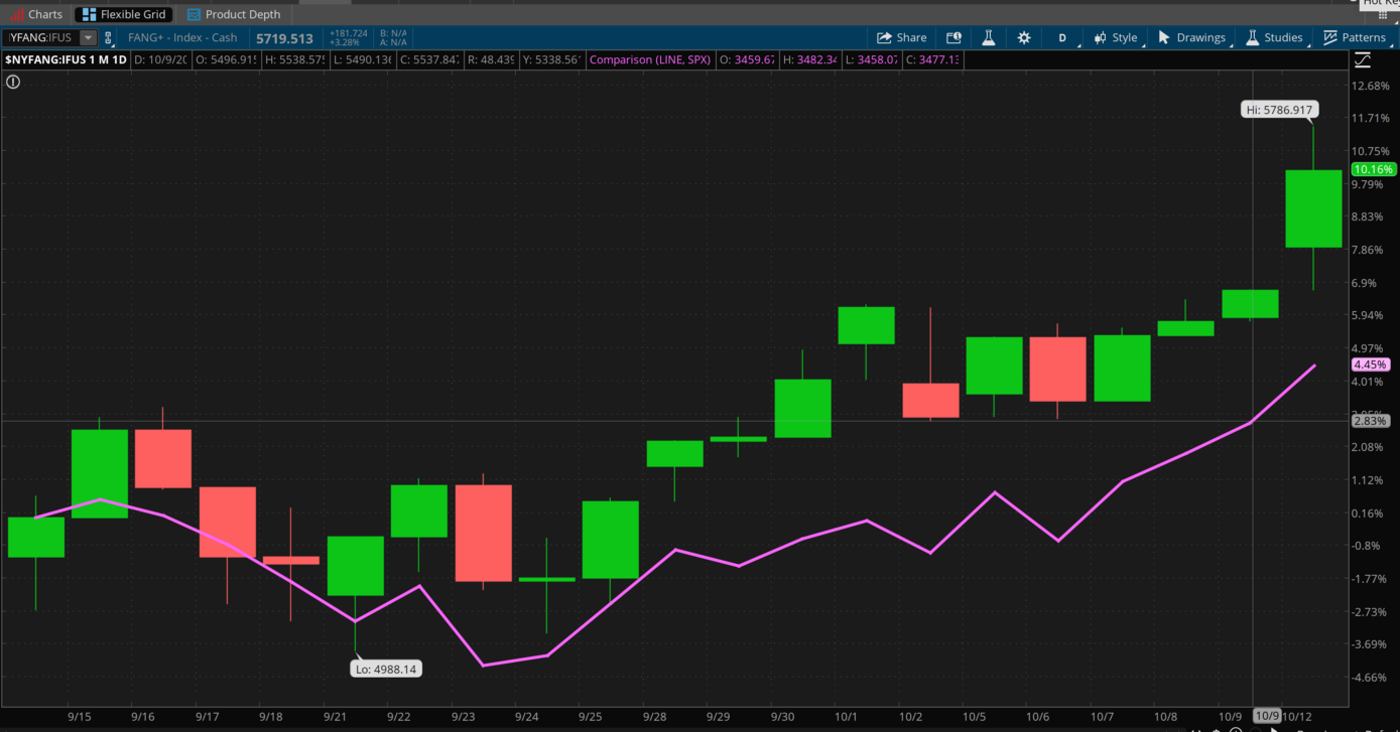

CHART OF THE DAY: AFTER FELLOWSHIP, IT’S NOW RETURN OF THE FAANG. The FAANGs ($NYFANG:IFUS—candlestick) had spent some time over the last month basically walking in place with the S&P 500 Index (SPX—purple line) or even falling below. Over the last week, however, and especially the last two or three sessions, the FAANGs have pulled out ahead of the broader market once again. Data sources: S&P Dow Jones Indices, Nasdaq. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Advance Notice: A “breadth thrust” might sound like some sort of exotic swim stroke, but it’s actually a bullish stock market term and it’s happening right now. At least that’s according to Barron’s, which reports that the market entered this week on a breadth thrust, defined as a 10-day period where advancing stocks outnumbered decliners by at least two-to-one. This has only happened 29 times since 1990, Barron’s, said, and typically means massive buying pressure in the market.

While past isn’t precedent, when breadth thrusts have occurred, the S&P 500 has been higher a year later 96% of the time, with an average gain of 13%. The counter to this? Short interest, or bets on stocks to fall, rose in both the New York Stock Exchange (NYSE) and Nasdaq exchange last month. So basically—as the old joke goes—we might have a humidifier and a dehumidifier fighting it out in the same room.

Nearing Highs: Monday’s S&P 500 Index (SPX) close of 3534 was the best since the Sept. 1 close of 3580. That was an area that seemed to trigger a lot of selling back in early September, so we’ll see if the SPX can find a way to consolidate this rise above 3500. The major moving averages people follow are now well below current SPX levels.

The Nasdaq (COMP) is also nearing its late summer peaks with yesterday’s 2.5% rally. The massive buying pushed the index well above 11,500, an area some analysts had seen as one that had triggered selling in the past. This could be a key test of whether COMP has staying power above that level.

AAPL, which we pointed out yesterday had been outperformed by the SPX recently, seemed like it was trying to make up for that all in a single day. In fact, almost every FAANG stock outperformed on Monday.

Taking a Step Back: As an individual investor, remember not to get overpowered by day-to-day market developments like yesterday’s rally. Leaping into stocks based on headlines is never a good idea, and neither is trying to time individual stocks or sectors. If you’re considering getting in, think about going in a little at a time.

Also, keep an eye on your portfolio. This rally has taken us back almost to the late-summer highs. It’s possible that’s stretched your stock market allocation beyond where you’d planned, in which case it’s never a bad idea to consider readjusting if necessary to bring it back.

While you could characterize Monday’s trading as more of a Tech comeback (and no one day is ever a trend), it’s also worth pointing out that Financials had a pretty decent opening round this week, rising more than 1%. This could suggest investor optimism going into earnings season. As noted here yesterday, the big banks are expected to see a nice bounce in Q3 earnings from where they were in Q2, though year-over-year numbers are seen falling pretty sharply for most of the sector.

Financials might have gotten an extra boost yesterday from the fact that it was a holiday (Columbus Day), bringing some thinner trade. The lower volume might have helped push things up.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Daniel Eledut on Unsplash

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.