After a dull Monday, investors awake this morning to a couple of big news items. That being said, both the consumer price index (CPI) and a pause in the use of Johnson & Johnson’s JNJ Covid vaccine seem to be having a muted impact on the market.

We’ll get to the JNJ vaccine withdrawal, but first a look at CPI: It came in at 0.6% for March, up from 0.4% in February and just a bit above analysts’ average estimate of 0.5%. The fact that it’s up isn’t too surprising considering all the inflation warnings from the Fed lately, but it’s good to see it’s only a little above expectations. That’s in contrast to last Friday’s producer price index, which came in way, way, above expectations. Maybe this will settle inflation fears a bit.

The other big news is the U.S. Food and Drug Administration’s (FDA) decision to temporarily pause use of JNJ’s Covid vaccine due to a handful of blood clots. This isn’t great news, obviously, but it’s nothing people need to go crazy over. We had good momentum with vaccinations heading into summer, and this might slow the momentum, but the other two vaccines are still working well.

Vaccine Pause Hits Reopening Shares

Also, people shouldn’t think of vaccines as a simple product without potential problems. No one knows yet if these blood clots are a game changer for the JNJ vaccine, but it isn’t surprising that a complication got reported, simply because vaccines aren’t widgets. Like any medical product, they’re complex and can have different effects on different people.

Hopefully this gets resolved quickly and the JNJ vaccine comes back. It’s a handful of cases (six cases after 6.8 million vaccinations) and the FDA said it acted “out of an abundance of caution.” It’s unclear how long it might take to get to the bottom of this, but the other vaccines were already being used millions of times a day in the U.S., and that continues. The FDA may want to examine more data before allowing JNJ to come back, but in a worst-case scenario it’s off the market for an extended period, putting more pressure on supplies of the other vaccines.

The JNJ pause could put some pressure on some of the “reopening” stocks and sectors until things get sorted out. Already this morning we’re seeing shares of airlines, casinos, and cruise lines turning lower in pre-market trading. An FDA press conference scheduled for 10 a.m. ET today might grab Wall Street’s attention.

Though reopening shares start the day under pressure, a new JP Morgan Chase & Co. JPM note suggests the economy could fully reopen by July 4. Whether this JNJ development affects that timeline is unclear, but it’s nice to think JPM might be right.

Meanwhile, volatility remains light and Bitcoin is now above $62,000. The Cboe Volatility Index (VIX) is up, but still below 17.5, which is amazing when you remember how long it spent above 50 last year.

Unless there’s big news out of the FDA press conference, trading could be pretty slow today as investors await tomorrow’s onslaught of big bank earnings.

Summer Of 2020 Revisited?

Nope, you’re not on a time machine back to last summer. Those really were NVIDIA Corporation NVDA and Tesla Inc TSLA rolling up big gains yesterday while this year’s “reopening” darlings like airlines, energy companies, and entertainment firms took a back seat. This was before today’s JNJ vaccine news, remember.

Both NVDA and TSLA rallied on specific news, with TSLA benefiting from an analyst upgrade while NVDA raised its Q1 revenue guidance and introduced several new products, which actually might have weighed on shares of some of its competitors including Intel Corporation INTC and Advanced Micro Devices, Inc. AMD.

NVDA and TSLA formed the vanguard Monday, but for the most part stocks marched in place as investors seemed to stay on the sidelines waiting for earnings.

It all starts tomorrow when we hear from JPMorgan Chase & Co. JPM, Goldman Sachs Group Inc GS, and Wells Fargo & Co WFC. For the first time in a while, the big banks have a tailwind and investors can focus more on traditional bank functions and less on the industry’s efforts to bail out the floodwaters. The 10-year yield is much higher than it was six months ago, so they can make more on the spread and that should go right to the bottom line.

Beyond that, trading is an important part of many bank businesses (especially some of the big Wall Street sluggers like JPM and GS), and they possibly saw benefits in their bond trading during Q1 thanks to opportunities there. As always, investors should consider focusing on the separate fortunes of equities and fixed income trading, where there’s often bifurcation.

Heading into earnings season, FactSet projected overall S&P 500 Financial Sector (IXM) earnings to rise 78.7% year-over-year in Q1, so things are definitely looking up. In fact, the average Wall Street Financial earnings forecast has risen pretty substantially even from just a month ago.

The banking sector has sputtered a bit lately after a great start to the year. Energy also slowed its pace a bit. Some analysts see this as a temporary slowdown while the Treasury market continues to consolidate. If Q1 earnings and coming economic data shape up as strong as many Wall Street watchers are starting to think they will, 10-year yields could start to rise again and lift the so-called “cyclicals” like Financials and Energy that tend to do better in a recovering economy.

Pandemic Provides The Backdrop

There’s always a caveat, and here’s one: The Covid situation isn’t really retreating much. Average caseloads are still rising despite the great vaccine progress. Even Fed Chairman Jerome Powell expressed caution over the weekend, telling “60 Minutes” that he’s concerned about the recent case spike and its possible impact on the economy. And of course, there was today’s bad news about the JNJ vaccine being paused due to blood clots.

If cases keep climbing, watch the other data like hospitalizations and deaths carefully. They tend to be lagging indicators, and if they stay relatively tame it could mean the vaccinations are protecting some of the most vulnerable people.

Leaving Covid behind for the moment, FactSet pegs overall S&P 500 earnings to rise 24.5% in Q1, led by Consumer Discretionary, Financials, Materials, and Info Tech. Energy and Industrials are the only sectors analysts see in the red with their Q1 earnings results, and those are also two of the three S&P sectors expected to have falling revenue, too.

Typically, analysts get too conservative with their estimates ahead of earnings season, so FactSet factors that in and says it’s more likely actual earnings will rise 28% when all is said and done. That would be the highest earnings growth in more than 10 years. At the high end, FactSet estimated earnings could grow as much as 37.6% in Q1.

Margin Call? Not Yet

Some people wonder if margins might start eroding, possibly due to rising costs like we saw in the producer price index (PPI) last week. So far, no sign of that. S&P Global expects margins to rise this year and next.

Of course, the Fed keeps telling everyone that any price growth we see here is probably temporary, and easy comparisons with soft year-ago inflation could over-dramatize how much things are actually going up. By later in 2021, it might be easier to get a sense not only of how transient or non-transient this inflationary pressure is, but also whether the Biden administration has the ability to push through a corporate tax increase, which is another thing that could potentially hurt margins.

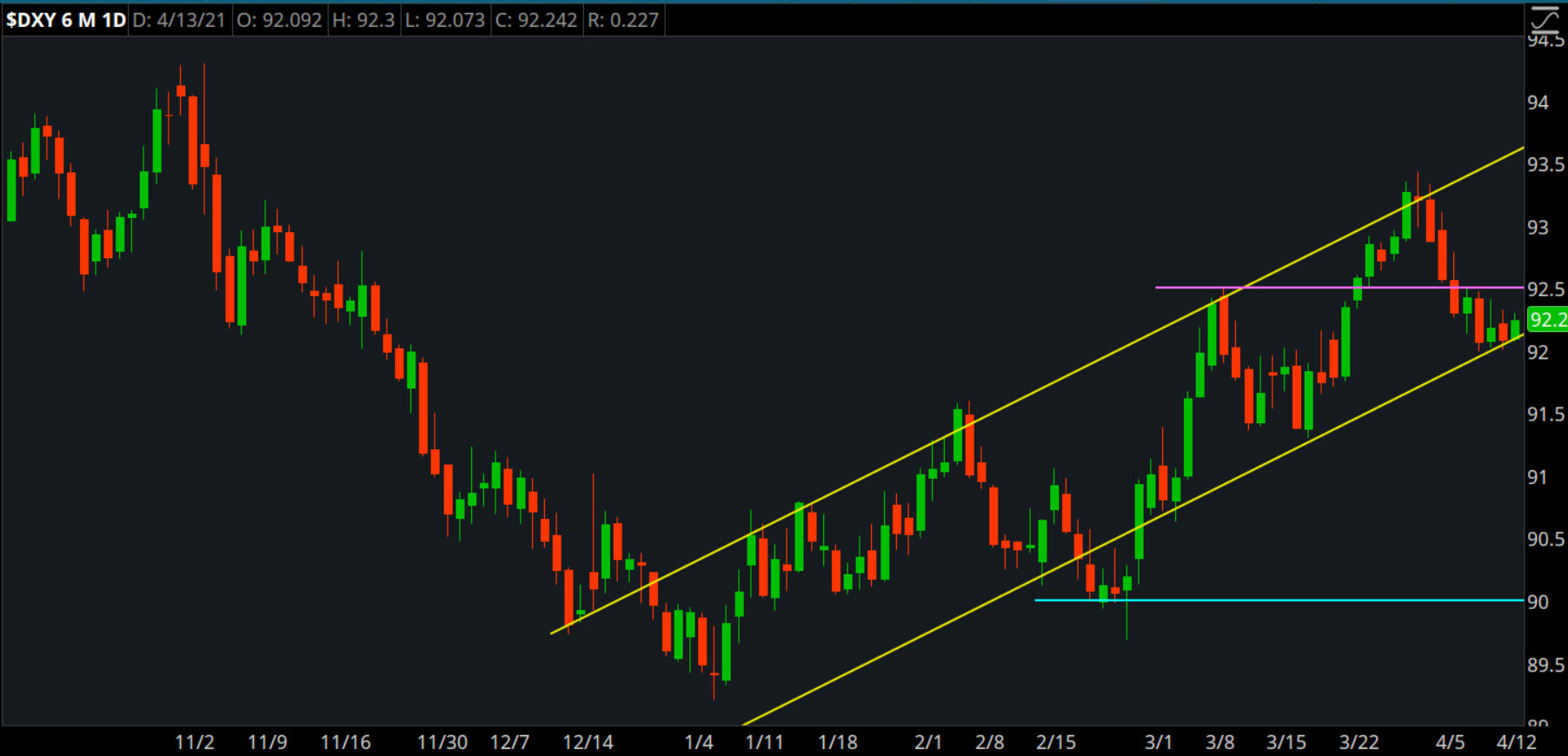

CHART OF THE DAY: CAN THE U.S. DOLLAR HANG ON? The U.S. Dollar Index ($DXY—candlestick) has generally remained within its upward channel (yellow lines) since the beginning of the year. Can it maintain this move as it skirts its support level once again? Although $DXY is moving up today, it doesn’t mean it can’t break below the lower channel. It could still go either way—retest the 90 level (blue line), which was the Feb low or break above 92.5 (purple line), the early March high, and resume its move within the channel. Data source: ICE Data Services. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

The Dollar’s Dilemma: While the U.S. Dollar Index ($DXY) is still trading within its uptrend channel (see chart above) since Jan. of this year, it’s hard to ignore that it is trading close to a critical support level. If it does break below the lower channel, which at the moment sits at around 92.10, we could see $DXY test the 90 level, the low it hit at the end of Feb, or it could continue moving within its upward channel.

When it comes to the U.S. dollar, a lot also depends on economic fundamentals such as actions taken by the Fed and other central banks. Are they going to be more dovish or hawkish, relatively speaking? Since the U.S. dollar trades against other currencies, it’s a good idea to know where other central banks stand with respect to interest rate decisions. It can shed some light on global economic growth outlook. Another piece of economic data to keep an eye on this week: retail sales and inflation. Both could have an impact on the U.S. dollar.

Bank Earnings, Net Margin, and the Rate Watch: As big banks prepare to open their Q1 books this week, it’s important to focus on recent moves in interest rates. On the face of it, the rise in long rates—particularly when accompanied by dovish talk from the Fed about leaving short rates at the zero bound—is the optimal setup for the banks. And sure enough, over the past three months the yield spread between the 3-month Treasury and the 10-year Treasury widened by over 80 basis points to its highest level in four years—a positive development for an industry that’s business model is centered on borrowing (and paying deposits on) the short end and lending on the long end.

But like most things economic, there’s always “the other hand.” A nominal rise in mortgage rates, all else equal, should pad the bottom line of lenders. But when you consider the amount of exuberance in the housing market—think Lennar Corporation LEN, KB Home KBH and other home builders that have seen shares blow through all-time highs in the middle of a pandemic—it’s possible that rising mortgage rates could eventually eat into the balance sheets of homeowners and small businesses, and to the housing market in general. Anyone who was around for the last recession knows what can happen to banks when a frothy housing market turns south. It’s another reminder to keep a close eye on bank earnings, as banks tend to be tied into the rest of the economy. For now, however, banks head into earnings season with the sun shining brightly.

When Things Look Good, People Worry: A couple things to consider here as the market finishes up its “breather” ahead of earnings: First, there’s concern among some analysts that a couple of economic indicators like manufacturing growth and consumer confidence may be at “toppy” levels. Manufacturing, for instance, is at multi-decade highs.

While that may be true, you can’t say for sure that there’s anything magical about current numbers just because they match, say, a level not seen since 1984. The numbers don’t know or care what happened back in the first Reagan term. They just do what they do. A fresh University of Michigan sentiment report Friday could give more insight into any perceived “toppiness.”

Also, volatility has gotten so low recently, with the VIX finishing below 17 again yesterday, that people are starting to worry it might go up again. This sounds like traditional “wall of worry” talk and another sign that this rally just doesn’t get much respect.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Lukas Krasa on Unsplash

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.