They say a rising tide lifts all boats, and that’s partially true for the U.S. banking industry here at the start of earnings season. Increasing bond yields and a recovering economy, along with a healthy dose of consumer-empowering fiscal stimulus, can help cover up a lot of other potential problems.

With that in mind, remember that even though all the big banks sail in the same waters, they’re not all piloting the exact same yachts. Some, like JPMorgan Chase & Co. JPM and Goldman Sachs Group Inc GS, which also report this week, appear to be doing swimmingly.

Others, like Bank of America Corp BAC and Citigroup Inc C, both expected to report tomorrow, have enjoyed strong share performances but still struggle with some issues investors look for them to address, and might see overall revenue decline.

With BAC, trading revenue is under a microscope after a miss in Q4, while C continues to deal with regulatory issues and recently took on a new CEO. BAC and C both are straight ahead Thursday, and Morgan Stanley MS, the last of the big banks to report this week, is expected to open its books on Friday.

Heading into earnings season, FactSet projected overall S&P 500 Financial Sector (IXM) earnings to rise 78.7% year-over-year in Q1, so things are definitely looking up. In fact, the average Wall Street Financial earnings forecast has risen pretty substantially even from just a month ago.

Before getting down to the fundamentals of each company, it’s important to address an issue that recently came up and may have implications for the entire industry.

- Massive Demand & Disruptive Potential – Boxabl has received interest for over 190,000 homes, positioning itself as a major disruptor in the housing market.

- Revolutionary Manufacturing Approach – Inspired by Henry Ford’s assembly line, Boxabl’s foldable tiny homes are designed for high-efficiency production, making homeownership more accessible.

- Affordable Investment Opportunity – With homes priced at $60,000, Boxabl is raising $1 billion to scale production, offering investors a chance to own a stake in its growth.

Warning Sign Flashes

Just when you thought it was safe to go back to the bank, a virus appeared out of nowhere and hurt some major financial companies this month.

Not the virus we’re all focusing on, but an old threat to banking: Too much leverage. When a major hedge fund recently stumbled, pressuring shares of banks connected to it (mainly European ones), investors received a timely reminder that big banks face more possible tripwires than simply Covid and historically low interest rates.

In the current era where stocks are at all-time highs and bonds have been losing some of their mojo, many people are seeking alternative investments they hope can provide better returns. Banks and their strategists can sometimes get caught up in the frenzy, but if they aren’t careful monitoring their balance sheets it can spell risk for both them and their investors.

Luckily for most investors in major U.S. banks, that ugly reminder of the risk likely had little-to-no impact on performance in Q1. Though shares of GS and MS initially recoiled on the news, it appears U.S. banks did a good job of protecting themselves from any fallout. That wasn’t necessarily true for Credit Suisse Group AG CS, which got caught up in the hedge fund mess and said it will have to take a $4.7 billion charge on the issue.

Stress Testing Next As Dividends, Buybacks Hang On Results

That doesn’t mean U.S. banks are necessarily immune to making bad decisions, as many of us probably remember from the 2008 crash. Remember to keep a close eye on the Fed’s “stress tests” of U.S. banks for insight into how these companies are managing risk and how prepared they might be for any kind of major negative event.

The Fed said recently that big banks will be allowed to resume normal levels of dividend payouts and share repurchases as of June 30, assuming they pass this year’s stress tests. These payouts had been restricted during Covid, when worries cropped up across the industry around credit risk. Remember, stress tests “evaluate the resilience of large banks by estimating their losses, revenue and capital levels under hypothetical scenarios over nine future quarters,” according to the Fed.

“The banking system continues to be a source of strength and returning to our normal framework after this year’s stress test will preserve that strength,” said Randal Quarles, the Fed’s vice chairman of supervision, according to recent media reports.

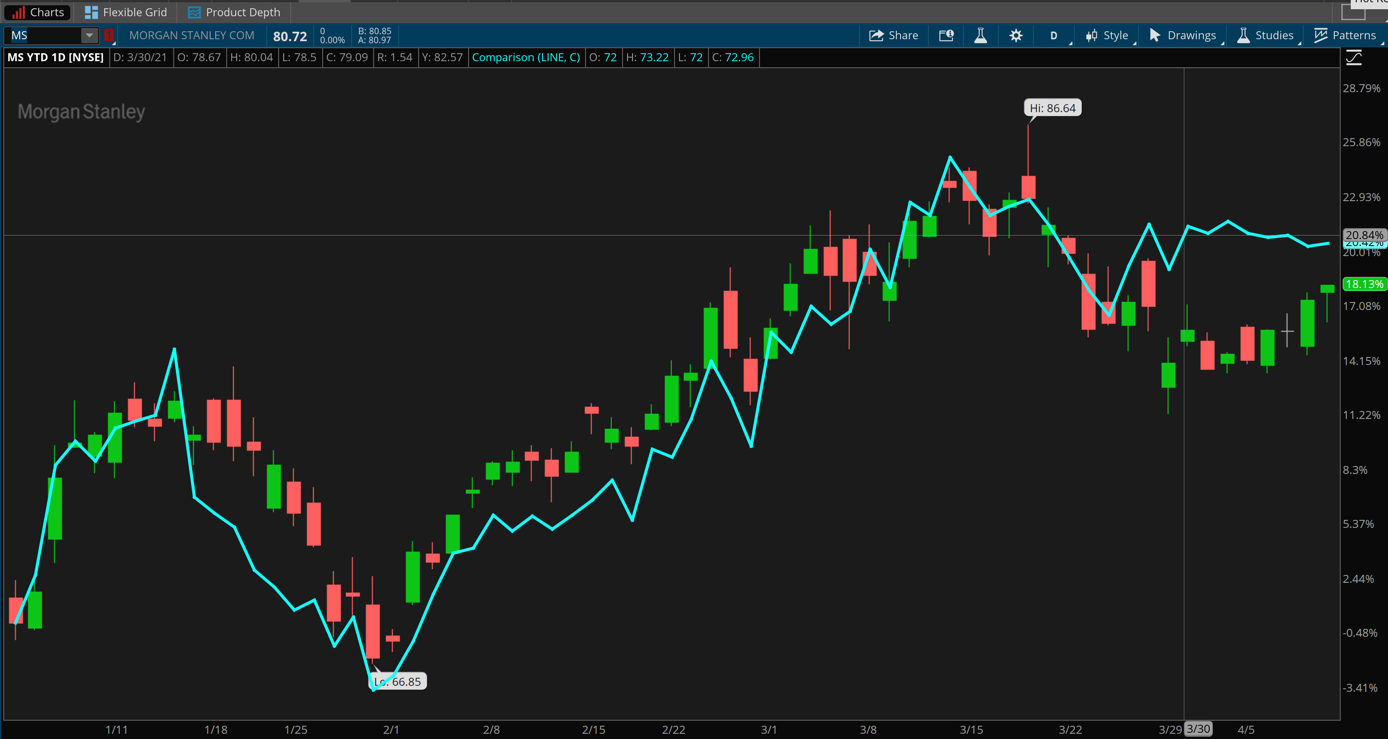

FIGURE 1: LEVELING OFF. After a blistering rally in Q1, shares of Morgan Stanley (MS—candlestick) and Citigroup (C—blue line) both lost ground and flat-lined over the last few weeks. This could reflect some investors taking profit in the so-called “value” trade that characterized the market over the first three months of 2021. Data Source: NYSE. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Bank Of America Earnings And Options Activity

Bank of America is expected to report adjusted EPS of $0.66 vs. $0.4 in the prior-year quarter, on revenue of $22.13 billion, according to third-party consensus analyst estimates. Revenue is expected to fall 3.4% year-over-year.

Options traders have priced in a 2.6% stock move in either direction around the coming earnings release, according to the Market Maker Move indicator. Implied volatility is near its lowest level in the past 52 weeks, at the 2nd percentile as of Wednesday morning.

Looking at the Apr 16 expiration, put options have been relatively active, with concentrations at the 35 and 38 strikes. Calls have been active at the 41 and 42 strikes.

Note: Call options represent the right, but not the obligation, to buy the underlying security at a predetermined price over a set period of time. Put options represent the right, but not the obligation to sell the underlying security at a predetermined price over a set period of time.

Bank Of America Seen As A Consumer Barometer

Recent consumer confidence reports approached or exceeded all-time highs. That’s possibly good news for investors in BAC, which derives the highest amount of its revenue from consumer banking.

Last earnings season we noted it would be helpful to get a sense of how banks’ commercial loan businesses are doing coming out of the late 2020 Covid shutdowns. The economy has been slowly reopening since then, and Q1 earnings offer a chance for investors to monitor the loan books when banks like BAC report.

Keep an eye on BAC’s business lines including credit cards, car loans, small business loans, mortgage books, loans to industry, and personal loans. It’s important not to look at this as a single homogenous pile, but to sort it out and see how different loan books are doing to get a sense of how various aspects of the economy are performing.

Also, BAC is often thought of as the big bank most exposed to interest rates due to its large base of deposits, so it probably has more to gain (or lose) than some of its rivals based on where rates go. For many months in 2020, being exposed to rates was a handicap for BAC. For instance, the company’s revenue and profit both fell in Q4 from a year earlier. Revenue actually came up short of analysts’ estimates that quarter, which helped weigh on the bank’s shares after it reported in January.

Since then, BAC shares have marched steadily higher, probably with a helping hand from the relentless rise in the 10-year Treasury yield. That benchmark began 2021 near 0.9% and recently traded near 1.68%, with a Q1 rise that was the largest for any quarter in five years.

Another thing that probably points in BAC’s favor as it gets ready to report is the recent round of government stimulus. Many consumers have received $2,000 in checks from Washington over the last three months or so, and that could be leading to more people deciding to make big purchases that they can help finance using the services of banks like BAC. The housing market sizzled in Q1, and other economic data, including job growth, may also work to BAC’s advantage.

One thing to watch in Q1 is the trading business at BAC. Fixed income revenue came up short of Wall Street’s estimates in Q4, but the environment looked pretty good for that sort of activity in Q1. BAC bulls are probably hoping the company caught the wave in time to recover.

Citigroup Earnings And Options Activity

Citigroup is expected to report adjusted earnings of $2.57, vs. $1.05 in the prior-year quarter, on revenue of $18.82 billion, according to third-party consensus analyst estimates. Revenue is expected to be down 9.2% year-over-year.

Options traders have priced in a 2.6% stock move in either direction around the coming earnings release, according to the Market Maker Move indicator. Implied volatility was at its lowest level of the past 52 weeks as of Wednesday morning.

Looking at the Apr 16 expiration, put options have been most active at the 70 strike, but more activity has been seen to the upside, with the highest concentrations at the 75- and 76-strike calls.

Did Credit Cards And SPACs Lift Citigroup’s Q1?

Almost everything you read above about BAC also applies to C, which is often considered a good consumer barometer thanks to its huge credit card business. If consumers were happier in Q1, and they seemed to be, that could be a driving factor in C’s potential earnings success.

Consumers don’t tend to spend if they aren’t employed, so the amazing jump in March job creation to over 900,000 would seem like great news for a company like C. However, job growth was a bit slow over the December through February period, and we continue to see initial weekly jobless claims running about 2.5 times as high as they were before Covid. As Fed Chairman Jerome Powell and other Fed officials keep telling us, there’s a long way to go with the economy. That means companies like BAC and C aren’t out of the woods yet.

With C, it also helps to understand what’s going on in Europe, because its loan book is heavily exposed to that economy. The euro has been trending up, which may be a good sign of better growth across the Atlantic. However, shutdowns in France and Italy along with growing Covid caseloads in Germany so far this year don’t seem to bode as well.

The U.S. 10-year Treasury yield recently traded at a 194-basis point premium to the benchmark 10-year German bund yield. The bund yield is up about 48% year-to-date, but the 10-year Treasury yield is up about 80%, so that premium has continued to build and might be a factor to consider as C reports.

With C recently expanding its initial public offerings (IPO) business, that aspect of the market is another one to look at. Q4 was a monster for IPOs, but Q1 wasn’t quite as packed with big debuts. Still, the year ahead looks like it could pick up steam, and C may offer some thoughts on coming developments in its earnings call.

There’s IPOs and then there’s special purpose acquisition companies (SPACS), a field where C is one of the dominant players. SPACs have been around for a long time, but they’ve become more popular in recent days after several high-profile SPAC success stories. Technically, though, a SPAC isn’t an alternative to an IPO or DPO. In general, investors access SPACs upon (or after) a public offering such as an IPO. It wouldn’t be surprising to hear C’s executives get asked about the SPAC situation when they take to the phones on Thursday.

Last time out, C disappointed investors by missing Wall Street’s revenue expectations and the stock sank more than 6%. The company made headlines recently when its new CEO Jane Fraser said she’s taking measures to improve work/life balance for employees. However, Fraser has a big job ahead of her, beyond that, as the bank still has regulatory issues it’s dealing with and is under pressure to improve returns.

Morgan Stanley Earnings And Options Activity

Morgan Stanley is expected to report adjusted earnings of $1.70, vs. $1.01 in the prior-year quarter, on revenue of $13.98 billion, according to third-party consensus analyst estimates. Revenue is expected to be up 47.3% year-over-year.

Options traders have priced in a 3.1% stock move in either direction around the coming earnings release, according to the Market Maker Move indicator. As of Wednesday morning, implied volatility was at its lowest level of the past 52 weeks.

Looking at the Apr 16 expiration, activity in both call and put options has been muted, but with some concentration in the 75-strike puts and the 85- and 90-strike calls.

Capital Markets Strength Seen Helping Morgan Stanley

Last time out in Q4, Morgan Stanley easily beat analysts’ revenue and earnings estimates thanks in part to a strong wealth management environment and lots of action in the capital markets.

It’s hard to really say what’s changed since then for the company, since both those trends likely continued in the Q1 earnings period. One thing to consider: MS is usually the last of the “significant six” big banks reporting, meaning investors may have its performance under a microscope to see if it did as well as other banks closely linked to the capital markets like JPM and GS.

As always, it’s important to keep an eye on MS’s investment banking revenue, which reached $2.3 billion in Q4. Wealth Management is another huge division for MS, and so is Equities Trading.

When MS reported Q4 results back in January, it kept its long-term goals largely unchanged, saying returns on tangible common equity will be 17% or higher. One question going into Q1 earnings is whether this number might go up or stay the same.

Another thing to listen for on the earnings call is any update on the company’s move toward more focus on money management and retail clients after a major acquisition last year. How is the integration going, and does MS have any other acquisitions up its sleeve?

TD Ameritrade® commentary for educational purposes only. Member SIPC. Options involve risks and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options.

Photo by Eduardo Soares on Unsplash

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.