The market has seen option volatility (as measured by the VIX) as low as 16 and as high as 27 in the past two weeks. Rising or declining implied volatility can affect the chances of success in an option trade. In options there are more ways to trade than outright calls and puts. Defined risk spreads can be used to mitigate or even take advantage of potential moves in option volatility when expressing directional or non-directional views. Below are some options concepts, like how the expected move can translate current levels of implied volatility into actionable information, and examples of options spreads that can be a part of a trader’s arsenal.

Expected Moves SPY, QQQ, AAPL And Tesla

First, the expected move. The expected move is the amount that options traders believe a stock price will move up or down. It can serve as a quick way to see where real-money option traders are pricing the future movement of a stock. That consensus is derived from the price (or implied volatility) of at-the-money options. An easy way to think about it is if the stock moves inside the expected move, options were overpriced, and if the stock moves outside the expected move, options were underpriced. When implied volatility increases, so does the expected move.

Knowing the expected move before making a trade can be incredibly powerful, regardless of whether you’re using stock or options to make your trade. It can also be used as a basis for starting strike selection, allowing a trader the ability to translate real-time implied volatility into potential option spreads. Options AI puts the expected move at the center of its trading experience.

Below is an expected move comparison (via the Options AI calculator) for the SPY, QQQ, AAPL and TSLA. Note Apple’s expected move close to QQQ while Tesla’s is much greater:

- SPY, options are pricing about a 2% move for the next seven days and about 4% for the next month.

- QQQ options are pricing about a 2.5% move for the next seven days and about 5% for the next month.

- Tesla is pricing about a 3.5% move for the next week and nearly 12% for the next month.

- Apple is pricing about a 1.6% move for the next seven days, and about 5.5% for the next month.

Below we’ll show how the expected move can be used to assist in strike selection for multiple trade types using the names above. The directional and non-directional strategies can be used for any of these stocks or any other stocks and are shown here merely as examples.

Apple Call Alternatives

The risk of buying outright options during a period of higher implied volatility can be partially mitigated via debit spreads.

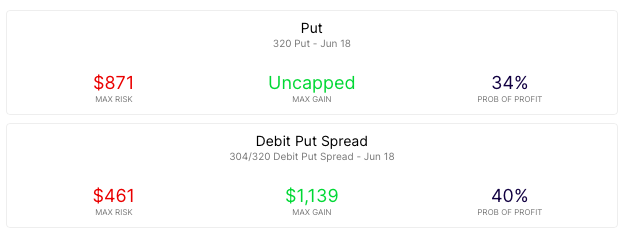

At the time of writing, buying an Apple (June 18th) $145 Call costs around $3.50, or $350 in premium. In order for the Call to be profitable on June 18th, the stock would need to be above $148.50.

Now, let’s take a scenario where a trader wants to position for a move higher but with a breakeven closer to where the stock is currently trading. One way to do that is to use the 5.5% expected move to guide strike selection, creating a defined risk option spread. One that lowers the breakeven when compared to an outright out-of-the-money or at-the-money Call and lessening exposure to option premium.

Using the Options AI platform, we’ll look below at some alternative strategies that have been generated with the expected move guiding strike selection. We can start by directly comparing the 125 call to a +125/-130 call spread.

.2021-05-19%2012_04_30.gif)

The 125/130 Debit Call Spread lowers the cost of the 125 call, from around $350 to $200 by simultaneously selling a call around the expected move level. In turn, this brings down the break-even level to around $147, vs $148.40 for the 125 call outright, while increasing the probability of profit (by lowering the break-even level required at expiration) from around 34% to 40% The trader has also reduced their overall exposure to elevated volatility in the options versus an outright call. Less capital is at risk, and a lesser move higher is needed in order to at least breakeven.

Aside from the additional potential risks of option spreads (such as early assignment and liquidity), it is important to note that a spread caps potential profits (if the stock moves beyond $130). Those that are bearish in Apple can use the same debit spread strategy in the form of a put spread to the bearish consensus.

QQQ Put Alternatives

If a trader is interested in positioning for a move lower in the stock, or even hedging, the bearish consensus could also be used for the initial trade setup. Again, using the Options AI platform, with June 18th expiry in QQQ:

The +320/-304 Debit Put Spread creates a breakeven around $5 dollar lower in the stock, vs about $9 in the 320 put. The Debit Put Spread is able to get that breakeven closer to where the stock is currently trading. The same strategy can be implemented for those looking to position for upside in the QQQ, via a debit call spread.

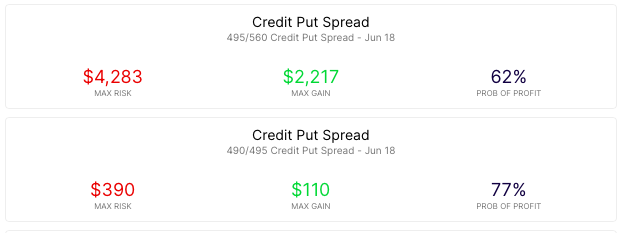

Tesla Credit Put or Call Spreads

Credit Spreads are another example. Whereas calls, puts and debit spreads position for something to happen (a move in the stock), Credit Spreads can best be thought of as positioning against something happening. They can be used to express a directional view, for instance being bullish by selling a credit put spread, or they can express a non-directional view, by selling a move, and therefore implied volatility, entirely.

This trade typically risks more to make less, but instead of requiring the stock to move in the direction of the traders’ view, it is profitable if the stock simply doesn’t move against it.

Below are examples of bullish Credit Put Spreads in Tesla TSLA, one at-the-money, the other out-of-the-money. Both trades use the bearish expected move to select the 393 put strike, via Options AI:

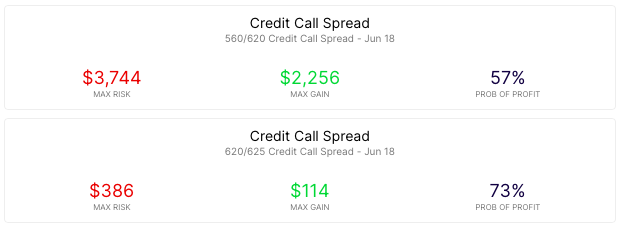

And bearish credit call spreads, using the 620 strike:

SPY Iron Condor – Selling to the bears and the bulls

Out of the money Credit Put and Call spreads can even be combined to form an Iron Condor, a credit spread that looks to make money if the stock stays within a range:

.2021-05-19%2013_05_36.gif)

With SPY around $408 the trade above uses the bullish and bearish consensus (as based on real-time implied volatility) to generate a 391/392/424/425 Iron Condor. It sees maximum profit if SPY is anywhere between $392 and $424 on June 18th expiration. It is max loss above $425 or below $391, beyond the expected move options are pricing. A move beyond the expected move would mean that options were underpriced at their current implied volatility.

Options AI puts the expected move at the heart of its trading platform. It allows traders to quickly generate and compare more ways to trade, by entering an informed price target or using the expected move for initial strike selection.

Options AI provides a couple of free tools like an expected move calculator, as well as an earnings calendar with expected moves. More education on expected moves and spread trading can be found at Learn / Options AI.

Image Sourced from Pixabay

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.