Source: CME Group

AT-A-GLANCE

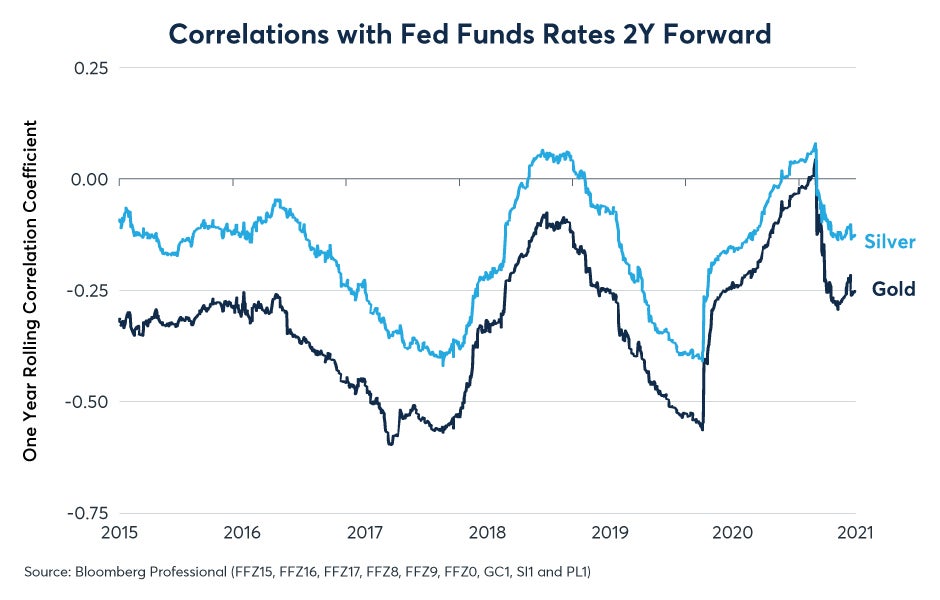

- Gold shows a consistent negative correlation with changes in expected Fed funds rates

- Expectations for falling rates boosted gold from mid-2018 to mid-2020

- Since mid-2020, expectations that the Fed might tighten policy appear to have held gold back

- Gold has been a major underperformer among risky assets despite surging inflation

Gold has underperformed many other investments since the pandemic began. This might come as a surprise considering gold’s reputation as an inflation hedge and the U.S. consumer price index (CPI) surging to over 6% year on year in October.

From late March 2020 the S&P 500 is up over 100%, Nasdaq 100 nearly 150% higher, copper has risen nearly 120% and silver prices have nearly doubled. Meanwhile, gold prices are only about 20% higher than they were at the March 2020 low. One reason for gold’s underperformance could be that it hasn’t captured the public’s imagination like equities and cryptocurrencies have, nor has it benefitted from the boom in the global manufacturing activity in the way that many industrial metals have. This may well be the case, but they are not the only explanation. An alternative reasoning is that investors could potentially see gold as a de facto currency, but one that pays no interest on deposits. As such, as anticipated future deposit rates move up or down, gold tends to move in the opposite direction.

Going into the pandemic, gold was outperforming other assets, rising from the 2018 low of $1,248 per ounce to $1,505 by March 2020, and going as high as $2,097 in July 2021. During this time, other metals, equities and even cryptocurrencies were not performing particularly well.

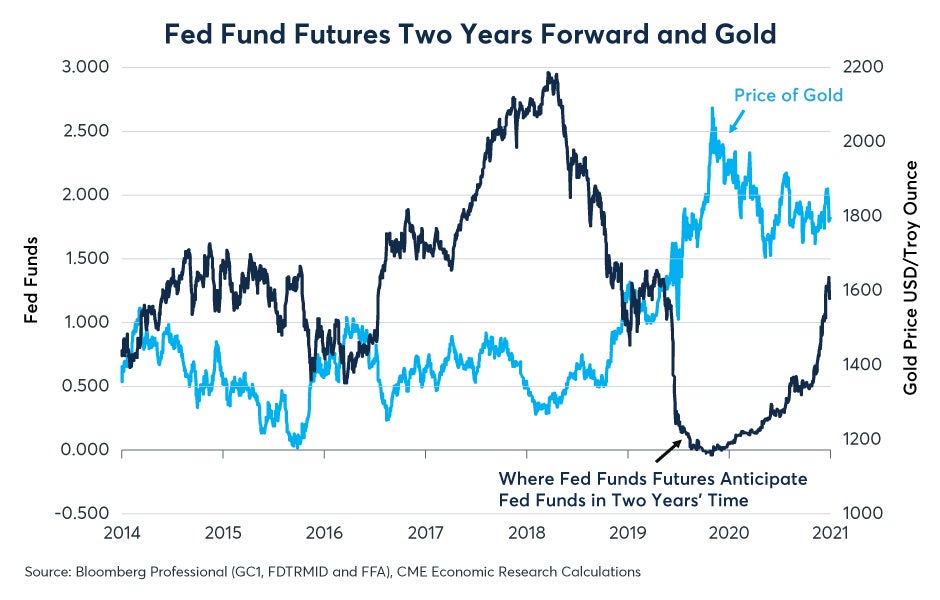

Part of the reason why gold was rallying in late 2018, 2019 and early 2020 was that the market expected the Federal Reserve (Fed) to reduce interest rates. Indeed, the Fed delivered on these expectations, cutting the Fed funds rate three times in 2019 before reducing rates to near zero and resuming quantitative easing in Q1 2020.

In Q2 and Q3 2020, as gold rose towards its all-time high, Fed funds futures even partially priced the possibility that the Fed might follow the European Central Bank (ECB) and the Bank of Japan (BoJ) into negative rates. This pricing coincided with the peak in gold prices. Since then, interest rate expectations have been moving in the other direction, slowly at first and picking up speed more recently (Figure 1). As of the end of November, Fed funds priced that the most likely scenario was for the Fed to hike rates five times over the next two years.

Figure 1: Gold Prices Held Back By Growing Expectations for Multiple Rate Hikes

The change in expectations from pricing the possibility of negative rates in the summer of 2020 to pricing 125 basis points (bps) of rate hikes by the fall of 2021 likely held back the price of gold, preventing it from rallying in line with other assets. Indeed, over the past seven years, the day-to-day change in gold prices has shown a consistent negative correlation with the day-to-day change in Fed rate expectations two years forward (Figure 2). If anything, given the sharp move in Fed expectations, it’s remarkable that gold has done as well as it has. For gold to sustain a strong rally, it might be necessary for rate hike expectations to stabilize or even moderate at first. That said, if the Fed is seen as being behind the curve by some and not doing enough to quell inflation, gold might rally even if rate rise expectations intensify further.

Figure 2: Gold Prices Have Shown Negative Correlation with Fed Rate-Hike Expectations

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the author and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

The preceding post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga. Although the piece is not and should not be construed as editorial content, the sponsored content team works to ensure that any and all information contained within is true and accurate to the best of their knowledge and research. The content was purely for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.