This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

(Thursday Market Open) Equity index futures were swinging between the positive and negative in premarket trading on Thursday. The S&P 500 futures ranged over 100 points from yesterday’s close to this morning’s action. Investors are trying to absorb the Fed’s Wednesday interest rate announcement, a trove of earnings reports, and some economic news all under the looming market volatility.

After Wednesday’s close, Tesla (NASDAQ: TSLA) reported a record profit, but investors appeared unsure if it was “record” enough because the stock bounced around in afterhours trading. The biggest issue per CEO Elon Musk is supply chains and what it might do to hurt Tesla going forward. As the provider of approximately 75% of electric vehicles sold in the United States, this could signal that the inflation issue isn’t going away any time soon.

A new theme emerging from earnings season is beating on earnings but not beating by enough. This appears to be the issue with Mastercard MA that beat on both earnings and revenue but fell nearly 2% in premarket trading.

Intel INTC, which announced better-then-expected earnings and revenue, dropped more than 3% in afterhours trading when the company’s management provided lower-than-expected forward guidance. This could be an interesting development for the semiconductors group after Texas Instruments TXN had a big beat yesterday.

Whirlpool WHR missed on revenue but was able to still report much better earnings, leading to a 0.89% rally before the bell. Blackstone BX rose 4.93% in premarket trading after reporting its best quarter ever, according to Blackstone president Jon Gray. The company beat on earnings and revenue and increased its forward guidance.

On the downside, McDonalds MCD missed on top and bottom line estimates leading to the stock falling 2.17% in premarket trading. Despite missing on earnings and revenue, MCD saw same-store sales grow from 6.58% to 7.5% with help from its new app. However, rising supply and labor costs were a drag on the company. Las Vegas Sands LVS reported a larger-than-expected loss and missed on revenue too but was up 1.54% in premarket trading after offering an upbeat projection for 2022.

After the bell, Apple AAPL will announce earnings. Obviously, this popular company will be a much watched report.

In economic news, the United States saw Gross Domestic Product (GDP) grow at 6.9% and well over analysts’ estimates. Durable goods orders came in on target and so did initial claims. S&P 500 futures traded a little higher on the news and the Cboe Market Volatility Index (VIX) slid a bit lower. The problem will likely be hanging on to any gains. Yesterday, the market destroyed a 2% gain in 90 minutes.

Eccles Shekels

The Federal Open Market Committee (FOMC) ended its two-day meeting on Wednesday with its customary interest rate decision announcement and press conference. After the December Consumer Price Index (CPI) reported inflation grew at 7.1% year over year, the market started to expect the Fed to hike the overnight rate to 0.25% in March.

In the announcement, the Fed stated that it wasn’t going to raise rates. As far as rate-hike guidance, the Fed simply reiterated what it has said before, that it would “continue to adjust as needed.” In a separate announcement, the Fed said it plans to reduce its balance sheet after it starts hiking interest rates.

During the press conference, Chair Powell was unwilling to state whether the Fed would raise rates each meeting or every other meeting and that it basically wants to keep its options open. He did clarify that the committee would defer the decision to raise the overnight rate in March at the March FOMC meeting. So, the market has been projecting three to four rate hikes in 2022, but the Fed wasn’t willing to make that commitment. However, Powell didn’t rule out any of these possibilities, nor did he rule out raising rates more than a quarter point at a time. The Fed has stuck with quarter-point adjustments for more than two decades to keep a measured approach to interest rate changes.

Stocks were volatile before and after the announcement. The S&P 500 (SPX) rallied higher and then sold off into negative territory. However, it also trimmed its losses to close just 0.15% lower on the day. The Dow Jones Industrial Average ($DJI) had another 800-point swing before closing just 0.38% lower on the day. The Nasdaq Composite ($COMP) also had major swings of its own ranging 600 points. But investors started buying technology stocks, leading the tech-heavy index to close basically flat for the day.

The 10-year Treasury yield (TNX) was relatively flat ahead of the announcement, trading around 1.785%, but rallied soon after, climbing to 1.848%, which is near its previous January highs. The Fed’s comments and rising yields pushed the dollar higher. The U.S. Dollar Index rallied 0.60%.

Crude oil prices didn’t appear to be threatened by the Fed’s plan to hike rates to take on inflation on Wednesday because it rallied more than 2.6% before the announcement. The rally resulted in a new 52-week high. However, the price of oil did pull off its high and closed at $86.98, which was still its highest close in seven years. The rally in crude also occurred despite an unexpected rise in oil inventories, according to the Energy Information Administration’s weekly crude inventory report. Higher crude inventories tend to be bearish for oil, but the Russia-Ukraine crisis appears to be overshadowing inventories.

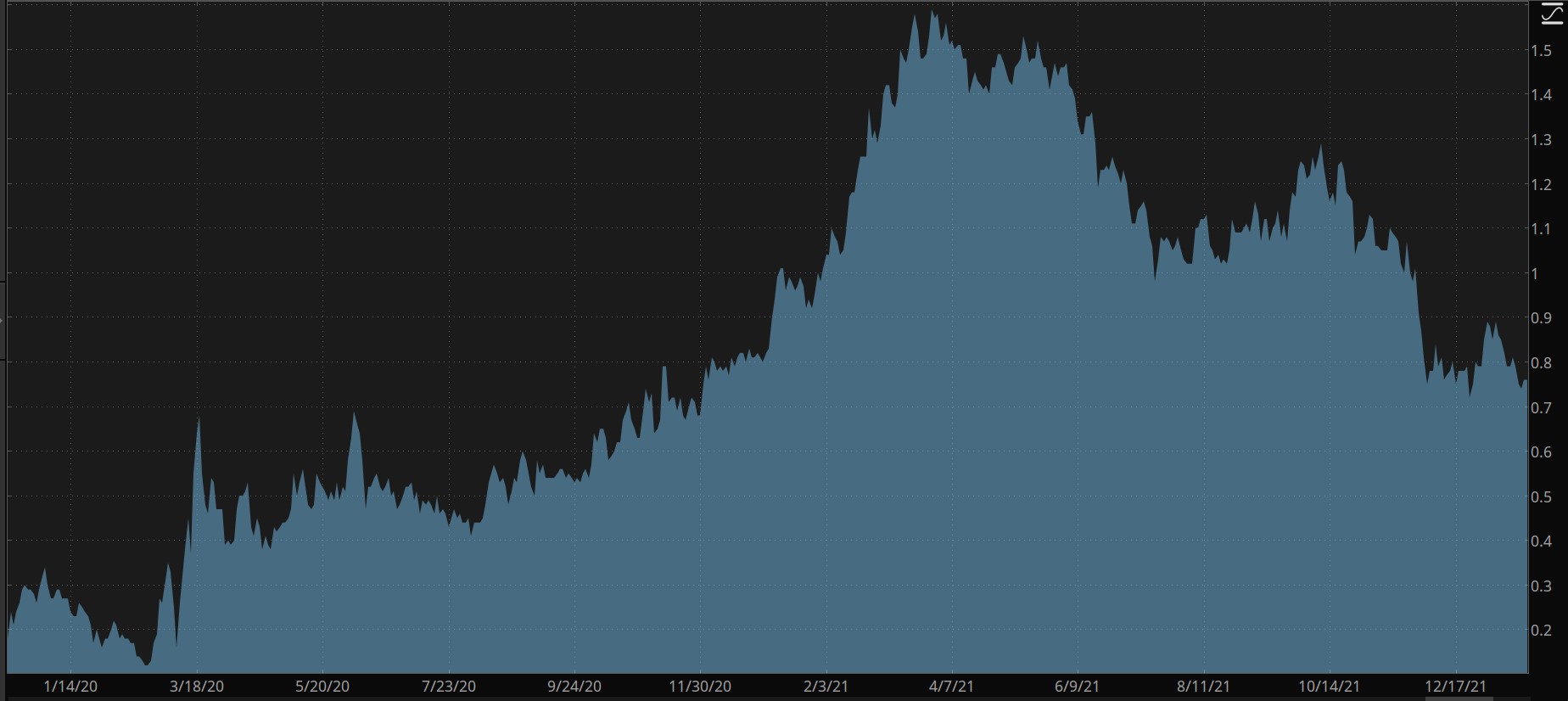

CHART OF THE DAY: AHEAD OF THE CURVE. The 10-year Constant Maturity Minus 2-year Treasury Constant Maturity (blue) is used to monitor changes in the yield curve. The curve steepened throughout the pandemic but started its flattening trend in April 2021. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Rate of Change: Throughout January, the yield curve has seen major shifts, particularly on the low end. The 2-month yield rose 50%, the 3-month skyrocketed 138%, the 6-month shot up 77%, the 1-year grew 63%, and the 2-year rose 31%. The remainder of the curve experienced gains but diminished by maturity. Climbing rates on the short end of the curve reflects the market’s expectations that Fed will raise rates sooner.

The long end of the curve will likely be more influenced by the Fed when it starts to reduce its balance sheet by allowing bonds to mature without replacing them and selling bonds. The Fed was buying longer-term bonds as part of its quantitative easing program to provide liquidity throughout the yield curve and keep rates low. However, the Fed did make it clear that the overnight rate is its primary tool, and that over the long run, it hopes to only hold Treasuries and not mortgage-backed securities.

Changing the Sheets: The rising short-term rates have continued to flatten the yield curve when looking at the 2s10s yield spread. Before the pandemic, the yield curve had already inverted, which is a precursor to a recession. The pandemic pushed the U.S. economy into a short recession, but the yield curve normalized and then steepened through April 2021. Since that time, the yield curve has been flattening but isn’t close to inverting.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Unsplash

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.