This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

AT-A-GLANCE

- Investors underestimated the actual amount of rate hikes at the outset of each of the past four tightening cycles

- Fed Funds futures underestimated the actual amount of tightening by 75-175bps

- Past tightening cycles came during periods of slower growth and much lower inflation

- Tighter U.S. fiscal policy could reduce the amount that the Fed needs to tighten

Even after the recent bout of turbulence in equity and bond markets, Fed Funds futures are still pricing a substantial tightening of monetary policy by the U.S. Federal Reserve (Fed). Fed Funds futures are pricing four or five rate hikes in 2022, followed by two or three more in 2023. In the view of investors, the Fed is most likely to have rates at 1.625% by the end of 2023 (Figure 1).

Figure 1: Investors are currently positioned for six to eight rate hikes in 2022 and 2023

But how accurately have investors been at anticipating past Fed tightening cycles? Looking back on the past four such cycles, the answer is: not very. In every tightening cycle from 1994 onward, Fed Funds futures substantially underestimated the actual number of rate hikes.

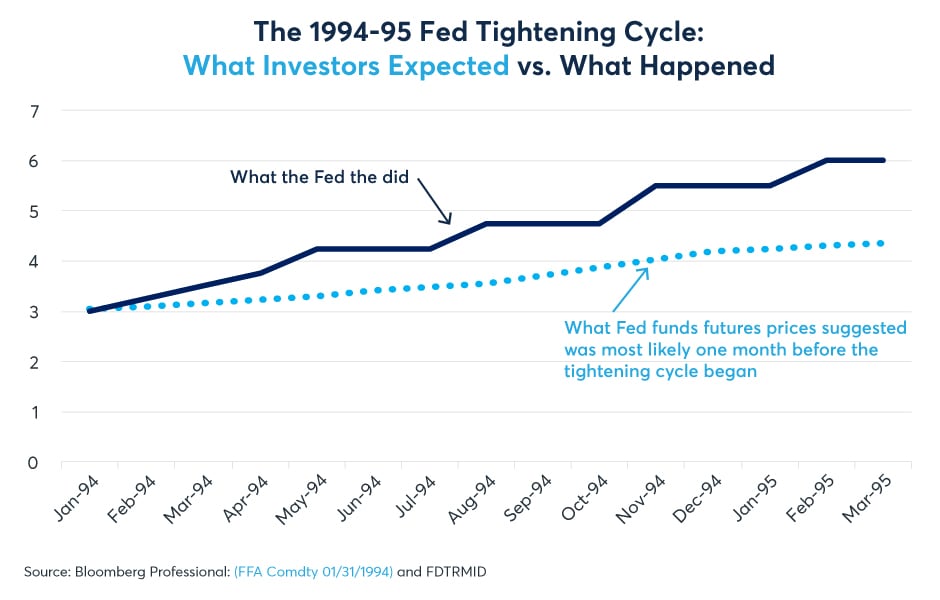

1994-95

In January 1994, with the economy several years into a recovery from the 1990-91 recession, Fed Fund futures priced a slow rise in U.S. interest rates. Investors expected rates to rise from 3% to perhaps around 4.25% by March 1995. The Fed, which was not yet engaged in managing market expectations, raised rates much more quickly than investors had anticipated and went much further, eventually raising rates to 6% by early 1995 before cutting them back to 5.25%. All told, the central bank went 175 basis points (bps) further than Fed Fund futures had anticipated at the outset of the tightening cycle (Figure 2).

Figure 2: In early 1994 investors priced 125bps of rate hikes and instead got 300bps

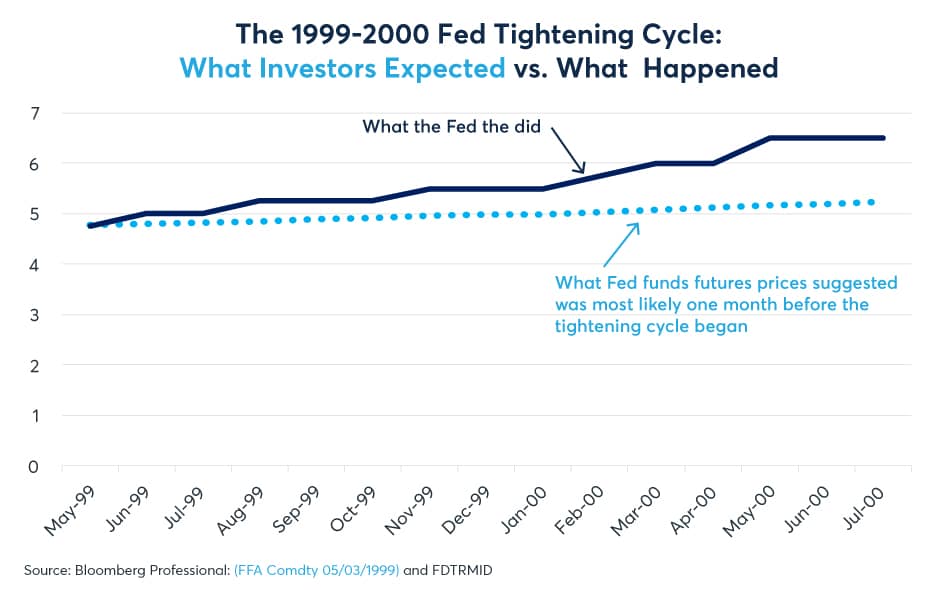

1999-2000

Following the Asian Crisis, the Russian debt default and the meltdown of hedge fund Long-Term Capital Management, the Fed cut rates from 5.5% to 4.75% over the summer and early fall of 1998. While those events created substantial volatility in financial markets, they had little impact on the real economy, which continued to grow strongly. In June 1999, the Fed decided it was time to withdraw its monetary policy accommodation and began raising rates. Investors were largely caught off guard. Going into this tightening cycle, Fed Funds futures priced that the Fed might hike rates to 5% by the end of 1999 and maybe to 5.25% by mid-2000. Instead, the Fed went much further, raising rates to 6.5%, which was followed by the tech wreck recession in 2001 (Figure 3).

Figure 3: In May 1999, Fed Funds futures priced 50bsp of rate hikes and got 175bps instead

2004-2006

Between 2000 and 2002 the tech-heavy Nasdaq index fell by 85%, and business investment contracted sharply. To prevent a deeper recession Fed Chair Alan Greenspan slashed rates from 6.5% to 1% by June 2003 and left them there until June 2004. By this time the Fed had begun signalling its intentions more clearly than it had in the past. As such, markets were somewhat better prepared for the 2004 to 2006 tightening cycle. At the outset of the cycle, Fed Funds futures priced that the Fed was most likely to raise rates to 4% by mid-2006. Once again, they went substantially further opting for 17 consecutive rate hikes that brought Fed Funds to 5.25% --125bps more than investors had anticipated at the outset (Figure 4).

Figure 4: Markets expected 300bps of tightening in 2004-06 and got 425bps instead

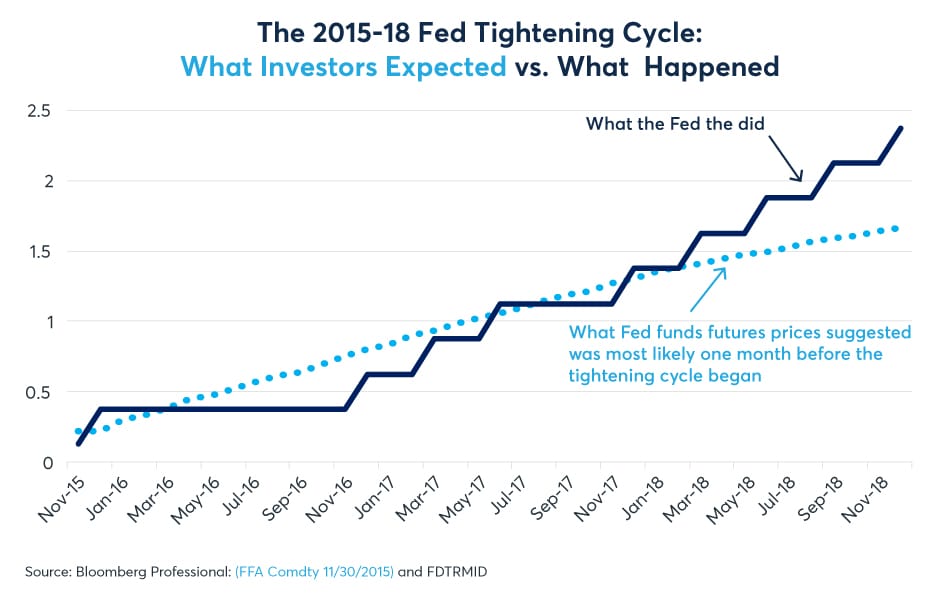

2015-18

By 2015, the Fed had become even more attuned to the idea of managing investor expectations. As such, the December 2015 rate hike came as no surprise to most investors. In this case, investors overestimated the Fed’s tightening in 2016, anticipating that they would have hiked rates twice more by November 2016. Instead, the Fed waited an entire year to do a second hike. In 2017 and 2018, however, the Fed hiked rates more quickly than investors expected eventually bringing its policy rate to 2.375%, about 75bps more than investors had anticipated at the outset of the cycle (Figure 5).

Figure 5: In 2015 Fed Funds futures priced 150bps of rate hikes but they wound up getting 225bps

In every one of the past four tightening cycles, the Fed raised rates 75-175bps more than the market initially anticipated. The bigger surprises came in the 1990s when interest rates were higher, moved more quickly and the Fed wasn’t yet engaged in managing investor expectations.

So, with investors expecting 150bps of tightening over the next two years, are they once again underestimating how far the Fed might eventually go? With inflation at 7% and unemployment below 4%, the possibility that the Fed might tighten further than investors currently anticipate seems very real. Even so, there are counter arguments:

- Fiscal policy will likely become much tighter as Congress appears unlikely to approve legislation for additional spending.

- An equity market correction might limit the degree to which the Fed might tighten.

- High levels of debt and leverage might make the U.S. economy more sensitive to rate hikes than it was in the past.

- The Fed might not want to invert the yield curve for fear of triggering a recession. Currently, 10Y yields are well below 2%. So, taking short-term rates higher than investors currently expect might depend on 10Y rates rising, which may be part of the Fed’s goal in shrinking its balance sheet.

Even so, the past four tightening cycles occurred during periods of relatively slow-paced declines in unemployment and periods of low and stable inflation. Going into what investors believe will be another tightening cycle beginning as soon as March 2022, the U.S. economy appears white hot, and that might be increasing the upside risks for rates relative to investor expectations.

Featured image provided by CME Group

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.