Judging by the coverage in most of the Western media, Russia is getting soundly beaten in its war with Ukraine. That may be an artifact of the West's (and Ukraine's) superiority at electronic media. The Ukrainian President, Vladimir Zelensky, is, after all, a former television star and producer, who understands media well. And Western media are full of stories of plucky Ukrainian defenders defeating bumbling Russian invaders, such as this article from the Financial Times.

Great reportage: how Ukraine inflicted a stinging defeat on Russian forces at the Battle of Kyiv https://t.co/aRNhDenRx9

— Lionel Barber (@lionelbarber) April 11, 2022

Some military experts, such as retired U.S. Army Colonel Douglas Macgregor, say that the Russian army never intended to take Kiev, that its forces deployed in the vicinity of Kiev were merely meant to tie down Ukrainian forces. But those experts have been losing the media war along with Russia.

So much for the media (bits). What about the physical world (atoms)? There, the picture looks starkly different.

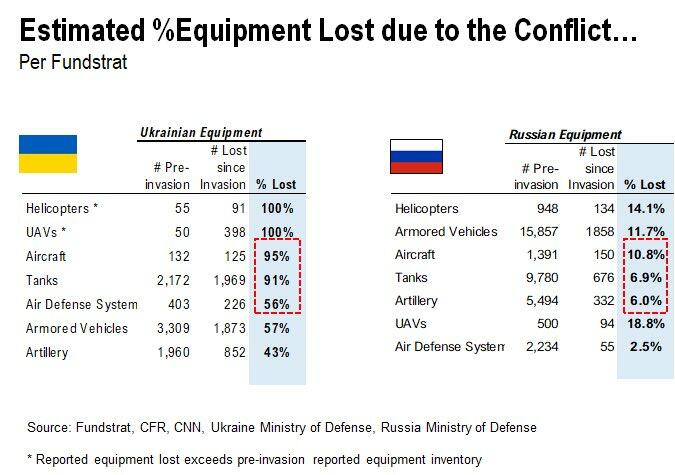

According to the data above, Ukraine has lost 91% of its tanks since Russia invaded, while Russia has lost 6.9% of its tanks.

A similar dynamic may be at work in the West's economic war against Russia. Over the weekend, the Financial Times expressed incredulity that "contrarian" fund manager Dave Iben hadn't written down his position in Gazprom--which has shipped record amounts of gas to Europe throughout the war--to zero.

Contrarian fund manager cautions against writing off Russia assets https://t.co/z4Cm226dxq

— Financial Times (@FT) April 10, 2022

Similarly, President Biden quipped after levying unprecedented sanctions on Russia that the ruble was now "rubble", but Russia's currency has already recovered to pre-war levels.

It appears that the laptop class in the West has underestimated the resilience and size of Russia's economy because it's more based on the physical world than ours is. That observation was fleshed out by French economist Jacques Sapir, as Arnaud Bertrand shared in the Twitter thread below.

Contrarian fund manager cautions against writing off Russia assets https://t.co/z4Cm226dxq

— Financial Times (@FT) April 10, 2022

- Massive Demand & Disruptive Potential – Boxabl has received interest for over 190,000 homes, positioning itself as a major disruptor in the housing market.

- Revolutionary Manufacturing Approach – Inspired by Henry Ford’s assembly line, Boxabl’s foldable tiny homes are designed for high-efficiency production, making homeownership more accessible.

- Affordable Investment Opportunity – With homes priced at $60,000, Boxabl is raising $1 billion to scale production, offering investors a chance to own a stake in its growth.

However this is the worst possible way of comparing the size of economies. A slightly more accurate way is to adjust for PPP (purchasing power parity: https://t.co/SmlsvzplMB) When you do so, you already realize that Russia's economy is actually more like the size of Germany's.

— Arnaud Bertrand (@RnaudBertrand) April 10, 2022

He says that when you adjust for this Russia's economy is vastly bigger than Germany's. His estimate is that Russia represents in fact maybe "5% or 6% of the world's economy", almost double the size it's normally estimated at on a PPP basis (https://t.co/I0WHghMEk3)

— Arnaud Bertrand (@RnaudBertrand) April 10, 2022

This is a fascinating way to look at it and it rings very true. This crisis is making us realize that we used to take manufacturing, the industry and commodities for granted, i.e. an antiquated side of the economy compared to shiny new "services".

— Arnaud Bertrand (@RnaudBertrand) April 10, 2022

Bertrand then extends this analysis to China and America.

It's also very interesting to revalue China's economy through that lens. If we look at the Chinese economy simply based on exchange rates, it is a $17.7 trillion economy to the U.S.'s $23 trillion.

— Arnaud Bertrand (@RnaudBertrand) April 10, 2022

All in all, this means that China and Russia's economies combined are in fact likely about 35% of the world's economy when taking PPP into account as well as compensating for the over-valuation of the service sector.

— Arnaud Bertrand (@RnaudBertrand) April 10, 2022

If you look at our top names from Friday, our system is not taking the physical world, and the economy based on it, for granted.

Screen capture via Portfolio Armor on 4/8/2022.

Here's how that top ten breaks down:

- Wheat: Teucrium Wheat Fund WEAT

- Oil & Gas: Occidental Petroleum Corp. OXY, Direxion Daily S&P Oil & Gas Exp. & Prod. Bull 2x Shares GUSH, and United States Oil Fund LP USO.

- Home solar energy: Enphase Energy, Inc. ENPH

- Fertilizer: CF Industries Holdings, Inc. CF

- Coal: Peabody Energy Corp. BTU

- Aluminum: Century Aluminum Co. CENX

- Coffee: iPath, Series B Bloomberg Coffee Subindex Total Return ETF JO

- Gold: VanEck Vectors Junior Gold Miners ETF GDXJ

These are the names our system is putting in portfolios now for the next six months. They're positioned to benefit from the sanctions regime making food and energy more expensive, and in the case of GDXJ, from Russia linking its currency to gold.

As always though, we suggest readers who buy any of our top names consider hedging, in case we end up being wrong, or the market goes against us. You can use our website or iPhone app to scan for optimal hedges on each of our top names.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.